As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q3. Today, we are looking at toys and electronics stocks, starting with Mattel (NASDAQ: MAT).

The toys and electronics industry presents both opportunities and challenges for investors. Established companies often enjoy strong brand recognition and customer loyalty while smaller players can carve out a niche if they develop a viral, hit new product. The downside, however, is that success can be short-lived because the industry is very competitive: the barriers to entry for developing a new toy are low, which can lead to pricing pressures and reduced profit margins, and the rapid pace of technological advancements necessitates continuous product updates, increasing research and development costs, and shortening product life cycles for electronics companies. Furthermore, these players must navigate various regulatory requirements, especially regarding product safety, which can pose operational challenges and potential legal risks.

The 4 toys and electronics stocks we track reported a satisfactory Q3. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 6.6% below.

Luckily, toys and electronics stocks have performed well with share prices up 10.4% on average since the latest earnings results.

Mattel (NASDAQ: MAT)

Known for the creation of iconic toys such as Barbie and Hotwheels, Mattel (NASDAQ: MAT) is a global children's entertainment company specializing in the design and production of consumer products.

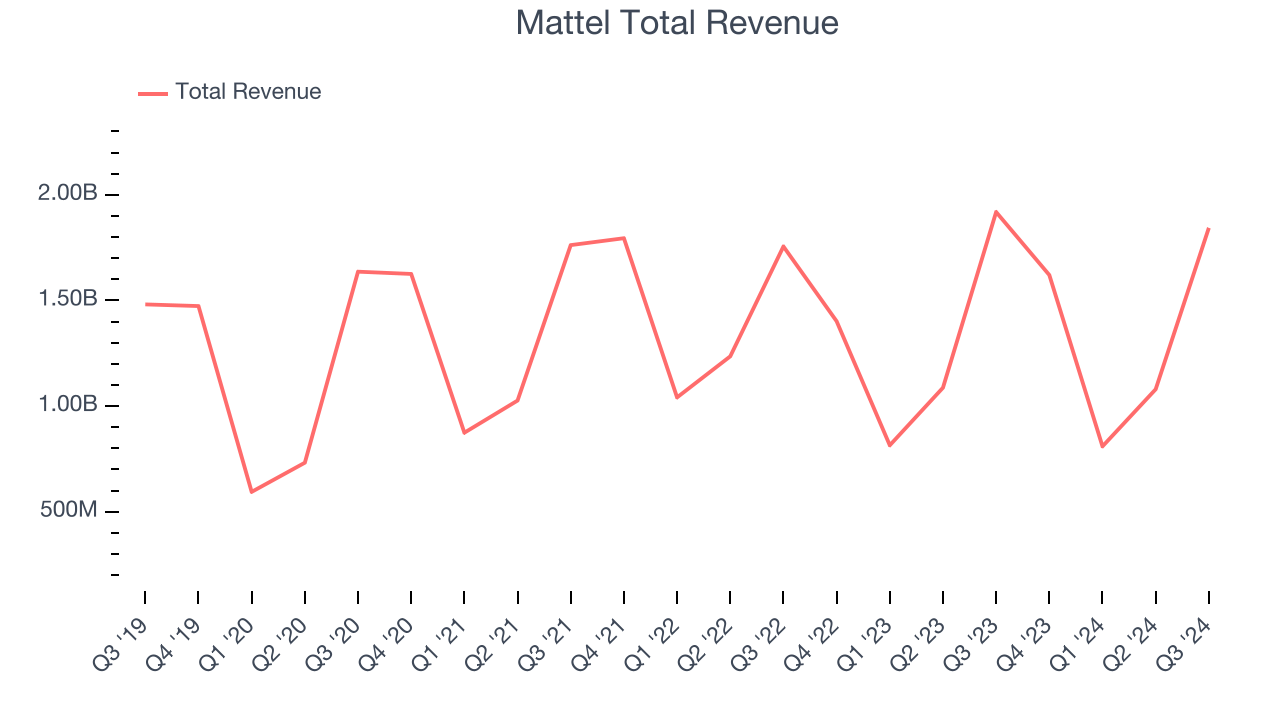

Mattel reported revenues of $1.84 billion, down 3.9% year on year. This print fell short of analysts’ expectations by 0.9%, but it was still a satisfactory quarter for the company with a solid beat of analysts’ EPS estimates.

Ynon Kreiz, Chairman and CEO of Mattel, said: “We continue to execute on our multi-year strategy to grow our IP-driven toy business and expand our entertainment offering. In line with our priorities this year, we continue to improve profitability, expand Gross Margin, and generate significant cash flow. We expect topline growth in the fourth quarter driven by a good holiday season, market share gains and a toyetic theatrical slate and are well positioned for long-term growth and shareholder value creation.”

Interestingly, the stock is up 6.7% since reporting and currently trades at $18.97.

Is now the time to buy Mattel? Access our full analysis of the earnings results here, it’s free.

