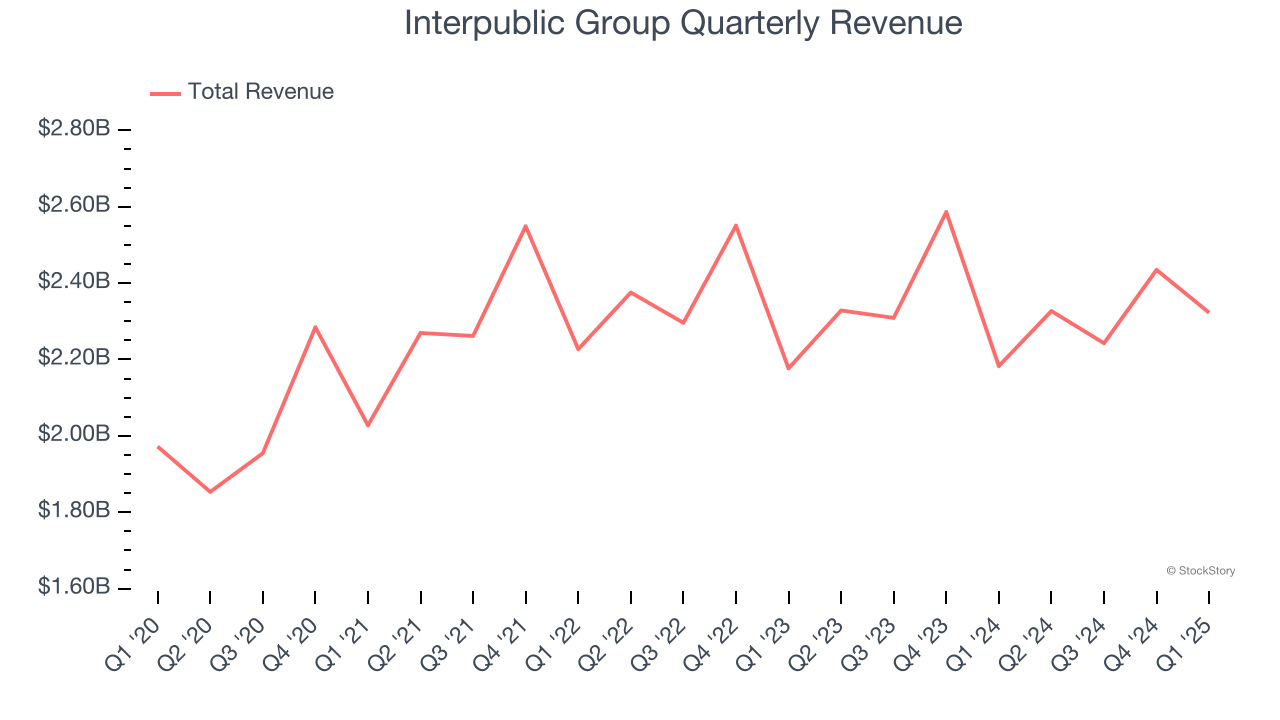

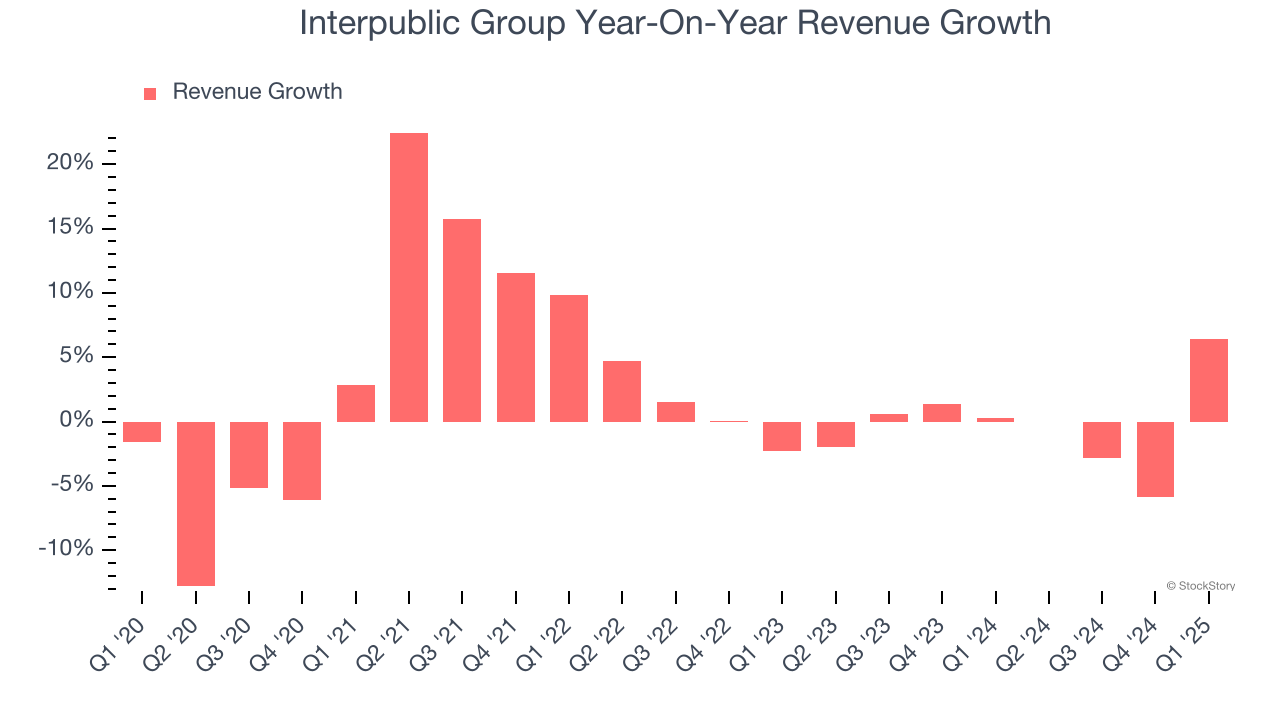

Global advertising conglomerate Interpublic Group (NYSE: IPG) announced better-than-expected revenue in Q1 CY2025, with sales up 6.4% year on year to $2.32 billion. Its non-GAAP profit of $0.33 per share was 26.9% above analysts’ consensus estimates.

Is now the time to buy Interpublic Group? Find out by accessing our full research report, it’s free.

Interpublic Group (IPG) Q1 CY2025 Highlights:

- Revenue: $2.32 billion vs analyst estimates of $2.00 billion (6.4% year-on-year growth, 15.8% beat)

- Adjusted EPS: $0.33 vs analyst estimates of $0.26 (26.9% beat)

