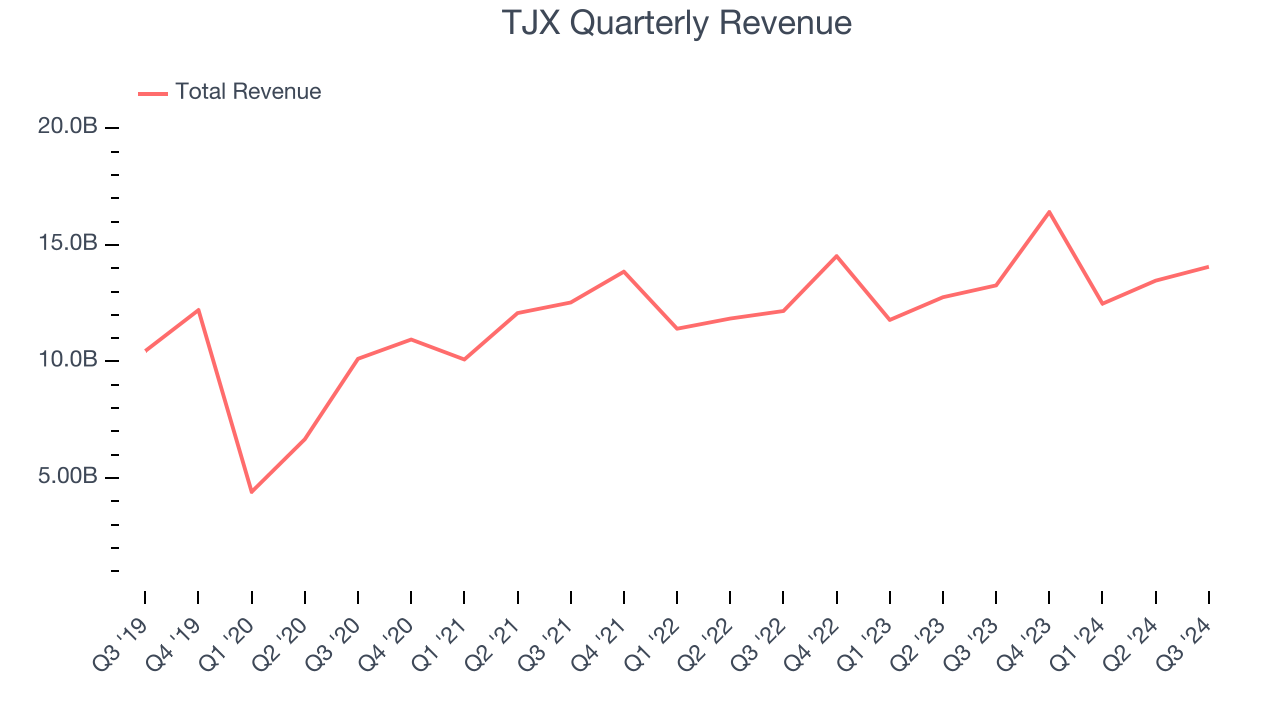

Off-price retail company TJX (NYSE: TJX) reported Q3 CY2024 results topping the market’s revenue expectations, with sales up 6% year on year to $14.06 billion. Its GAAP profit of $1.14 per share was 4% above analysts’ consensus estimates.

Is now the time to buy TJX? Find out by accessing our full research report, it’s free.

TJX (TJX) Q3 CY2024 Highlights:

- Revenue: $14.06 billion vs analyst estimates of $13.95 billion (6% year-on-year growth, 0.8% beat)

- Adjusted EPS: $1.14 vs analyst estimates of $1.10 (4% beat)

- EPS (GAAP) guidance for Q4 is $1.13 at the midpoint, missing analysts' expectations

- EPS (GAAP) guidance for the full year is $4.16 at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 12%, in line with the same quarter last year

