- Two-Thirds of Americans Look Forward to Working for Pleasure and Would Prefer a Phased Retirement

- Confidence in Retirement is Strong Among Those Investing, but All Generations Wish They Started Planning Earlier

- Investors Can Retire their Way Using Fidelity’s Retirement Planning Hub

Several years since the pandemic began, its societal and economic impact is still felt throughout the country, as many Americans now opt for a non-traditional approach to retirement. According to the latest Fidelity Investments® State of Retirement Planning study, which examines how people are viewing and planning for retirement, 2-in-3 (66%) respondents say the pandemic made them more intentional about focusing on their personal passions and dreams in retirement, with Millennials leading the charge at 73%.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20240312987682/en/

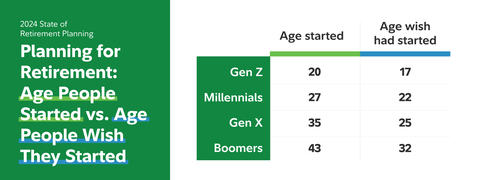

(Graphic: Business Wire)

The traditional retirement no longer holds much appeal for more than half of Gen Z (60%) and Millennials (58%), who are encouraged by the rise of remote work and are more likely than their older counterparts to travel, relocate to somewhere scenic or abroad, or take a chance on starting their own business in retirement. Across generations, two-thirds look forward to pursuing work for pleasure while in retirement and hope for a phased retirement – working full-time at first, then part-time, before stopping altogether.

“Americans are approaching their ‘golden years’ with more intention and opportunity than ever before,” said Rita Assaf, vice president of Retirement Products at Fidelity Investments. “As more people rethink retirement, with new goals such as living abroad or starting a business, it’s important to consider the potential impacts to their Social Security, Medicare and taxes. We’re encouraged to see a growing understanding of the value in creating a retirement plan early, which helps people map out the best strategy for reaching their goals.”

Confidence Abounds on the Road to Retirement, Despite Ongoing Concerns

Despite one of the most challenging and unpredictable economic environments in recent history, the encouraging news is that three-quarters of respondents expressed confidence about retiring when and how they want, although many women and older generations were less confident than their male and younger counterparts. Improving market performance in the fourth quarter certainly played a part, with Fidelity’s latest data showing retirement account balances at the highest they’ve been in two years.

However, many concerns still remain. Compared to their parents’ retirement, over half of younger generations (56% of Gen Z and 57% of Millennials) believe they’ll have a harder time saving for retirement due to the higher cost of living (compared to only 16% of Boomers and 38% of Gen X). Across generations, inflation, consumer debt and building emergency savings are the main barriers to reaching retirement savings goals; although younger people also cite additional challenges such as student debt, saving for a home and wedding, as well as childcare costs. Given these common hurdles, all generations wish they had started planning for retirement earlier, including Gen Z, who started planning at an average age of 20.

Optimistically, retirement savers noted recent legislative changes have made saving easier, such as the passage of SECURE 2.0, particularly as it relates to employers helping their workforce save for retirement while paying down student debt and building up emergency savings. In fact, a third of Gen Z believe their employer could leverage the new legislation to help them save more for retirement by making a matching retirement contribution when they make their student loan payments. Additionally, one-third of Gen Z and Millennials say it will help them save more for retirement while building up emergency savings. This legislation has also added tax credits for small businesses offering retirement plans, including benefits for their employees who participate.

Technological advancements have also made saving easier. For example, 1-in-10 are using a robo advisor to manage their retirement savings, with the heaviest users being Millennials at 20%. Most robo advisor users say the technology has helped them simplify investing (87%), increase their risk tolerance (80%), as well as improve their confidence in reaching investment goals (81%). Younger generations are also twice as likely than their older counterparts to seek financial guidance from digital sources, such as a robo advisor, social media channels or influencers they follow.

However, even among those aware of robo advisors, nearly 4-in-5 across all generations agree having access to a human financial advisor is still important for when they have questions. Over three-quarters also prefer working with a human financial advisor when it comes to creating a plan to accomplish their goals.

