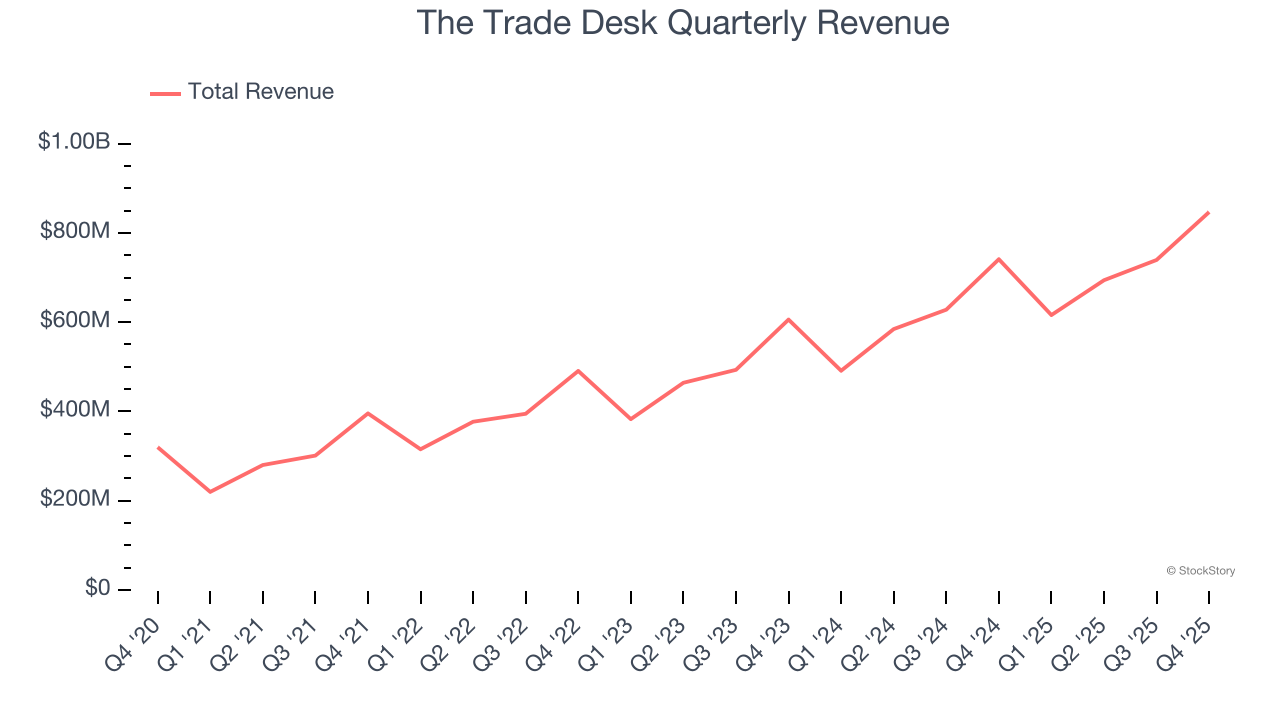

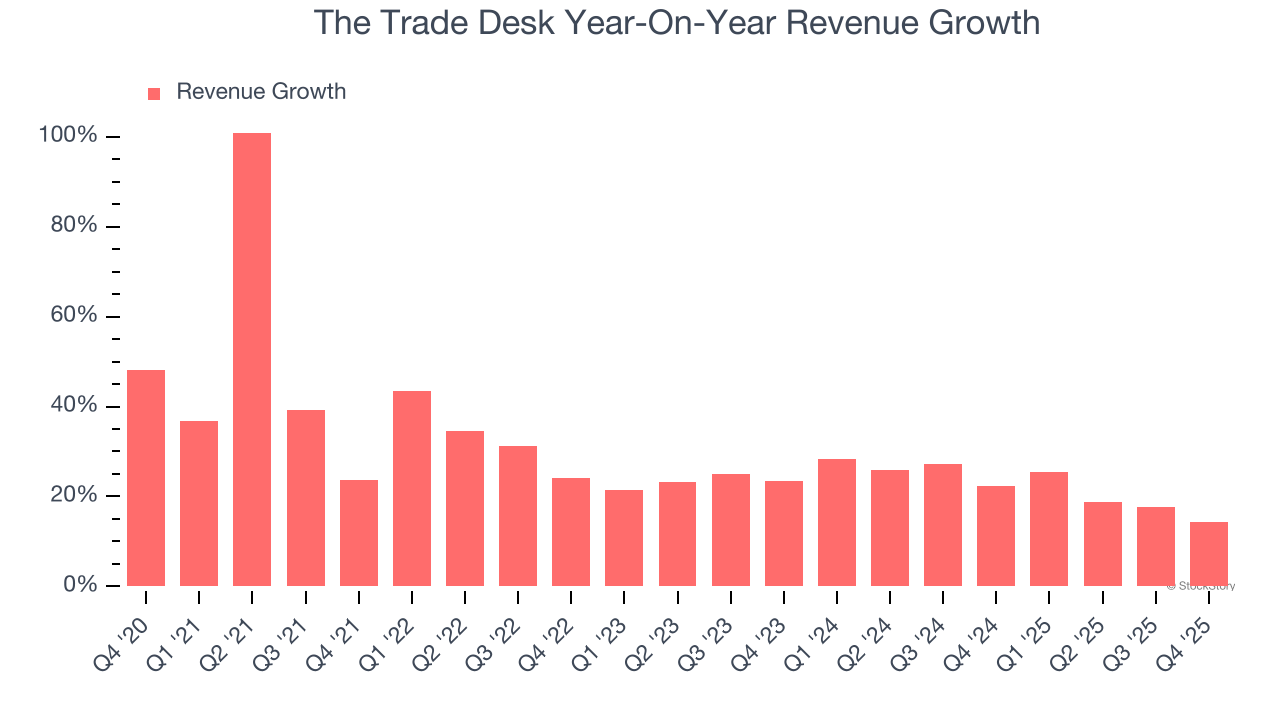

Digital advertising platform The Trade Desk (NASDAQ: TTD) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 14.3% year on year to $846.8 million. On the other hand, next quarter’s revenue guidance of $678 million was less impressive, coming in 1.5% below analysts’ estimates. Its non-GAAP profit of $0.59 per share was in line with analysts’ consensus estimates.

Is now the time to buy The Trade Desk? Find out by accessing our full research report, it’s free.

The Trade Desk (TTD) Q4 CY2025 Highlights:

- Revenue: $846.8 million vs analyst estimates of $841.9 million (14.3% year-on-year growth, 0.6% beat)

- Adjusted EPS: $0.59 vs analyst estimates of $0.58 (in line)

- Adjusted EBITDA: $400.3 million vs analyst estimates of $376.4 million (47.3% margin, 6.4% beat)

- Revenue Guidance for Q1 CY2026 is "at least" $678 million vs analyst estimates of $688.1 million

- EBITDA guidance for Q1 CY2026 is $195 million at the midpoint, below analyst estimates of $222.4 million

- Operating Margin: 30.3%, up from 26.4% in the same quarter last year

- Free Cash Flow Margin: 33.3%, up from 21% in the previous quarter

- Market Capitalization: $12.06 billion

“The Trade Desk delivered $2.9 billion in revenue in 2025 while continuing to generate significant profitability and cash flow,” said Jeff Green, Co-Founder and CEO of The Trade Desk.

Company Overview

