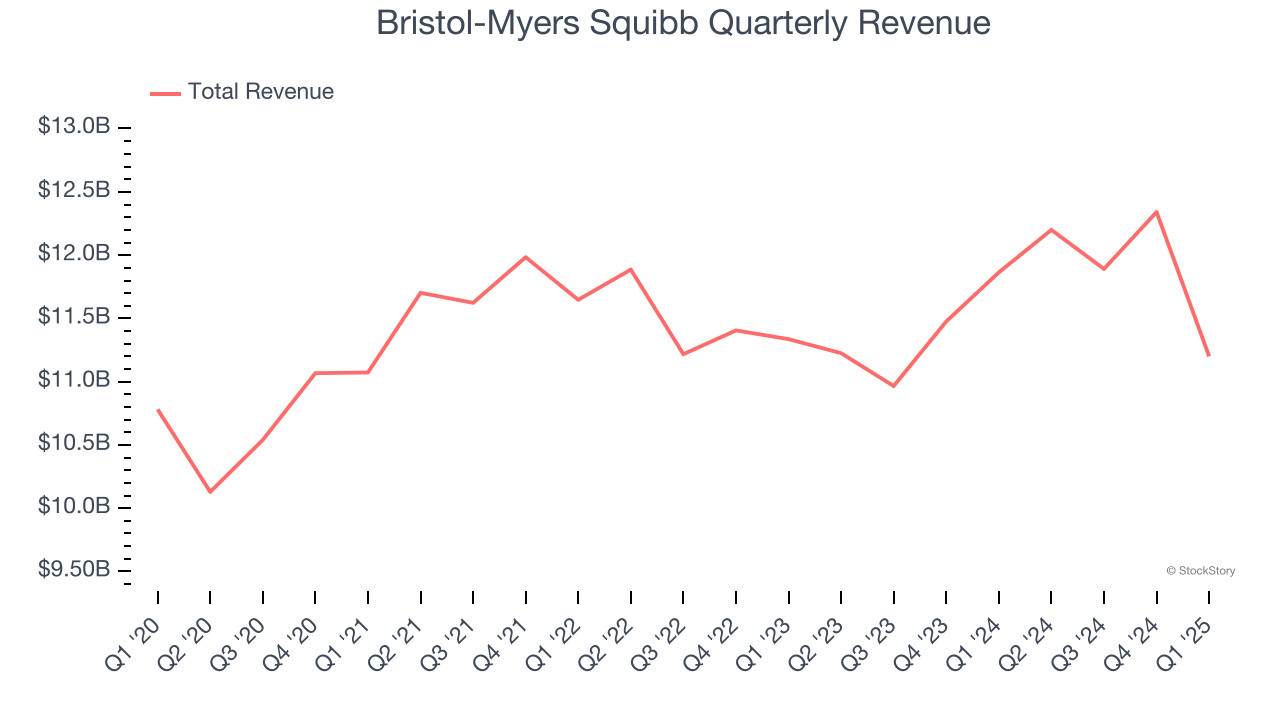

Biopharmaceutical company Bristol Myers Squibb (NYSE: BMY) reported revenue ahead of Wall Street’s expectations in Q1 CY2025, but sales fell by 5.6% year on year to $11.2 billion. The company’s full-year revenue guidance of $46.3 billion at the midpoint came in 1.2% above analysts’ estimates. Its non-GAAP profit of $1.80 per share was 19.9% above analysts’ consensus estimates.

Is now the time to buy Bristol-Myers Squibb? Find out by accessing our full research report, it’s free.

Bristol-Myers Squibb (BMY) Q1 CY2025 Highlights:

- Revenue: $11.2 billion vs analyst estimates of $10.78 billion (5.6% year-on-year decline, 3.9% beat)

- Adjusted EPS: $1.80 vs analyst estimates of $1.50 (19.9% beat)

- The company lifted its revenue guidance for the full year to $46.3 billion at the midpoint from $45.5 billion, a 1.8% increase

- Management raised its full-year Adjusted EPS guidance to $6.85 at the midpoint, a 2.2% increase

- Market Capitalization: $98.75 billion

“Our strong execution in the first quarter drove continued momentum across our Growth Portfolio and meaningful progress in the pipeline,” said Christopher Boerner, Ph.D., board chair and CEO, Bristol Myers Squibb.