Living in Retirement

Nearly all respondents (85%) want to retire while they are still healthy enough to be active, targeting an average retirement age of 61-62. Motivating factors for determining when to retire vary by generation though; Gen Z and Millennials cite becoming debt-free or reaching career goals as top factors; whereas Boomers say they’ll retire when they emotionally ‘feel’ ready. One-in-10 Gen X respondents have not yet determined when they plan to retire, although they are continuing to save at Fidelity’s recommended savings rate of 15% of their income (this includes employer and employee contributions). Encouragingly, younger generations are currently saving an even higher percentage of their income for retirement, with Millennials saving 20% and Gen Z saving 25%.

When it comes time to draw down hard-earned retirement savings, the majority (80%) of people with a retirement income plan are at least somewhat confident that plan will meet their goals. That said, nearly half still have some concerns in the back of their head about having enough money in retirement, including outliving their savings. Maintaining mental and physical fitness followed as other close concerns. Among the just under one-fifth who claim to have retired – and then unretired – the reasons for going back to work were evenly divided between financial and mental.

To help people retire the way they want, Fidelity offers a retirement planning hub for online tips and resources. Fidelity also created the Fidelity Retirement Score℠, which provides a rough estimate of how much people may need in retirement and suggests ways to help improve their score. Additionally, Fidelity offers digital advice through Fidelity Go® and Managed FidFolios℠, as well as human financial professional support at one of Fidelity’s Investor Centers or by phone at 1-800-FIDELITY (1-800-343-3548). Plus, for those with Fidelity workplace retirement accounts, there is access to one-on-one appointments, phone consultations and workshops through their employers.

About the Fidelity Investments 2024 State of Retirement Planning Study

This study presents the findings of a national online survey, consisting of 2,014 adult financial decision makers age 18 plus who own an investment account. Respondents had at least one investment account. The generations are defined as: Baby Boomers (ages 59-77), Gen X (ages 43-58), Millennials (ages 27-42) and Gen Z (ages 18-26). Interviewing was conducted December 7-15, 2023 by Big Village, which is not affiliated with Fidelity Investments. The results may not be representative of all adults meeting the same criteria as those surveyed. For a detailed look at the study, go here.

About Fidelity Investments

Fidelity’s mission is to strengthen the financial well-being of our customers and deliver better outcomes for the clients and businesses we serve. Fidelity’s strength comes from the scale of our diversified, market-leading financial services businesses that serve individuals, families, employers, wealth management firms, and institutions. With assets under administration of $12.6 trillion, including discretionary assets of $4.9 trillion as of December 31, 2023, we focus on meeting the unique needs of a broad and growing customer base. Privately held for 77 years, Fidelity employs more than 74,000 associates across the United States, Ireland, and India. For more information about Fidelity Investments, visit https://www.fidelity.com/about-fidelity/our-company.

**Fidelity Go® provides discretionary investment management, and in certain circumstances, non-discretionary financial planning, for a fee.** Advisory services offered by Fidelity Personal and Workplace Advisors LLC (FPWA), a registered investment adviser. Brokerage services provided by Fidelity Brokerage Services LLC (FBS), and custodial and related services provided by National Financial Services LLC (NFS), each a member NYSE and SIPC. FPWA, FBS and NFS are Fidelity Investments companies.

IMPORTANT: The projections or other information generated by Fidelity Retirement Score regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. Results may vary with each use and over time.

Investing involves risk, including risk of loss.

Views expressed are as of the date indicated, based on the information available at that time, and may change based on market or other conditions. Unless otherwise noted, the opinions provided are those of the speaker or author and not necessarily those of Fidelity Investments or its affiliates. Fidelity does not assume any duty to update any of the information.

###

Fidelity Brokerage Services LLC, Member NYSE, SIPC,

900 Salem Street, Smithfield, RI 02917

Fidelity Distributors Company LLC,

900 Salem Street, Smithfield, RI 02917

National Financial Services LLC, Member NYSE, SIPC,

245 Summer Street, Boston, MA 02205

1135229.1.0

©2024 FMR LLC. All rights reserved

View source version on businesswire.com: https://www.businesswire.com/news/home/20240312987682/en/

Contacts

Fidelity Media Relations

fidelitymediarelations@fmr.com

Sohana O’Hare

(214) 693-4501

sohana.ohare@fmr.com

Visit our online newsroom