- Free Cash Flow Margin: 4.4%, similar to the same quarter last year

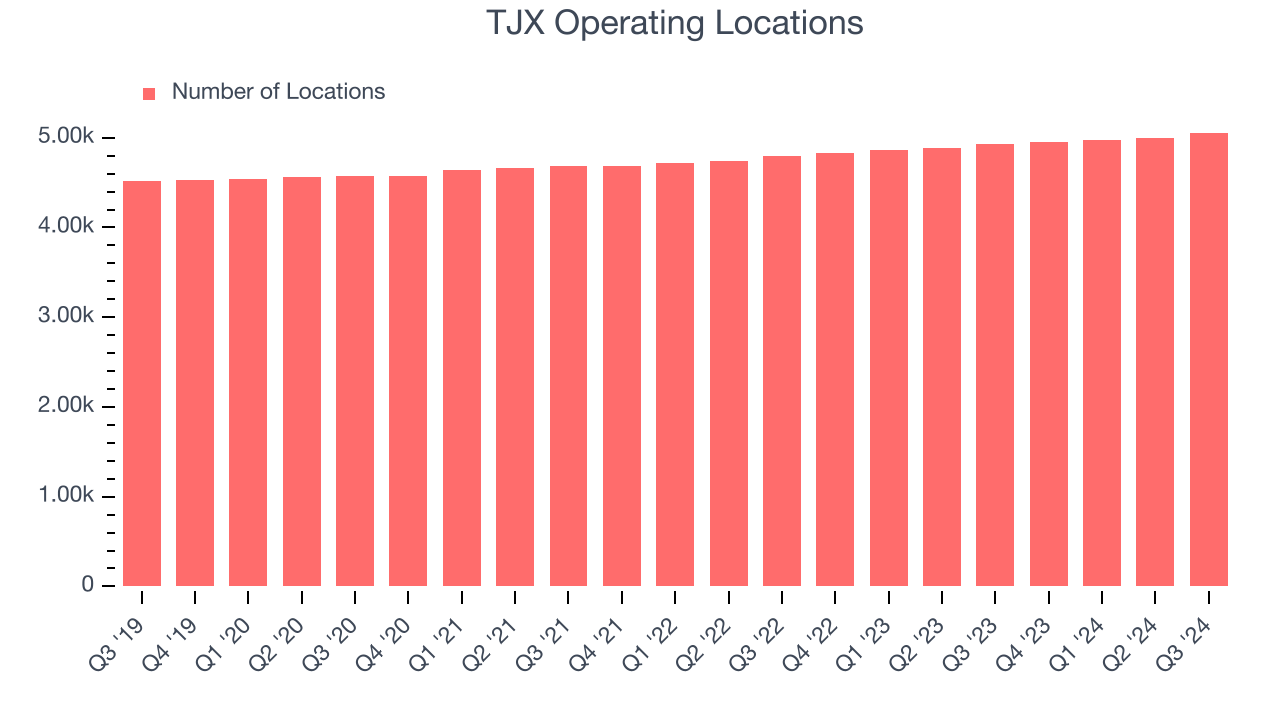

- Locations: 5,057 at quarter end, up from 4,934 in the same quarter last year

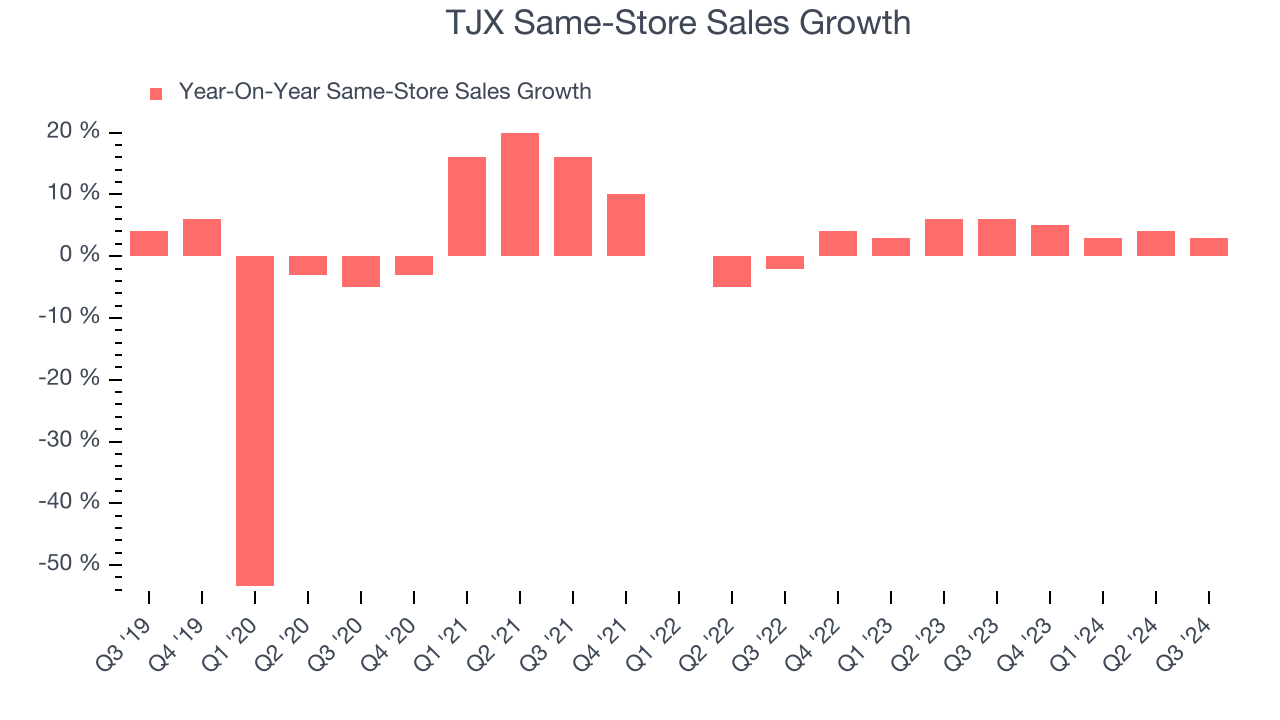

- Same-Store Sales rose 3% year on year (6% in the same quarter last year)

- Market Capitalization: $134.8 billion

Ernie Herrman, Chief Executive Officer and President of The TJX Companies, Inc., stated, “I am very pleased with our third quarter results and the strong execution of our off-price business fundamentals by our teams. Our comp store sales increase of 3% was at the high-end of our plan, and both pretax profit margin and earnings per share came in well above our expectations. Across the Company, customer transactions drove our comp sales increases, which tells us that our values and treasure hunt shopping experience are appealing to a wide range of customers. I want to specifically highlight our European team for their strong results, which drove the 7% comp increase at our TJX International division. With our above-plan profitability results in the third quarter, we are raising our full year guidance for pretax profit margin and earnings per share. The fourth quarter is off to a strong start, and we are excited about our opportunities for the holiday selling season. In stores and online, we are offering consumers an ever-changing and inspiring shopping destination for gifts at excellent values, and feel confident that there will be something for everyone when they shop us. Going forward, we continue to see great potential to successfully grow TJX around the globe well into the future.”

Company Overview

Initially based on a strategy of buying excess inventory from manufacturers or other retailers, TJX (NYSE: TJX) is an off-price retailer that sells brand-name apparel and other goods at prices much lower than department stores.

Discount Retailer

Discount retailers understand that many shoppers love a good deal, and they focus on providing excellent value to shoppers by selling general merchandise at major discounts. They can do this because of unique purchasing, procurement, and pricing strategies that involve scouring the market for trendy goods or buying excess inventory from manufacturers and other retailers. They then turn around and sell these snacks, paper towels, toys, clothes, and myriad other products at highly enticing prices. Despite the unique draw and lure of discounts, these discount retailers must also contend with the secular headwinds of online shopping and challenged retail foot traffic in places like suburban strip malls.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one sustains growth for years.

