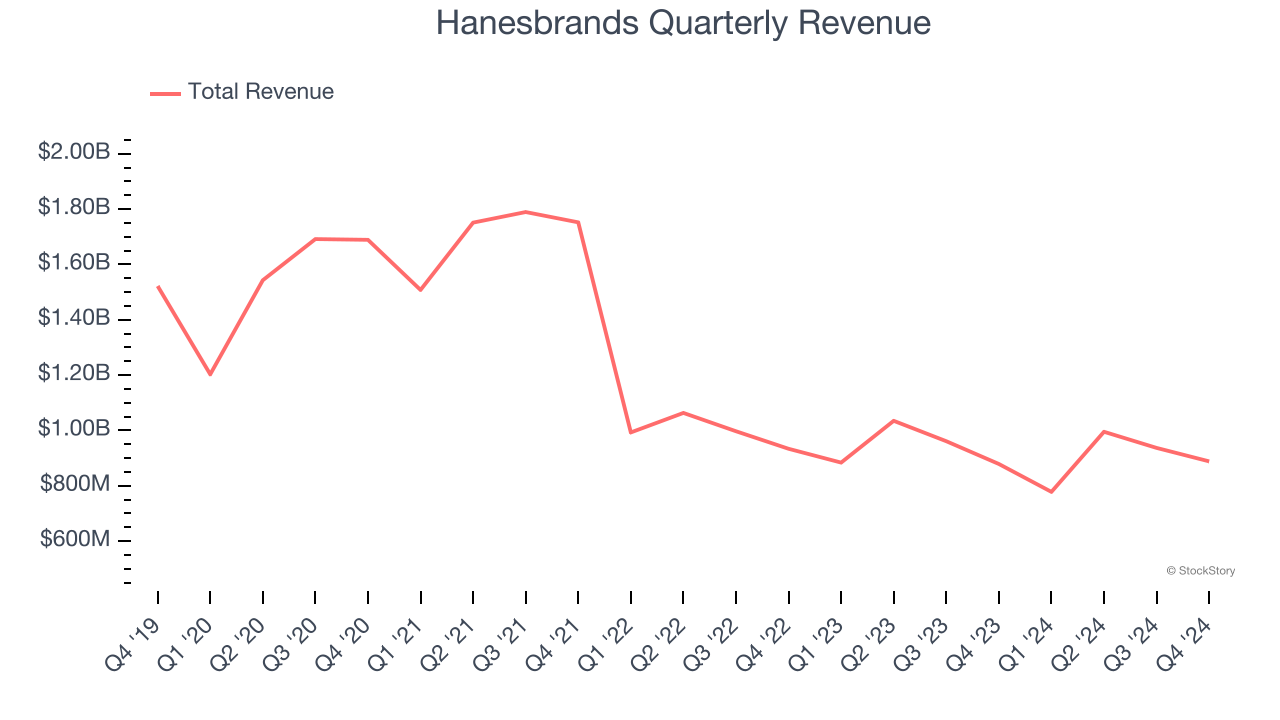

Clothing company Hanesbrands (NYSE: HBI) missed Wall Street’s revenue expectations in Q4 CY2024 as sales only rose 1.1% year on year to $888.5 million. Next quarter’s revenue guidance of $750 million underwhelmed, coming in 4.1% below analysts’ estimates. Its non-GAAP profit of $0.17 per share was 19.5% above analysts’ consensus estimates.

Is now the time to buy Hanesbrands? Find out by accessing our full research report, it’s free.

Hanesbrands (HBI) Q4 CY2024 Highlights:

- Revenue: $888.5 million vs analyst estimates of $899.4 million (1.1% year-on-year growth, 1.2% miss)

- Adjusted EPS: $0.17 vs analyst estimates of $0.14 (19.5% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $3.50 billion at the midpoint, missing analyst estimates by 3.8% and implying -2.9% growth (vs -4.3% in FY2024)

- Adjusted EPS guidance for the upcoming financial year 2025 is $0.53 at the midpoint, beating analyst estimates by 2.2%

