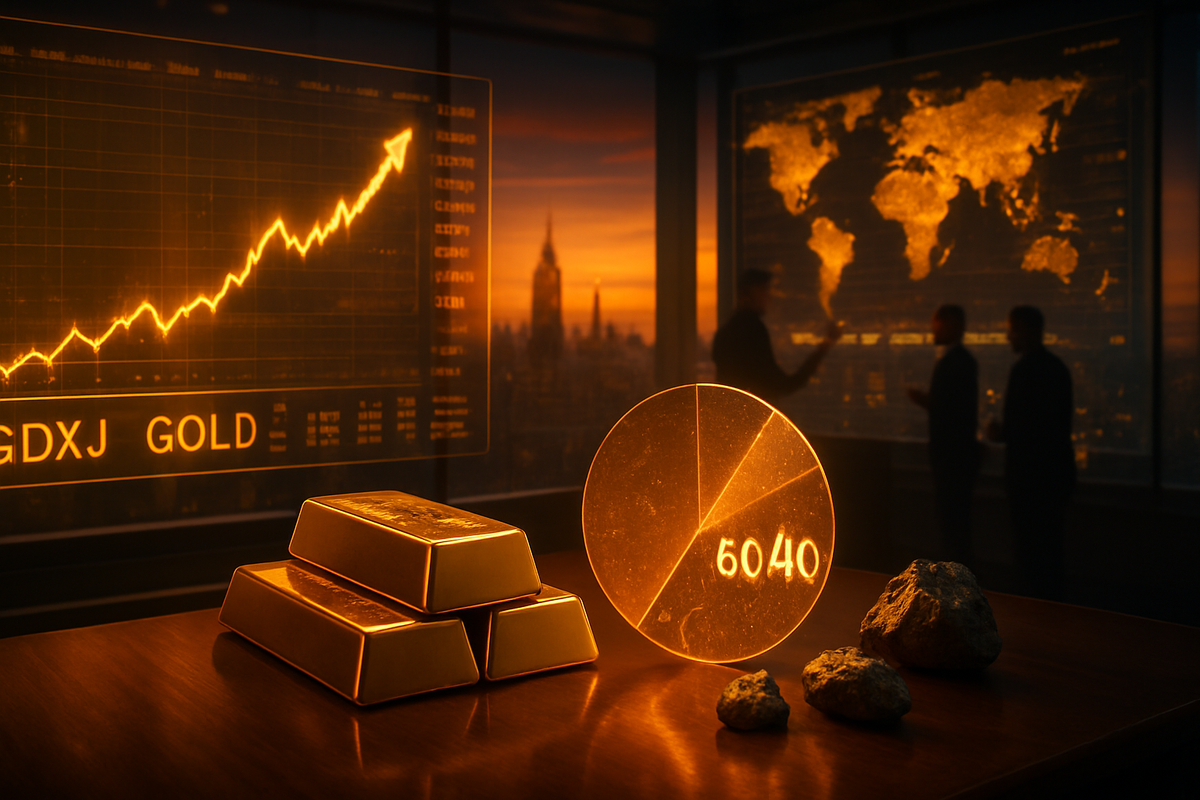

NEW YORK — As the calendar turns to mid-January 2026, the financial landscape is undergoing a structural transformation not seen in nearly half a century. The traditional 60/40 portfolio, a cornerstone of conservative wealth management for decades, is being systematically dismantled in favor of "hard money" allocations. Driven by a relentless climb in the price of bullion, which recently breached the $4,600 per ounce threshold, institutional and retail investors alike are flocking to precious metals to shield themselves from a looming sovereign debt crisis and the persistent erosion of fiat currency value.

The immediate fallout of this shift has been a historic capital flight from government bonds into liquid gold proxies and high-growth mining equities. By January 15, 2026, major wealth management firms have begun revising their "neutral" gold allocations from a mere 5% to as high as 25%. This "Gold Super-Cycle," as many are now calling it, has turned the junior mining sector into the market’s primary engine for alpha, with the VanEck Junior Gold Miners ETF (NYSE Arca: GDXJ) standing as the poster child for this new era of asset allocation.

The 153% Surge: A Year of Junior Mining Dominance

The current fervor follows a blistering 2025 that saw the VanEck Junior Gold Miners ETF (NYSE Arca: GDXJ) surge by a staggering 153%. This performance was not merely a speculative bubble but the result of a "perfect storm" of fundamental drivers. Throughout 2025, the gold spot price rose by over 60%, but junior miners provided the leverage that investors craved. As producer margins expanded—with many junior firms reporting all-in sustaining costs (AISC) below $1,500 while selling gold for nearly triple that price—the sector became a cash-flow machine. This led to a massive influx of capital into the ETF, which serves as a basket for small-to-mid-cap explorers and producers that typically outperform senior miners during aggressive bull runs.

The timeline leading to this moment began in late 2024, when global central banks accelerated their de-dollarization efforts. By mid-2025, the world watched as foreign central banks, led by the People’s Bank of China and the National Bank of Poland, collectively purchased over 1,000 tonnes of gold for the fourth year in a row. For the first time since the mid-1990s, the value of gold held in central bank reserves globally surpassed the value of U.S. Treasury holdings. This milestone triggered a psychological shift among Western institutional investors, who realized that the "safe haven" of the past—government debt—was being actively replaced by "monetary metals" on the world's most significant balance sheets.