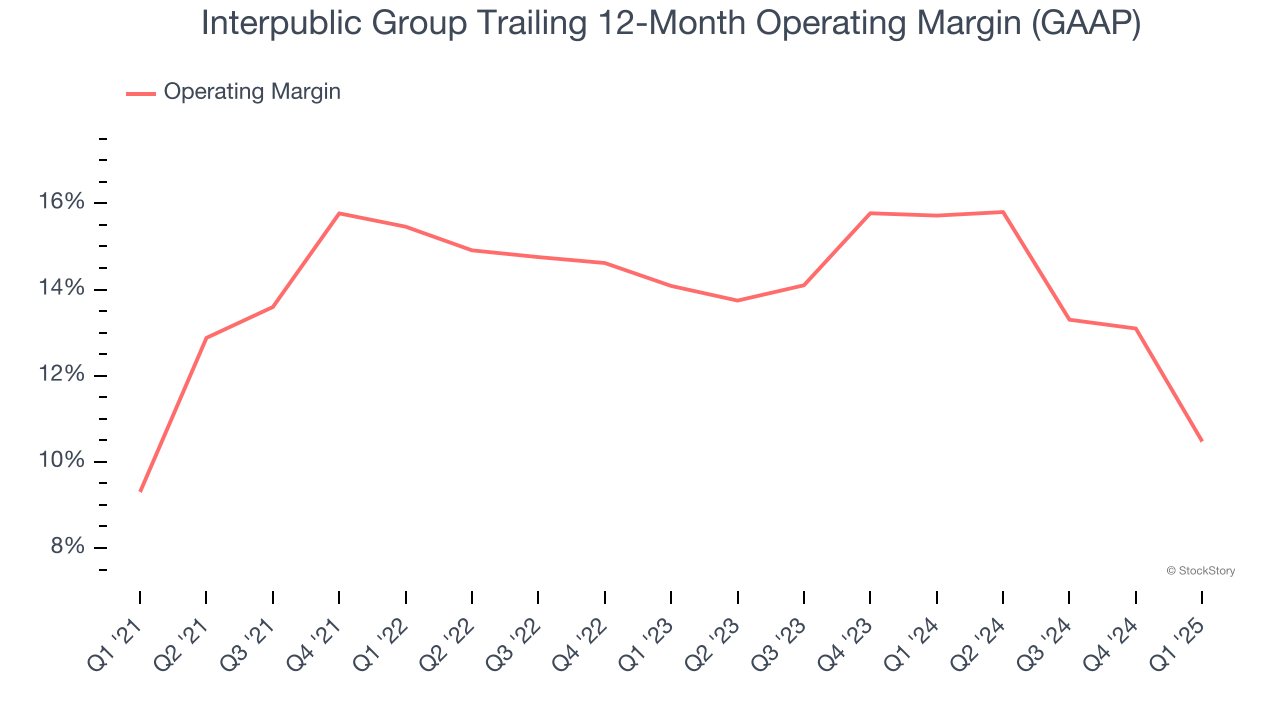

- Operating Margin: -1.8%, down from 8.4% in the same quarter last year

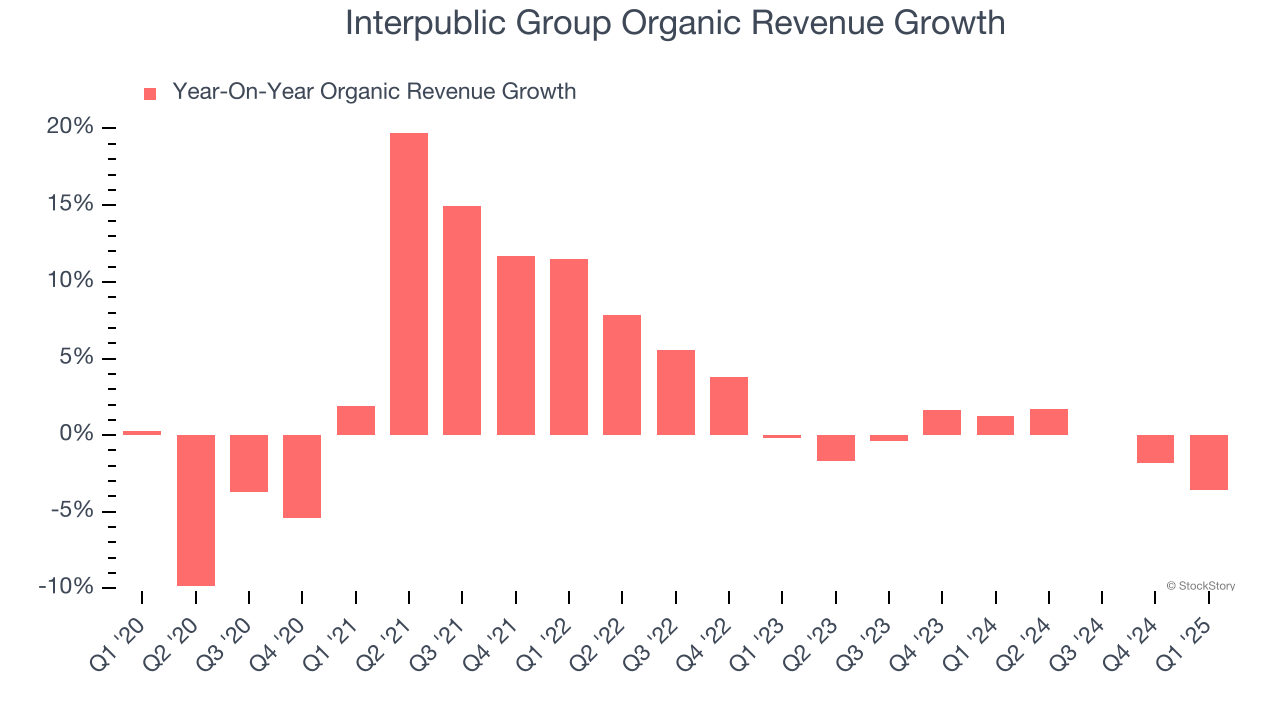

- Organic Revenue fell 3.6% year on year (1.3% in the same quarter last year)

- Market Capitalization: $8.94 billion

Company Overview

With a history dating back to 1902 and roots in the McCann-Erickson agency, Interpublic Group (NYSE: IPG) is a marketing and communications holding company that owns agencies specializing in advertising, media buying, public relations, and digital marketing services.