- Operating Margin: 13.5%, up from 11.1% in the same quarter last year

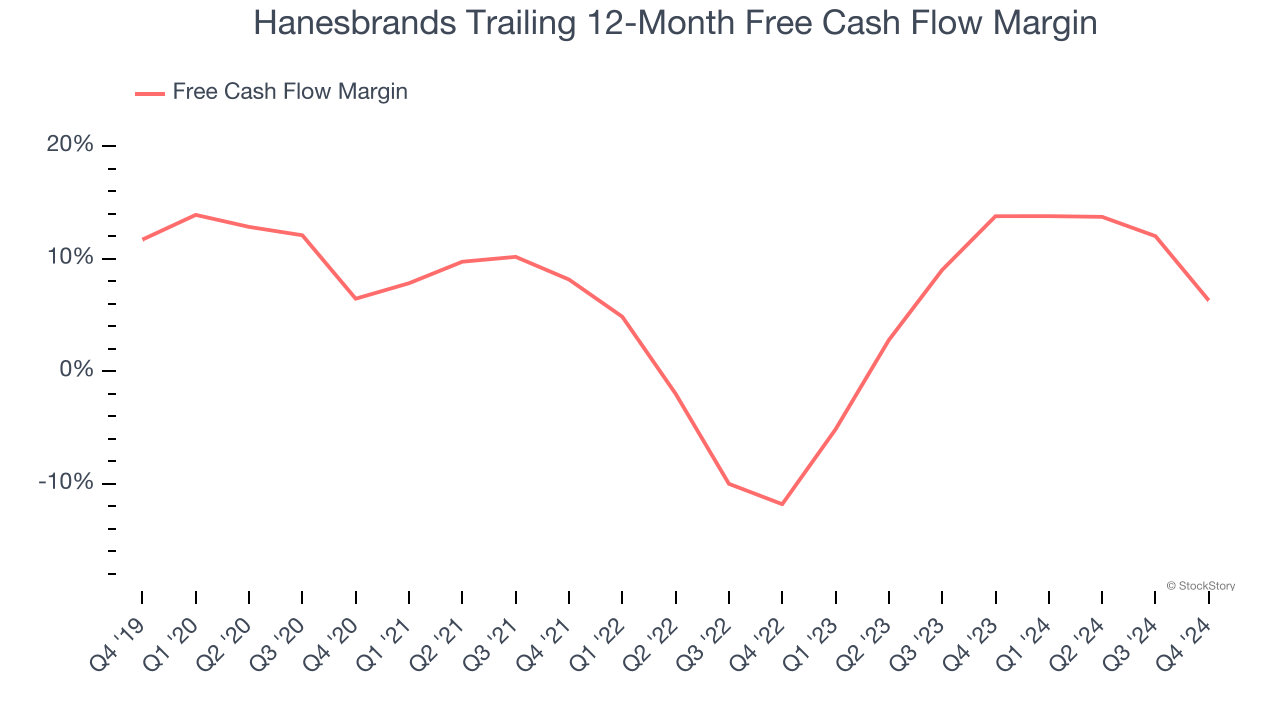

- Free Cash Flow Margin: 6.9%, down from 30.3% in the same quarter last year

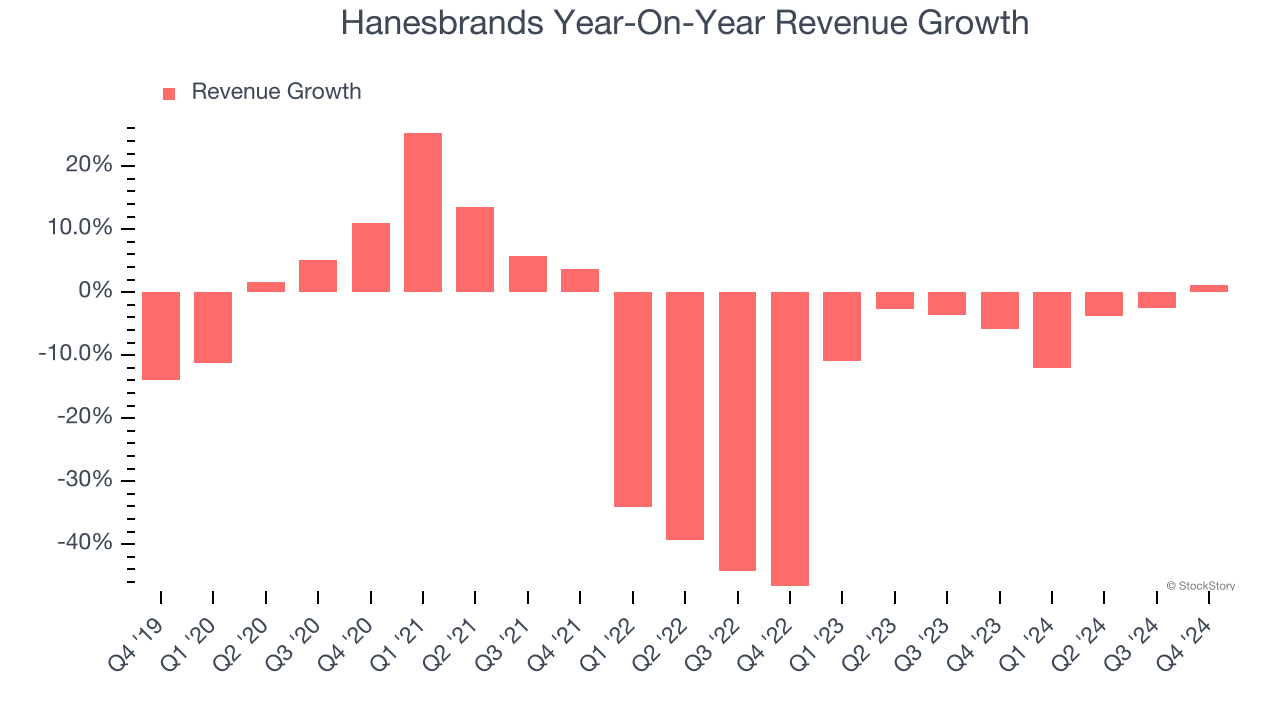

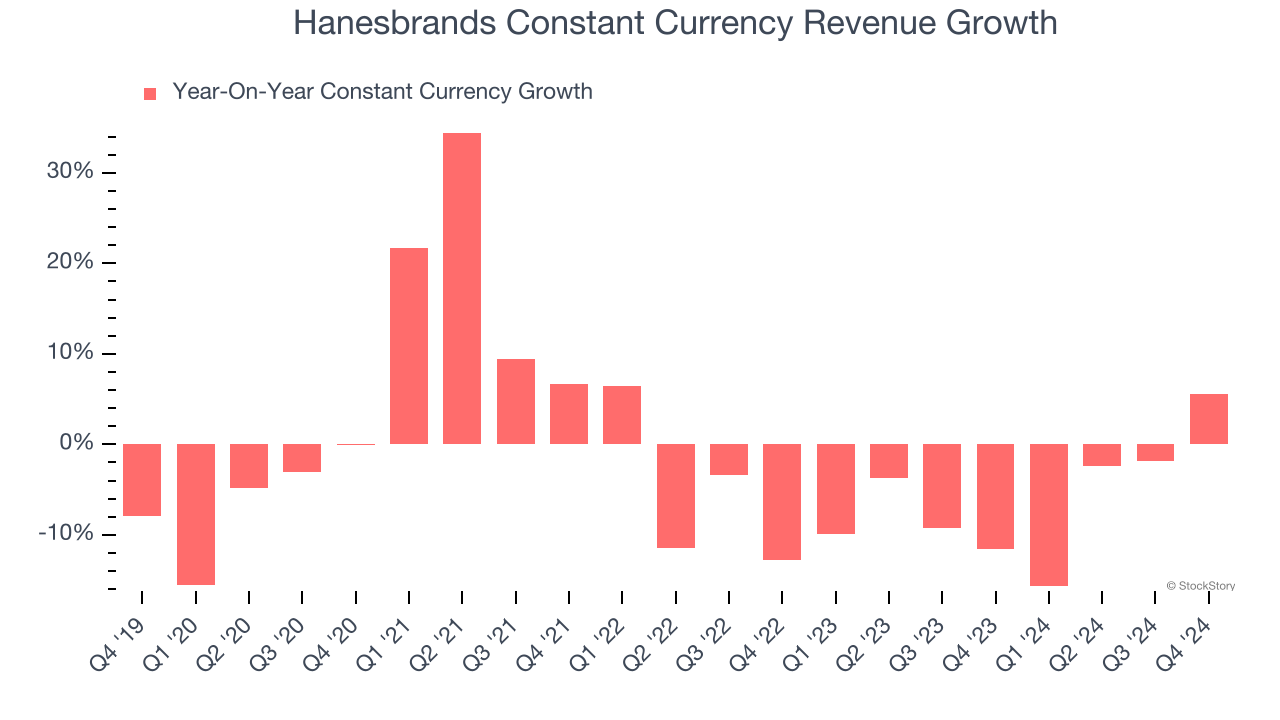

- Constant Currency Revenue rose 5.6% year on year (-11.6% in the same quarter last year)

- Market Capitalization: $2.70 billion

“We delivered a strong quarter and full-year with results across all key metrics exceeding our expectations as the benefits of our transformation strategy are clearly working,” said Steve Bratspies, CEO.

Company Overview

A classic American staple founded in 1901, Hanesbrands (NYSE: HBI) is a clothing company known for its array of basic apparel including innerwear and activewear.

Apparel and Accessories

Thanks to social media and the internet, not only are styles changing more frequently today than in decades past but also consumers are shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel and accessories companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Hanesbrands’s demand was weak over the last five years as its sales fell at a 9.7% annual rate. This was below our standards and is a sign of poor business quality.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Hanesbrands’s annualized revenue declines of 5% over the last two years suggest its demand continued shrinking.

We can dig further into the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 6.1% year-on-year declines. Because this number aligns with its normal revenue growth, we can see Hanesbrands’s foreign exchange rates have been steady.

This quarter, Hanesbrands’s revenue grew by 1.1% year on year to $888.5 million, falling short of Wall Street’s estimates. Company management is currently guiding for a 3.6% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Hanesbrands has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.1% over the last two years, slightly better than the broader consumer discretionary sector.

Hanesbrands’s free cash flow clocked in at $61.72 million in Q4, equivalent to a 6.9% margin. The company’s cash profitability regressed as it was 23.3 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Key Takeaways from Hanesbrands’s Q4 Results

Although Hanesbrands missed analysts' revenue estimates this quarter, it beat their constant currency revenue expectations. We were also glad its EPS outperformed. On the other hand, its full-year revenue guidance missed significantly and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 3.5% to $7.40 immediately after reporting.

Hanesbrands underperformed this quarter, but does that create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.