Market participants were initially skeptical of the 2025 rally, often dismissing it as a temporary hedge against geopolitical tensions. However, as the U.S. national debt cleared the $40 trillion mark in early 2026, the narrative shifted toward a "fiscal doom loop." The industry’s reaction has been one of total re-orientation; major brokerage houses that once mocked "gold bugs" are now launching specialized precious metals desks to handle the deluge of buy orders for mining ETFs and physical bullion.

Winners and Losers in the Super-Cycle

The primary beneficiaries of this shift are the nimble producers within the VanEck Junior Gold Miners ETF (NYSE Arca: GDXJ) and its senior counterpart, the VanEck Gold Miners ETF (NYSE Arca: GDX). Individual companies with high-quality deposits and low debt levels, such as Agnico Eagle Mines (NYSE: AEM) and Barrick Gold (NYSE: GOLD), have seen their market capitalizations swell as they benefit from record-breaking free cash flow. These companies are now being viewed not just as miners, but as dividend-paying alternatives to traditional utility stocks, appealing to a much broader investor base.

Conversely, the traditional "60/40" devotees and bond-heavy funds are the clear laggards of 2026. Long-dated U.S. Treasuries have failed to provide the diversification benefit they historically offered, as both stocks and bonds have occasionally sold off in tandem due to debt sustainability fears. Asset managers who failed to pivot are seeing massive redemptions. Furthermore, the SPDR Gold Shares (NYSE Arca: GLD) and the iShares Gold Trust (NYSE Arca: IAU) have seen record inflows, often at the direct expense of "Growth" ETFs that dominated the early 2020s.

The broader banking sector is also feeling the pinch. As central banks and private investors move up to 25% of their portfolios into gold, the demand for traditional dollar-denominated financial products has softened. However, bullion-heavy banks and custodial services for physical metal are seeing a boom. For the average consumer, the "winner" status is bittersweet; while their gold-heavy retirement accounts are surging, the underlying cause—currency debasement—is manifesting as persistently high costs for imported goods and services.

The End of 60/40 and the Rise of the 25% Gold Standard

The wider significance of this trend cannot be overstated: we are witnessing the obsolescence of the 60/40 portfolio. This model relied on the inverse correlation between stocks and bonds, a relationship that has disintegrated as sovereign debt risks have moved to the forefront of global macroeconomics. In the 2026 market, gold has effectively "fired" the bond market from its role as the primary defensive asset. The recommendation by leading analysts to allocate 25% of a portfolio to gold is a return to a more defensive, historical posture reminiscent of the "Permanent Portfolio" strategy of the 1970s.

This shift fits into a broader trend of "geopolitical fragmentation," where trust in a unified global financial system is fraying. Nations are no longer willing to store all their wealth in another country's currency, fearing sanctions or debt monetization. This has ripple effects on competitors and partners alike; as more capital flows into gold, less is available for venture capital and speculative tech, potentially slowing the pace of innovation in other sectors of the economy.

Historically, this era is being compared to the 1971-1980 period, when gold rose from $35 to $850. However, the scale of today's debt—and the speed of information—has made the 2025-2026 move even more volatile. Regulators are now struggling to keep up, with some central banks considering "Gold-Backed Digital Currencies" to regain some control over the monetary system. This transition represents a fundamental loss of faith in the ability of central planners to manage debt without debasing the currency.

Looking Ahead: $5,000 Gold and Beyond?

In the short term, the momentum behind the gold super-cycle shows no signs of abating. Technical analysts point to a "Wave 3" breakout, a phase characterized by rapid price appreciation and high volume. By the end of 2026, many institutional desks, including J.P. Morgan and Goldman Sachs, have projected gold targets between $5,000 and $6,000 per ounce. For the VanEck Junior Gold Miners ETF (NYSE Arca: GDXJ), this could mean another year of triple-digit gains as smaller explorers are acquired by larger majors desperate to replenish their reserves.

However, a strategic pivot will be required for the market at large. As gold becomes a larger percentage of global wealth, we may see a "re-pricing" of all other assets. Real estate and equities may begin to be valued in ounces of gold rather than dollars to provide a clearer picture of real value. The major challenge for the next 24 months will be the potential for "gold nationalism," where countries might restrict the export of gold or tax mining profits at punitive rates to shore up their own national treasuries.

If the sovereign debt crisis reaches a boiling point, we could see an ultimate scenario where a new Bretton Woods-style agreement is sought, re-pegging currencies to a basket of commodities that includes gold. Until then, the volatility in the precious metals space remains both a risk and an unparalleled opportunity for those who recognized the shift early.

A New Era for Asset Allocation

The narrative of 2026 is clear: the era of "easy" diversification through the 60/40 model is over. Gold has transitioned from a fringe "doomsday" asset to a pillar of the modern institutional portfolio. The 153% surge of junior miners in 2025 was the first loud alarm bell, and the subsequent reallocation of trillions of dollars into monetary metals is the resulting seismic shift.

As we move forward, the market will likely be defined by "gold-driven inflation" and a scramble for tangible assets. Investors should keep a close eye on the Federal Reserve's response to debt levels and the monthly gold accumulation reports from central banks. For those holding VanEck Junior Gold Miners ETF (NYSE Arca: GDXJ) and similar instruments, the current super-cycle offers a once-in-a-generation tailwind, but it also signals a world where the very definition of "money" is being rewritten.

This content is intended for informational purposes only and is not financial advice.