Best Q3: Hasbro (NASDAQ: HAS)

Credited with the creation of toys such as Mr. Potato Head and the Rubik’s Cube, Hasbro (NASDAQ: HAS) is a global entertainment company offering a diverse range of toys, games, and multimedia experiences for children and families.

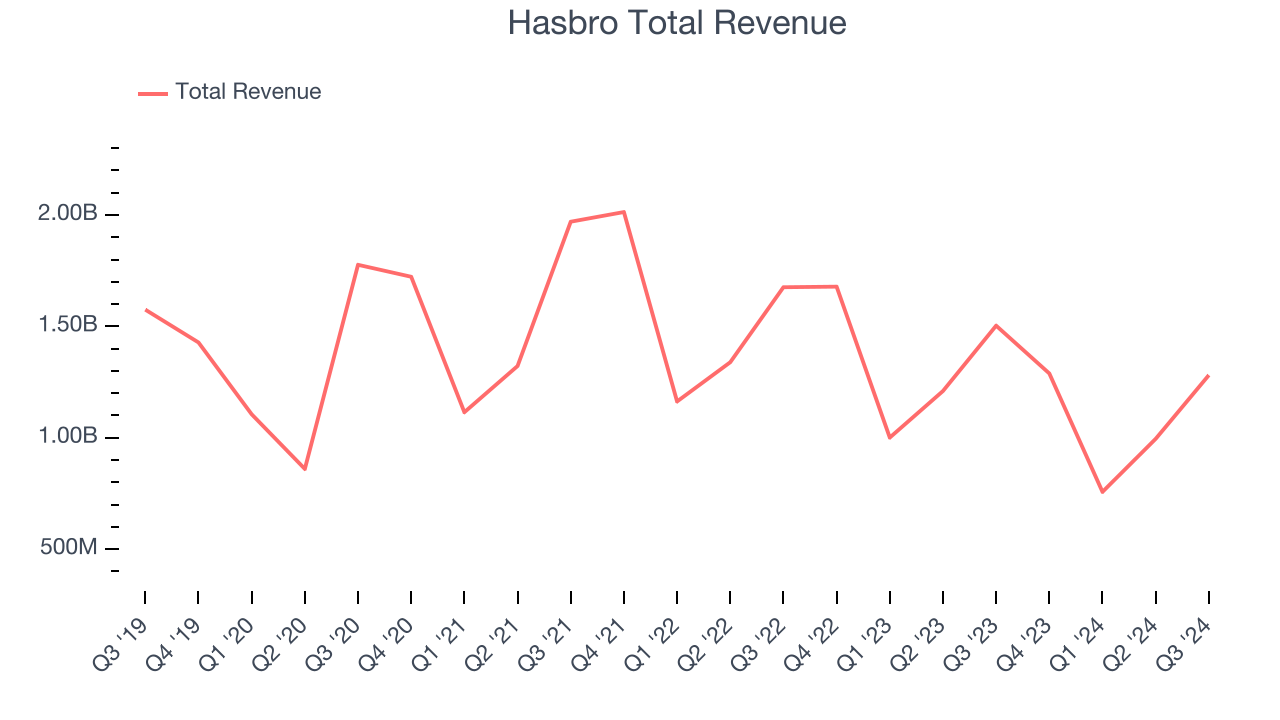

Hasbro reported revenues of $1.28 billion, down 14.8% year on year, falling short of analysts’ expectations by 1.3%. However, the business still had a strong quarter with an impressive beat of analysts’ EPS and EBITDA estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 10.3% since reporting. It currently trades at $63.12.

Is now the time to buy Hasbro? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Funko (NASDAQ: FNKO)

Boasting partnerships with media franchises like Marvel and One Piece, Funko (NASDAQ: FNKO) is a company specializing in creating and distributing licensed pop culture collectibles.

Funko reported revenues of $292.8 million, down 6.4% year on year, exceeding analysts’ expectations by 1.1%. Still, it was a mixed quarter as it posted full-year revenue guidance missing analysts’ expectations.

Funko delivered the biggest analyst estimates beat but had the weakest full-year guidance update in the group. As expected, the stock is down 3.5% since the results and currently trades at $11.77.

Read our full analysis of Funko’s results here.

Bark (NYSE: BARK)

Making a name for itself with the BarkBox, Bark (NYSE: BARK) specializes in subscription-based, personalized pet products.

Bark reported revenues of $126.1 million, up 2.5% year on year. This result surpassed analysts’ expectations by 0.7%. Zooming out, it was a mixed quarter as it also produced an impressive beat of analysts’ EPS estimates.

Bark delivered the fastest revenue growth and highest full-year guidance raise among its peers. The stock is up 48.6% since reporting and currently trades at $2.20.

Read our full, actionable report on Bark here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September, a quarter in November) have kept 2024 stock markets frothy, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there's still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.