Mueller Water Products trades at $26.67 and has moved in lockstep with the market. Its shares have returned 9.3% over the last six months while the S&P 500 has gained 7.7%.

Is now a good time to buy MWA? Find out in our full research report, it’s free.

Why Does Mueller Water Products Spark Debate?

As one of the oldest companies in the water infrastructure industry, Mueller (NYSE: MWA) is a provider of water infrastructure products and flow control systems for various sectors.

Two Things to Like:

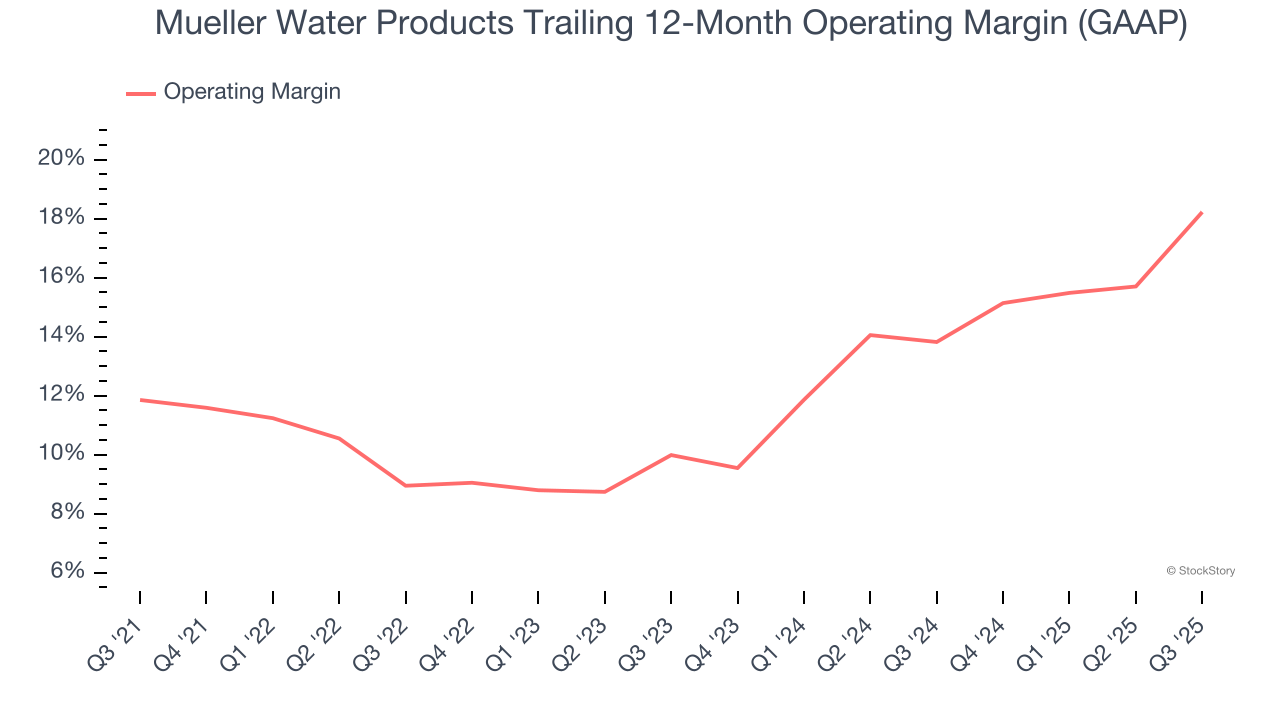

1. Operating Margin Rising, Profits Up

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Analyzing the trend in its profitability, Mueller Water Products’s operating margin rose by 6.4 percentage points over the last five years, as its sales growth gave it immense operating leverage. Its operating margin for the trailing 12 months was 18.2%.

