Saia has been on fire lately. In the past six months alone, the company’s stock price has rocketed 40.7%, reaching $557.50 per share. This run-up might have investors contemplating their next move.

Is there a buying opportunity in Saia, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.We’re happy investors have made money, but we're swiping left on Saia for now. Here are three reasons why you should be careful with SAIA and a stock we'd rather own.

Why Is Saia Not Exciting?

Pivoting its business model after realizing there was more success in delivering produce than selling it, Saia (NASDAQ: SAIA) is a provider of freight transportation solutions.

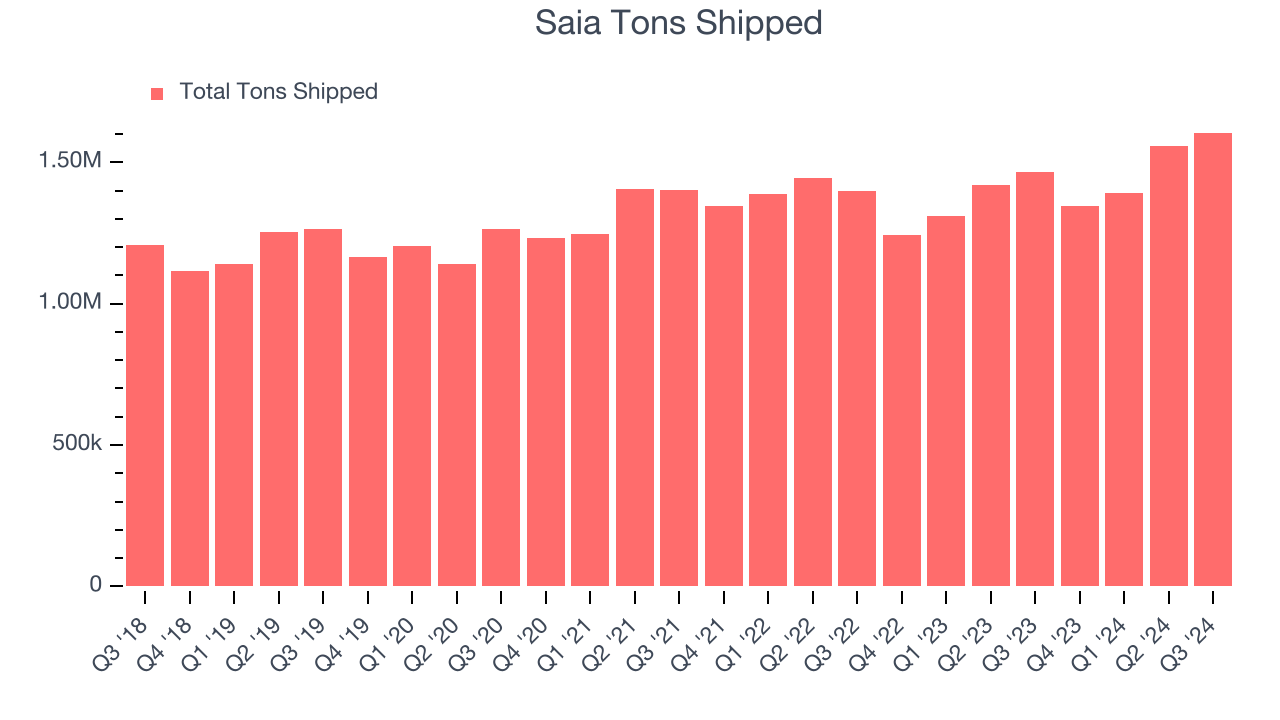

1. Weak Sales Volumes Indicate Waning Demand

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Ground Transportation company because there’s a ceiling to what customers will pay.

Saia’s tons shipped came in at 1.61 million in the latest quarter, and over the last two years, averaged 3% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

