Since July 2024, Watsco has been in a holding pattern, posting a small loss of 3.4% while floating around $465.36. The stock also fell short of the S&P 500’s 6.3% gain during that period.

Is now the time to buy Watsco, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.We're swiping left on Watsco for now. Here are three reasons why WSO doesn't excite us and a stock we'd rather own.

Why Is Watsco Not Exciting?

Originally a manufacturing company, Watsco (NYSE: WSO) today only distributes air conditioning, heating, and refrigeration equipment, as well as related parts and supplies.

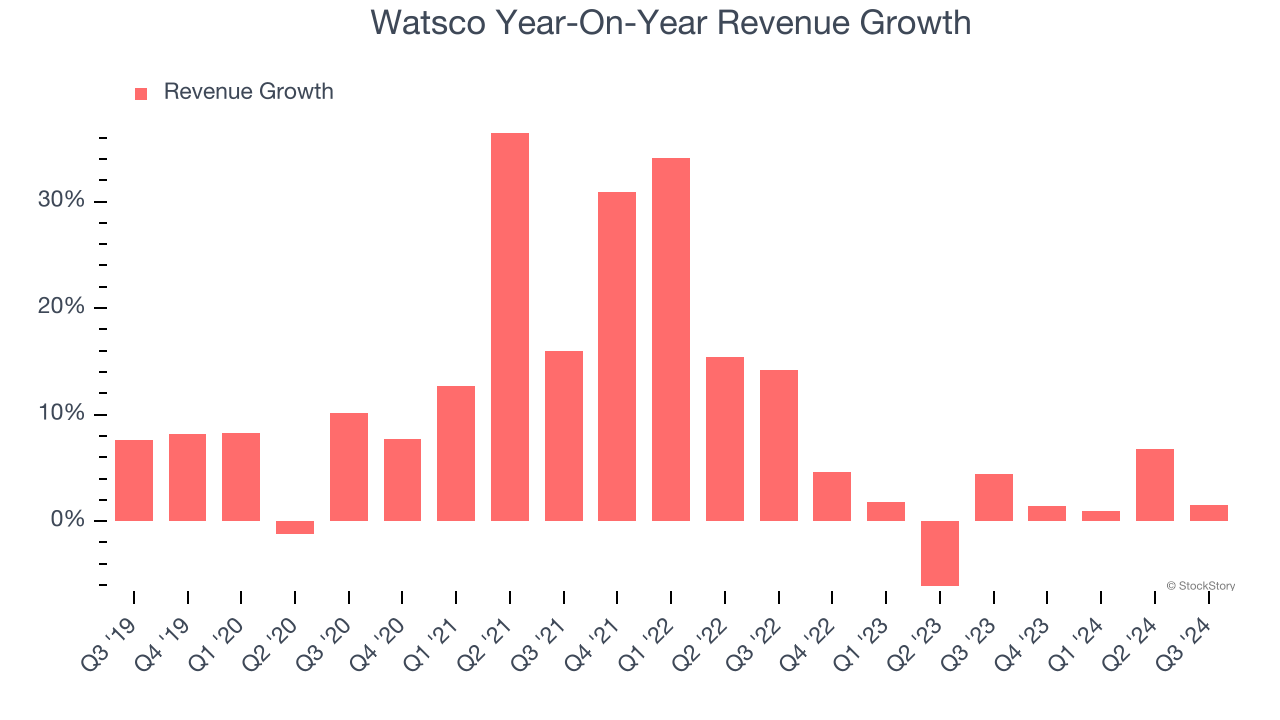

1. Lackluster Revenue Growth

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Watsco’s recent history shows its demand slowed as its annualized revenue growth of 1.8% over the last two years is below its five-year trend.