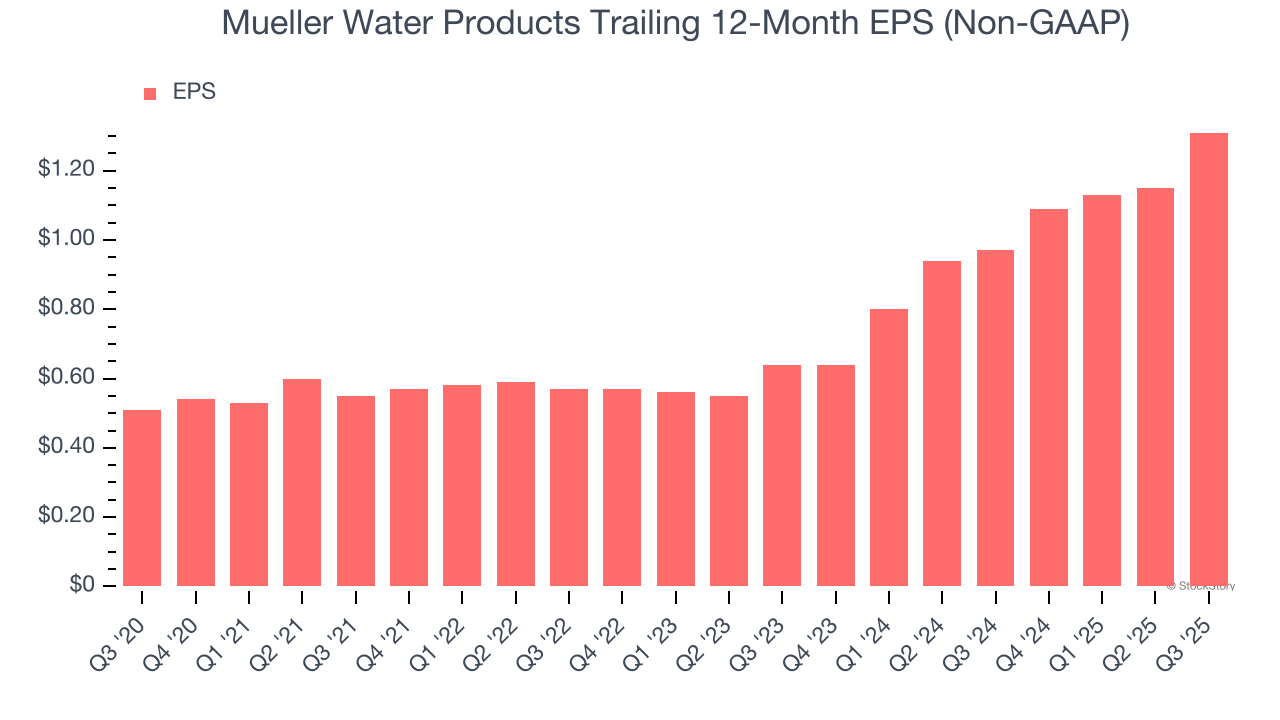

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Mueller Water Products’s EPS grew at an astounding 20.8% compounded annual growth rate over the last five years, higher than its 8.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

One Reason to be Careful:

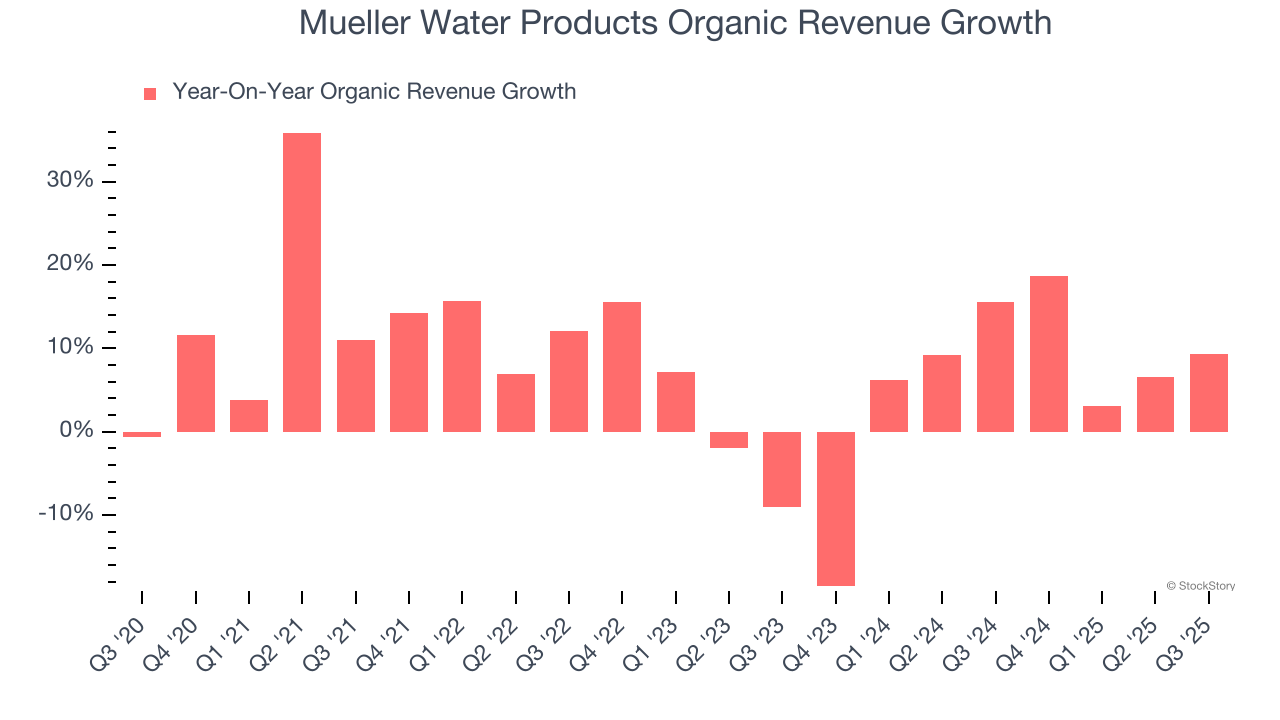

Slow Organic Growth Suggests Waning Demand In Core Business

Investors interested in Water Infrastructure companies should track organic revenue in addition to reported revenue. This metric gives visibility into Mueller Water Products’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Mueller Water Products’s organic revenue averaged 6.3% year-on-year growth. This performance slightly lagged the sector and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Final Judgment

Mueller Water Products’s merits more than compensate for its flaws, but at $26.67 per share (or 18.6× forward P/E), is now the right time to buy the stock? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Mueller Water Products

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.