Advertising & Marketing Services

The sector is on the precipice of both disruption and growth as AI, programmatic advertising, and data-driven marketing reshape how things are done. For example, the advent of the Internet broadly and programmatic advertising specifically means that brand building is not a relationship business anymore but instead one based on data and technology, which could hurt traditional ad agencies. On the other hand, the companies in the sector that beef up their tech chops by automating the buying of ad inventory or facilitating omnichannel marketing, for example, stand to benefit. With or without advances in digitization and AI, the sector is still highly levered to the macro, and economic uncertainty may lead to fluctuating ad spend, particularly in cyclical industries.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $9.33 billion in revenue over the past 12 months, Interpublic Group is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s challenging to maintain high growth rates when you’ve already captured a large portion of the addressable market. To accelerate sales, Interpublic Group likely needs to optimize its pricing or lean into new offerings and international expansion.

As you can see below, Interpublic Group grew its sales at a sluggish 1.7% compounded annual growth rate over the last five years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Interpublic Group’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Interpublic Group’s organic revenue was flat. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Interpublic Group reported year-on-year revenue growth of 6.4%, and its $2.32 billion of revenue exceeded Wall Street’s estimates by 15.8%.

Looking ahead, sell-side analysts expect revenue to decline by 6.7% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Interpublic Group has managed its cost base well over the last five years. It demonstrated solid profitability for a business services business, producing an average operating margin of 13.1%.

Looking at the trend in its profitability, Interpublic Group’s operating margin rose by 1.2 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Interpublic Group generated an operating profit margin of negative 1.8%, down 10.2 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

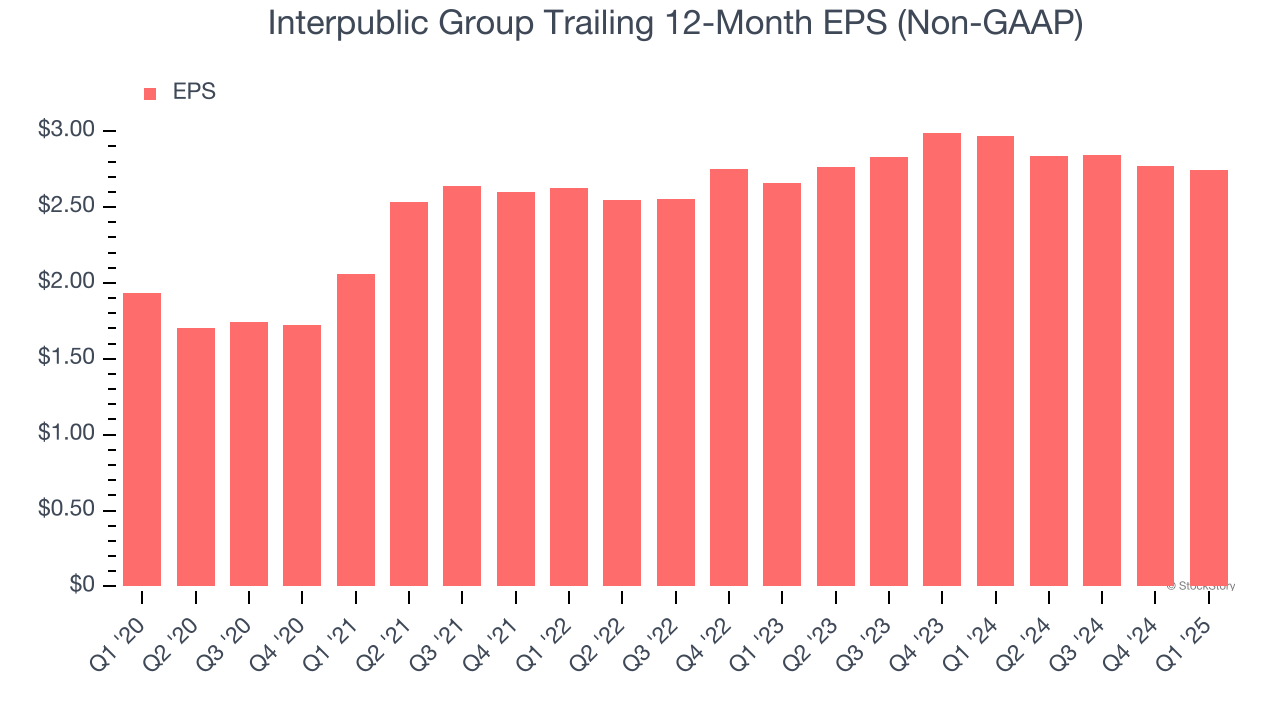

Interpublic Group’s EPS grew at an unimpressive 7.3% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 1.7% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