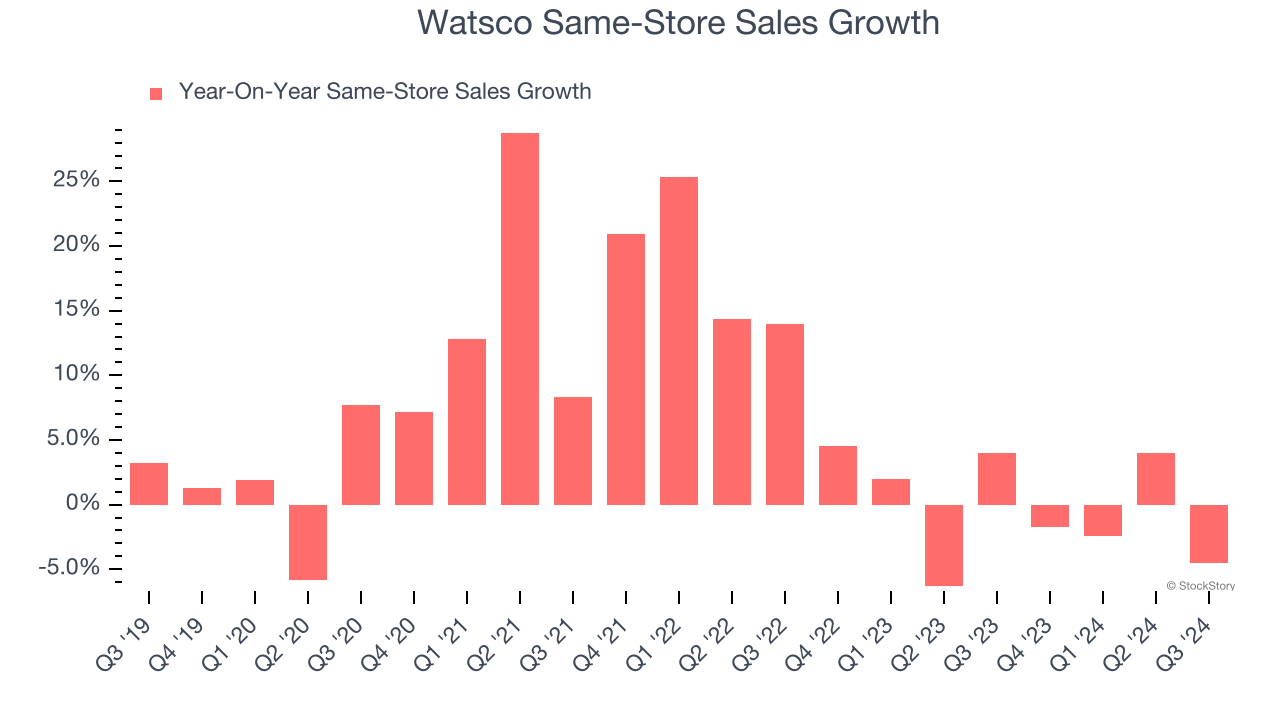

2. Flat Same-Store Sales Indicate Weak Demand

In addition to reported revenue, same-store sales are a useful data point for analyzing Infrastructure Distributors companies. This metric measures the change in sales at brick-and-mortar locations that have existed for at least a year, giving visibility into Watsco’s underlying demand characteristics.

Over the last two years, Watsco failed to grow its same-store sales. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Watsco might have to change its strategy and pricing, which can disrupt operations.

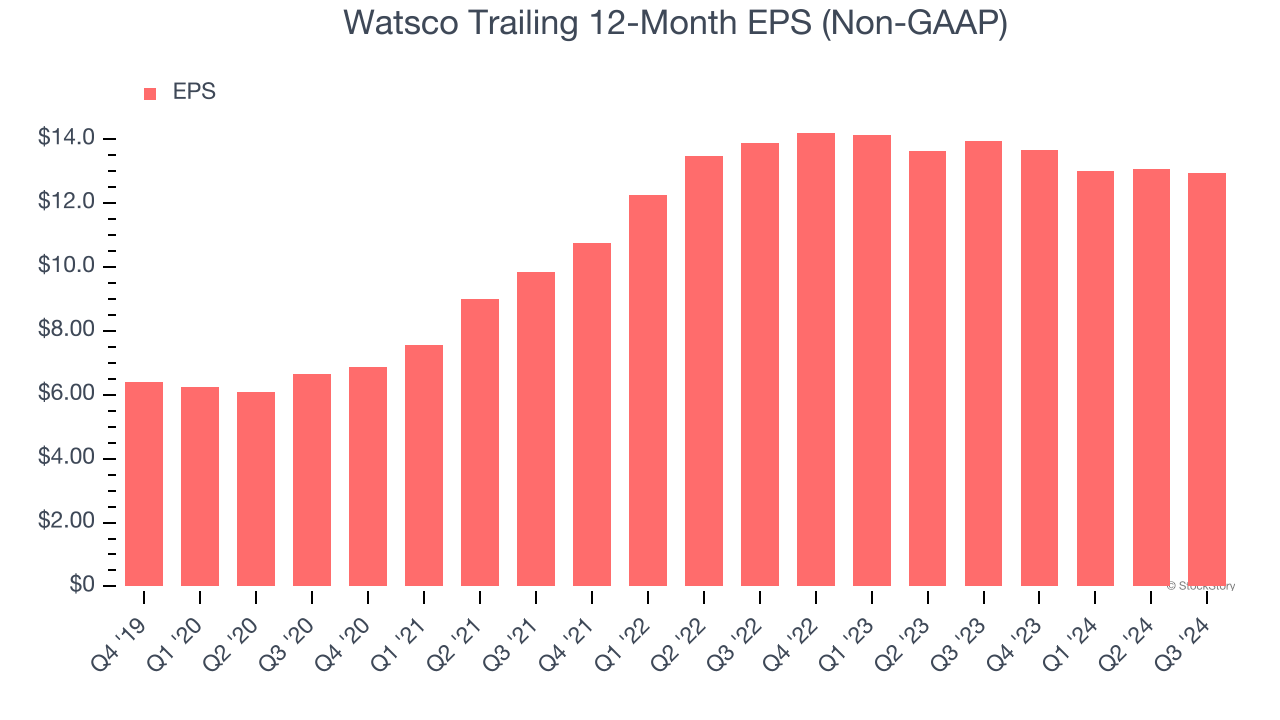

3. EPS Took a Dip Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Watsco, its EPS declined by 3.4% annually over the last two years while its revenue grew by 1.8%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Watsco isn’t a terrible business, but it doesn’t pass our bar. With its shares trailing the market in recent months, the stock trades at 30.6× forward price-to-earnings (or $465.36 per share). At this valuation, there’s a lot of good news priced in - we think there are better opportunities elsewhere. Let us point you toward CrowdStrike, the most entrenched endpoint security platform.

Stocks We Like More Than Watsco

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.