Company Overview

With roots dating back to 1887 and a transformative merger in 1989 that gave the company its current name, Bristol-Myers Squibb (NYSE: BMY) discovers, develops, and markets prescription medications for serious diseases including cancer, blood disorders, immunological conditions, and cardiovascular diseases.

Branded Pharmaceuticals

The branded pharmaceutical industry relies on a high-cost, high-reward business model, driven by substantial investments in research and development to create innovative, patent-protected drugs. Successful products can generate significant revenue streams over their patent life, and the larger a roster of drugs, the stronger a moat a company enjoys. However, the business model is inherently risky, with high failure rates during clinical trials, lengthy regulatory approval processes, and intense competition from generic and biosimilar manufacturers once patents expire. These challenges, combined with scrutiny over drug pricing, create a complex operating environment. Looking ahead, the industry is positioned for tailwinds from advancements in precision medicine, increasing adoption of AI to enhance drug development efficiency, and growing global demand for treatments addressing chronic and rare diseases. However, headwinds include heightened regulatory scrutiny, pricing pressures from governments and insurers, and the looming patent cliffs for key blockbuster drugs. Patent cliffs bring about competition from generics, forcing branded pharmaceutical companies back to the drawing board to find the next big thing.

Sales Growth

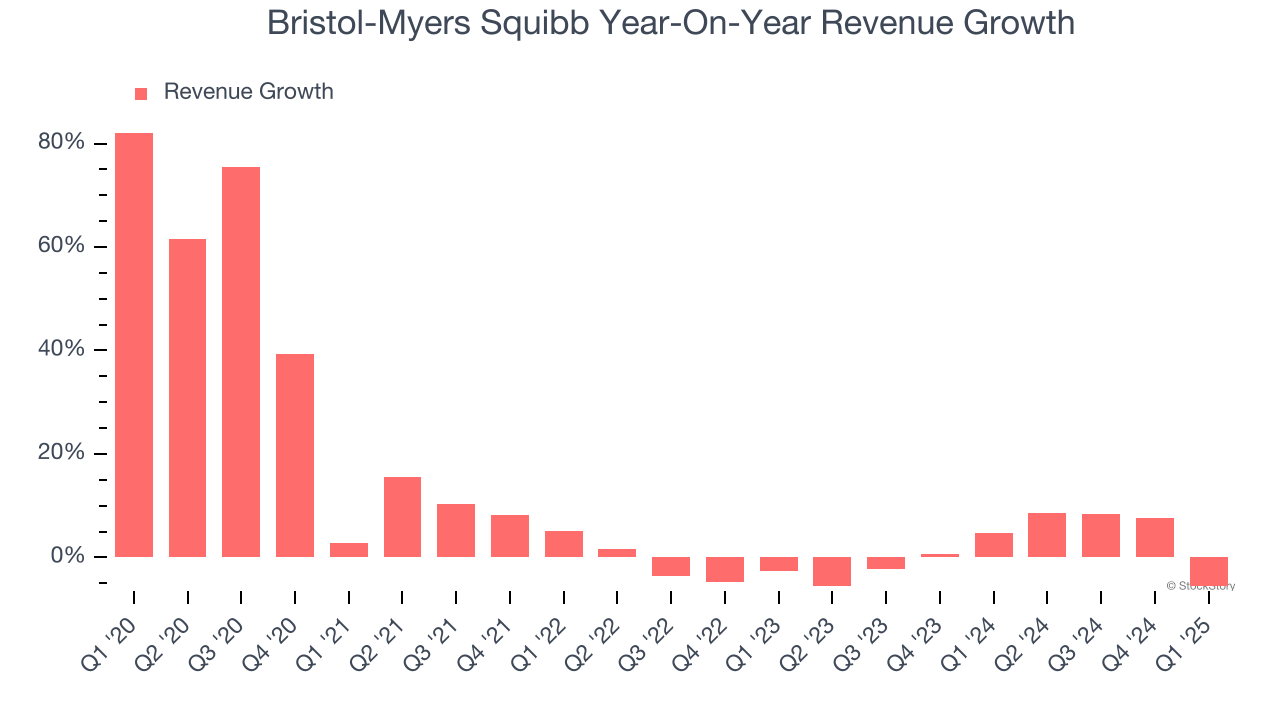

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Bristol-Myers Squibb’s sales grew at a decent 9% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Bristol-Myers Squibb’s recent performance shows its demand has slowed as its annualized revenue growth of 1.9% over the last two years was below its five-year trend.