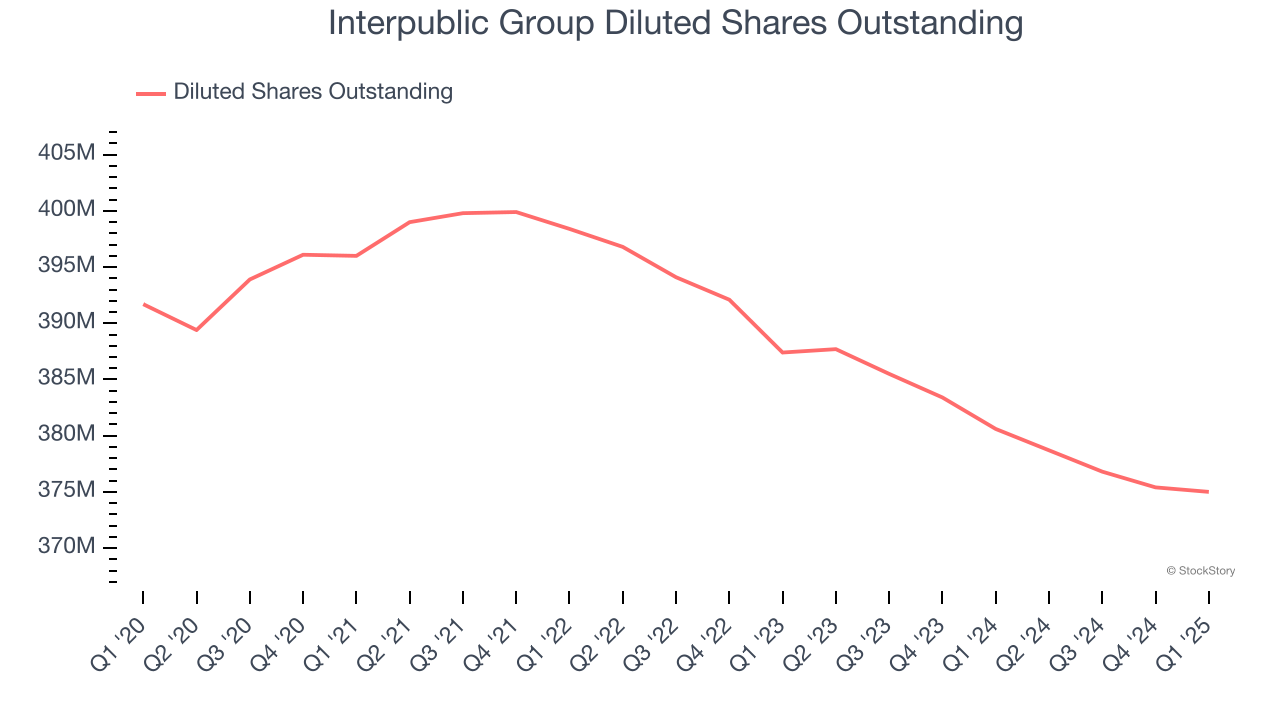

Diving into the nuances of Interpublic Group’s earnings can give us a better understanding of its performance. As we mentioned earlier, Interpublic Group’s operating margin declined this quarter but expanded by 1.2 percentage points over the last five years. Its share count also shrank by 4.3%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q1, Interpublic Group reported EPS at $0.33, down from $0.36 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Interpublic Group’s full-year EPS of $2.74 to shrink by 2%.

Key Takeaways from Interpublic Group’s Q1 Results

We were impressed by how significantly Interpublic Group blew past analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good quarter with some key areas of upside. The stock traded up 2.3% to $24.49 immediately after reporting.

Interpublic Group put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.