Looking back on medical devices & supplies - specialty stocks’ Q4 earnings, we examine this quarter’s best and worst performers, including Globus Medical (NYSE: GMED) and its peers.

The medical devices industry operates a business model that balances steady demand with significant investments in innovation and regulatory compliance. The industry benefits from recurring revenue streams tied to consumables, maintenance services, and incremental upgrades to the latest technologies, although specialty devices are more niche. The capital-intensive nature of product development, coupled with lengthy regulatory pathways and the need for clinical validation, can weigh on profitability and timelines. In addition, there are constant pricing pressures from healthcare systems and insurers maximizing cost efficiency. Over the next several years, one tailwind is demographic–aging populations means rising chronic disease rates that drive greater demand for medical interventions and monitoring solutions. Advances in digital health, such as remote patient monitoring and smart devices, are also expected to unlock new demand by shortening upgrade cycles. On the other hand, the industry faces headwinds from pricing and reimbursement pressures as healthcare providers increasingly adopt value-based care models. Additionally, the integration of cybersecurity for connected devices adds further risk and complexity for device manufacturers.

The 6 medical devices & supplies - specialty stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 0.8%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 11.1% since the latest earnings results.

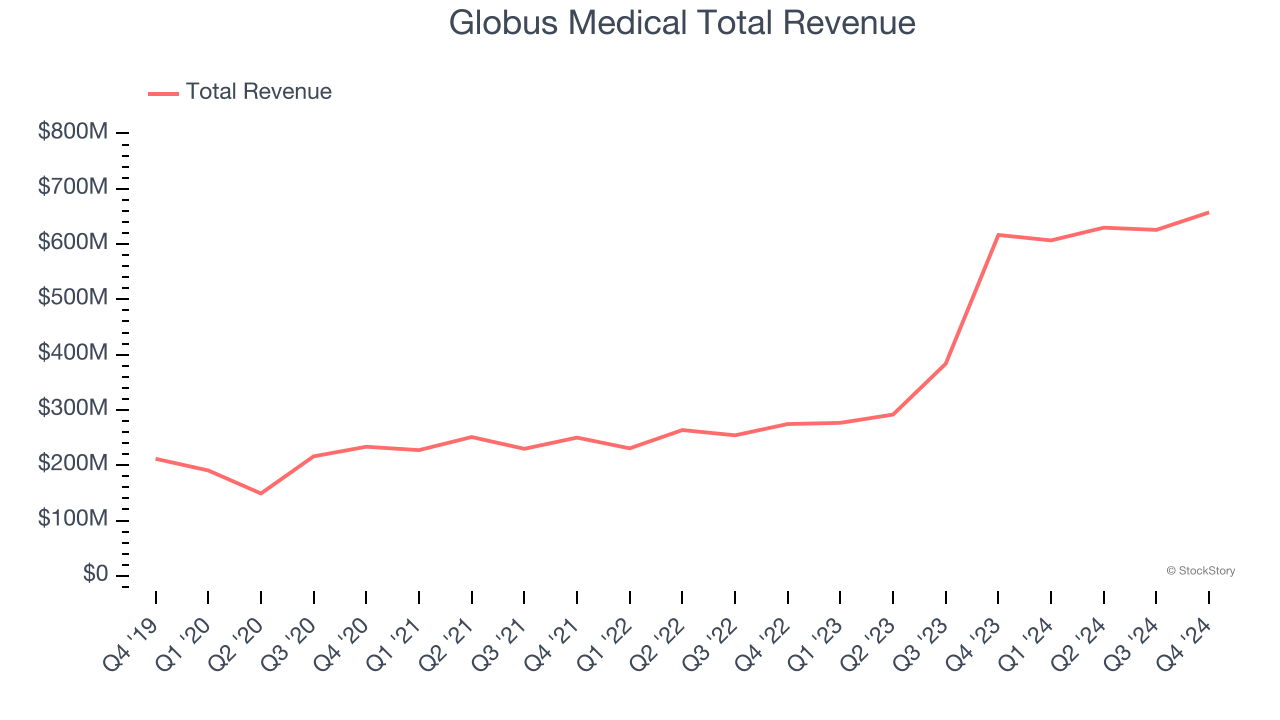

Globus Medical (NYSE: GMED)

Founded in 2003, Globus Medical (NYSE: GMED) develops and manufactures medical devices and solutions for musculoskeletal disorders, with a focus on products for spine surgery, orthopedic trauma, and joint reconstruction.

Globus Medical reported revenues of $657.3 million, up 6.6% year on year. This print exceeded analysts’ expectations by 1.9%. Overall, it was a strong quarter for the company with an impressive beat of analysts’ EPS estimates and a narrow beat of analysts’ constant currency revenue estimates.

“I’m proud of our team at Globus Medical, delivering incredible results for 2024. We made significant progress integrating the business and creating a strong foundation for future growth while remaining focused on improving patient outcomes. Our spine sales force is the most dedicated and talented team in the market. Our innovation engine delivered a record amount of new product launches in 2024 and remains unmatched in our industry.” said Dan Scavilla, President and CEO.

Globus Medical pulled off the biggest analyst estimates beat of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 10.2% since reporting and currently trades at $75.51.

Is now the time to buy Globus Medical? Access our full analysis of the earnings results here, it’s free.