Bristol-Myers Squibb also breaks out the revenue for its most important segment, Growth Portfolio. Over the last two years, Bristol-Myers Squibb’s Growth Portfolio revenue averaged 17.5% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, Bristol-Myers Squibb’s revenue fell by 5.6% year on year to $11.2 billion but beat Wall Street’s estimates by 3.9%.

Looking ahead, sell-side analysts expect revenue to decline by 5.4% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

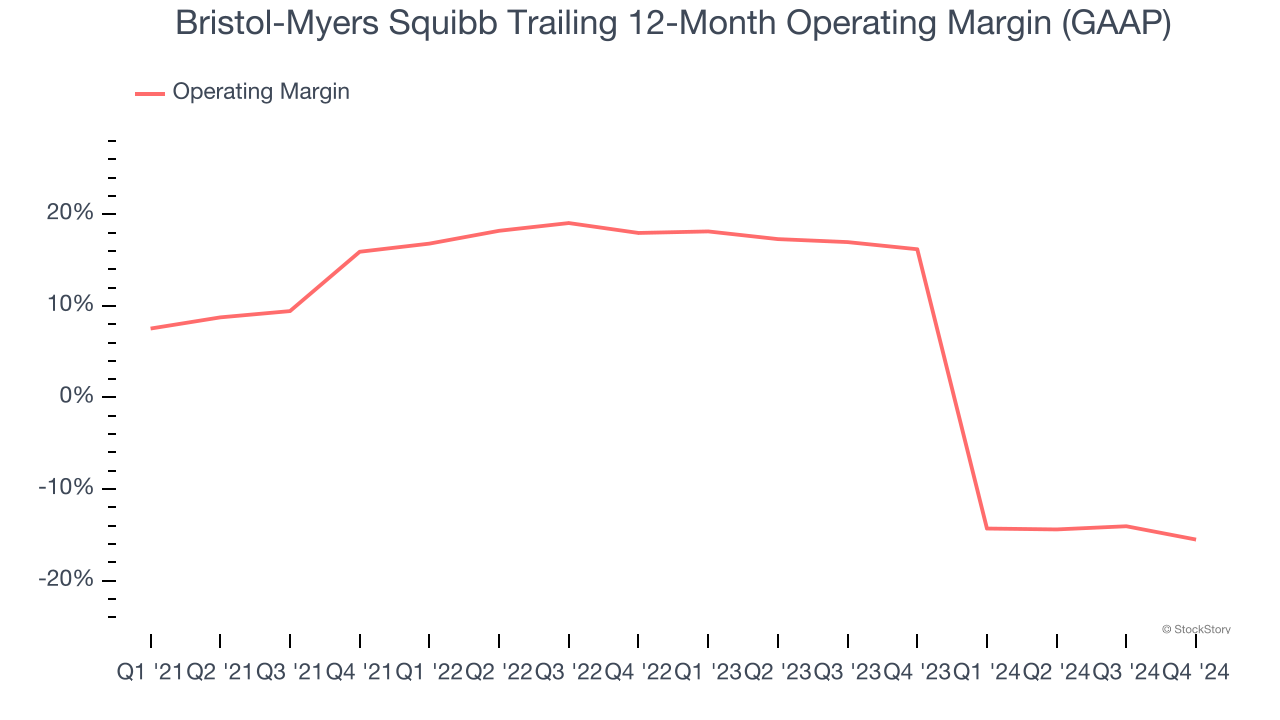

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Bristol-Myers Squibb was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.7% was weak for a healthcare business.