TJX is a behemoth in the consumer retail sector and benefits from economies of scale, giving it an edge in distribution and the flexibility to offer lower prices. However, its scale is a double-edged sword because there are only a finite number of places to build new stores, making it harder to find incremental growth.

As you can see below, TJX’s 6.8% annualized revenue growth over the last five years (we compare to 2019 to normalize for COVID-19 impacts) was tepid, but to its credit, it opened new stores and increased sales at existing, established locations.

This quarter, TJX reported year-on-year revenue growth of 6%, and its $14.06 billion of revenue exceeded Wall Street’s estimates by 0.8%.

Looking ahead, sell-side analysts expect revenue to grow 3.9% over the next 12 months, a slight deceleration versus the last five years. We still think its growth trajectory is satisfactory and implies the market is baking in success for its products. Some tapering/deceleration is natural given the magnitude of its revenue base.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Store Performance

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

TJX sported 5,057 locations in the latest quarter. Over the last two years, it has opened new stores quickly, averaging 2.7% annual growth. This was faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

TJX’s demand has been spectacular for a retailer over the last two years. On average, the company has increased its same-store sales by an impressive 4.3% per year. This performance suggests its rollout of new stores is beneficial for shareholders. We like this backdrop because it gives TJX multiple ways to win: revenue growth can come from new stores, e-commerce, or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, TJX’s same-store sales rose 3% year on year. This growth was a deceleration from its historical levels, showing the business is still performing well but losing a bit of steam.

Key Takeaways from TJX’s Q3 Results

It was good to see TJX narrowly top analysts’ revenue and gross margin expectations this quarter. This led to an EPS beat. On the other hand, its EPS guidance for next quarter missed. Overall, this quarter was mixed. The stock remained flat at $120.10 immediately following the results.

Is TJX an attractive investment opportunity right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.