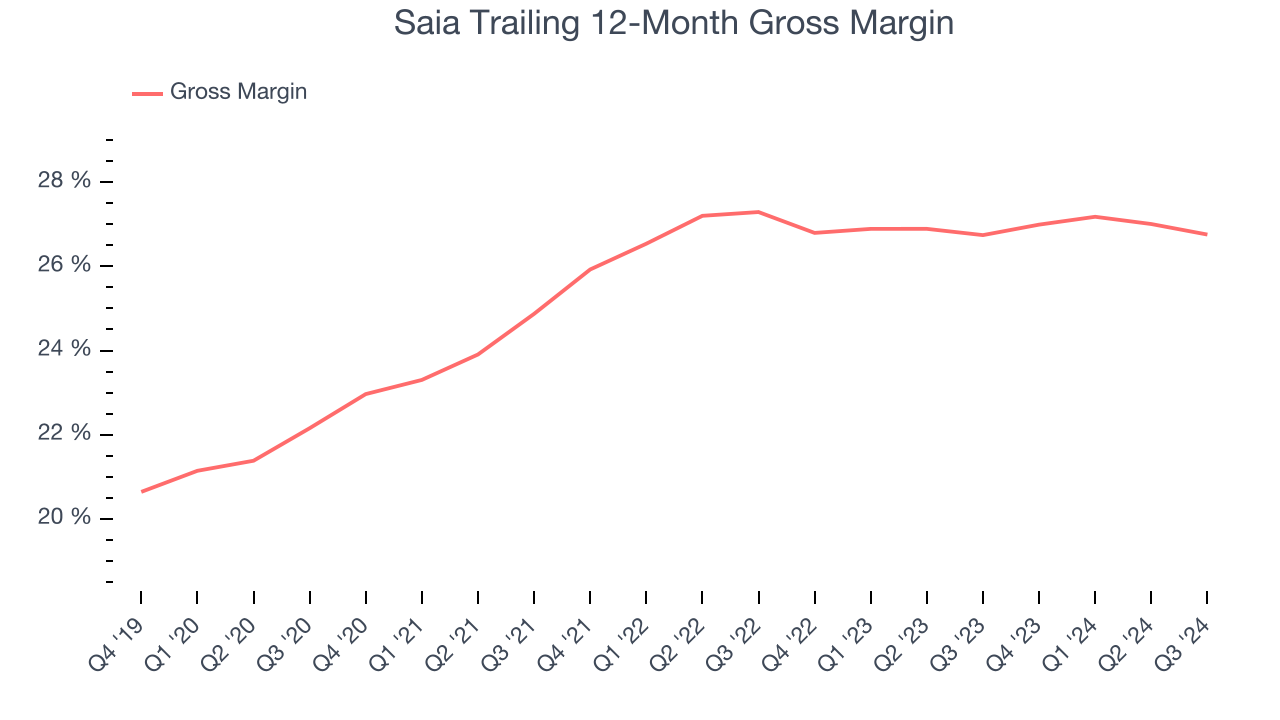

2. Low Gross Margin Reveals Weak Structural Profitability

Cost of sales for an industrials business is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics.

Saia has weak unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 25.9% gross margin over the last five years. Said differently, Saia had to pay a chunky $74.10 to its suppliers for every $100 in revenue.

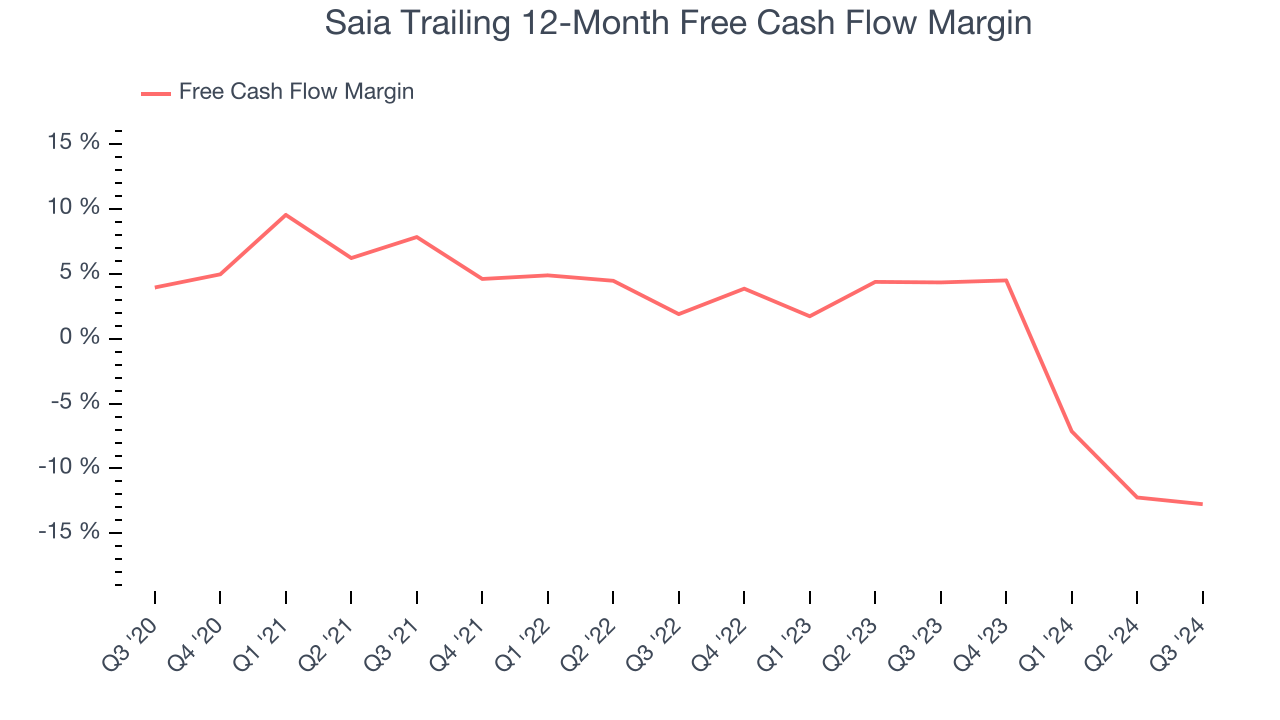

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Saia’s margin dropped by 16.7 percentage points over the last five years. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. Saia’s free cash flow margin for the trailing 12 months was negative 12.7%.

Final Judgment

Saia isn’t a terrible business, but it isn’t one of our picks. After the recent surge, the stock trades at 36.1x forward price-to-earnings (or $557.50 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. We’d recommend looking at Wingstop, a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Would Buy Instead of Saia

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.