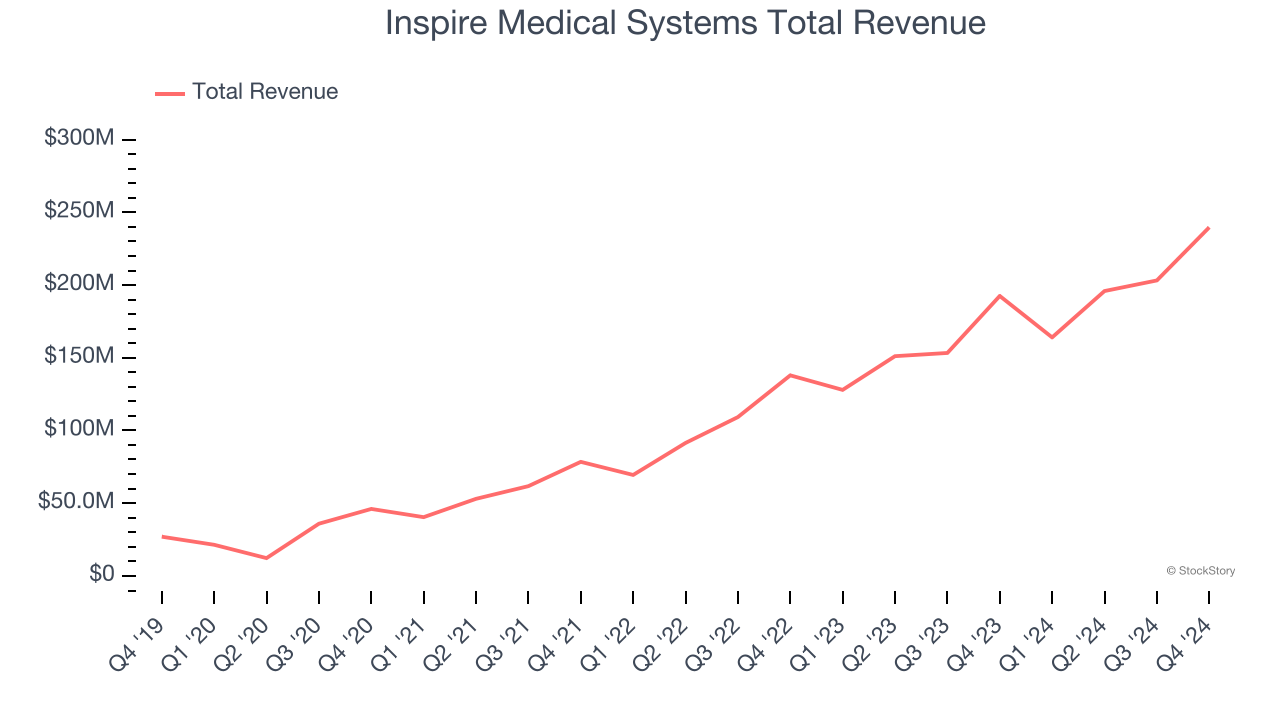

Best Q4: Inspire Medical Systems (NYSE: INSP)

Founded in 2007, Inspire Medical Systems (NYSE: INSP) develops and markets products for obstructive sleep apnea (OSA), with its flagship product being a neurostimulation system designed to improve breathing during sleep.

Inspire Medical Systems reported revenues of $239.7 million, up 24.5% year on year, outperforming analysts’ expectations by 0.9%. The business had a very strong quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ full-year EPS guidance estimates.

Inspire Medical Systems scored the fastest revenue growth among its peers. However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $179.86.

Is now the time to buy Inspire Medical Systems? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Haemonetics (NYSE: HAE)

Founded in 1971, Haemonetics Corporation (NYSE: HAE) offers products for plasma collection, blood donation, and surgical and critical care.

Haemonetics reported revenues of $348.5 million, up 3.7% year on year, falling short of analysts’ expectations by 1.3%. It was a slower quarter as it posted organic revenue in line with analysts’ estimates.

Haemonetics delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 4.6% since the results and currently trades at $68.

Read our full analysis of Haemonetics’s results here.

Bausch + Lomb (NYSE: BLCO)

Founded in 1853, Bausch + Lomb (NYSE: BLCO) is a global healthcare company specializing in eye health products, including contact lenses, lens care products, surgical instruments, and pharmaceuticals for ocular conditions.

Bausch + Lomb reported revenues of $1.28 billion, up 9.1% year on year. This number beat analysts’ expectations by 1.8%. Aside from that, it was a mixed quarter as it also produced a decent beat of analysts’ EPS estimates but full-year revenue guidance slightly missing analysts’ expectations.

Bausch + Lomb had the weakest full-year guidance update among its peers. The stock is down 20.4% since reporting and currently trades at $13.01.

Read our full, actionable report on Bausch + Lomb here, it’s free.

Enovis (NYSE: ENOV)

Originally founded in 1995 as diversified industrial company Colfax Corporation, Enovis Corporation (NYSE: ENOV) focuses on medical technology for orthopedic care, rehabilitation, and surgical products.

Enovis reported revenues of $561 million, up 23.3% year on year. This print surpassed analysts’ expectations by 1%. Taking a step back, it was a mixed quarter as it also logged a decent beat of analysts’ EPS estimates but full-year revenue guidance slightly missing analysts’ expectations.

The stock is down 15.7% since reporting and currently trades at $35.52.

Read our full, actionable report on Enovis here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.