Built as an alternative to "walled garden" advertising ecosystems, The Trade Desk (NASDAQ: TTD) provides a cloud-based platform that helps advertisers and agencies plan, manage, and optimize digital advertising campaigns across multiple channels and devices.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, The Trade Desk’s sales grew at an impressive 28.2% compounded annual growth rate over the last five years. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. The Trade Desk’s annualized revenue growth of 22% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, The Trade Desk reported year-on-year revenue growth of 14.3%, and its $846.8 million of revenue exceeded Wall Street’s estimates by 0.6%. Company management is currently guiding for a 10.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 15.6% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is above average for the sector and suggests the market is baking in some success for its newer products and services.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

The Trade Desk is extremely efficient at acquiring new customers, and its CAC payback period checked in at 5.5 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give The Trade Desk more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

Key Takeaways from The Trade Desk’s Q4 Results

We enjoyed seeing The Trade Desk beat analysts’ EBITDA expectations this quarter. On the other hand, its revenue guidance for next quarter slightly missed and its EBITDA guidance for next quarter also fell short of Wall Street’s estimates. Overall, this was a softer quarter that is not convincing enough after a few uneven quarters from the company that have led to fears that competition is hurting The Trade Desk or that its AI capabilities are falling behind. The stock traded down 15.6% to $21.41 immediately after reporting.

The Trade Desk’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).