On the plus side, Bristol-Myers Squibb’s operating margin rose by 6.4 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming into its more recent performance, however, we can see the company’s margin has decreased by 6.4 percentage points on a two-year basis. If Bristol-Myers Squibb wants to pass our bar, it must prove it can expand its profitability consistently.

in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

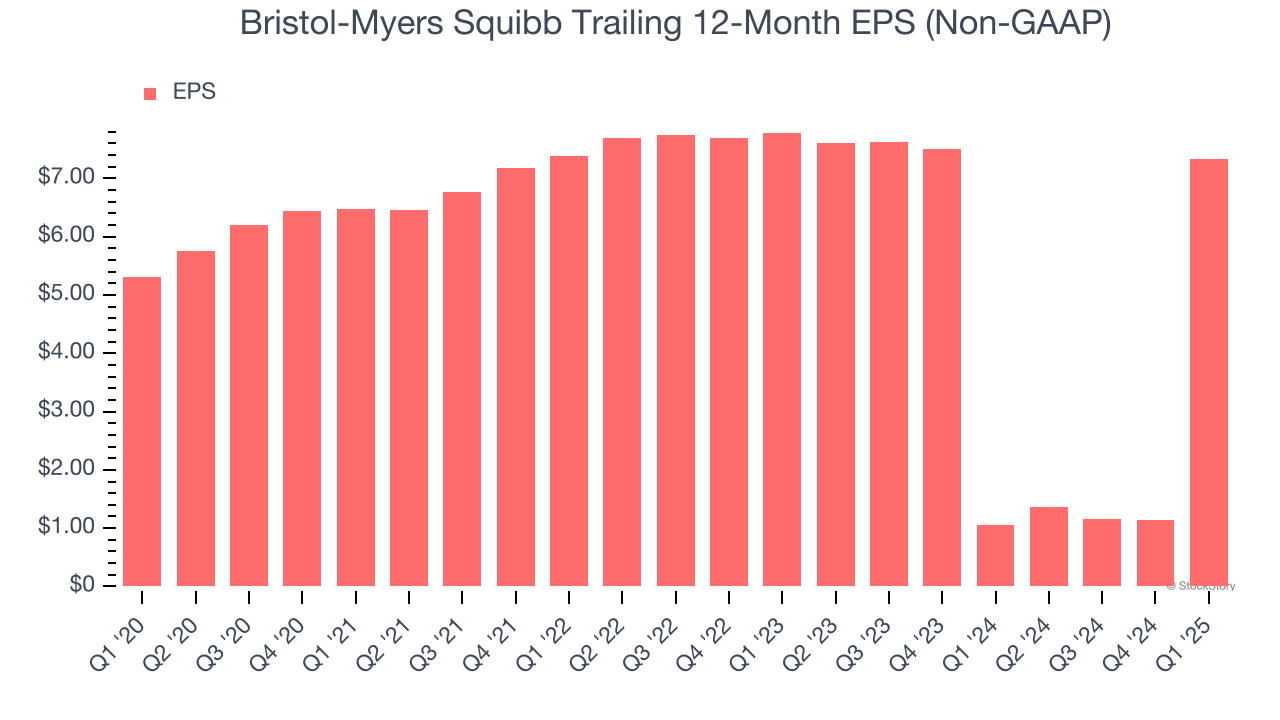

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Bristol-Myers Squibb’s EPS grew at a decent 6.7% compounded annual growth rate over the last five years. Despite its operating margin expansion and share repurchases during that time, this performance was lower than its 9% annualized revenue growth, telling us the delta came from reduced interest expenses or taxes.

In Q1, Bristol-Myers Squibb reported EPS at $1.80, up from negative $4.40 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Bristol-Myers Squibb’s full-year EPS of $7.34 to shrink by 9.6%.

Key Takeaways from Bristol-Myers Squibb’s Q1 Results

We enjoyed seeing Bristol-Myers Squibb beat analysts’ revenue and EPS expectations this quarter. We were also glad it lifted its full-year guidance for both metrics. Zooming out, we think this was a solid "beat-and-raise" quarter. The stock traded up 1.3% to $49.12 immediately following the results.

Bristol-Myers Squibb may have had a good quarter, but does that mean you should invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.