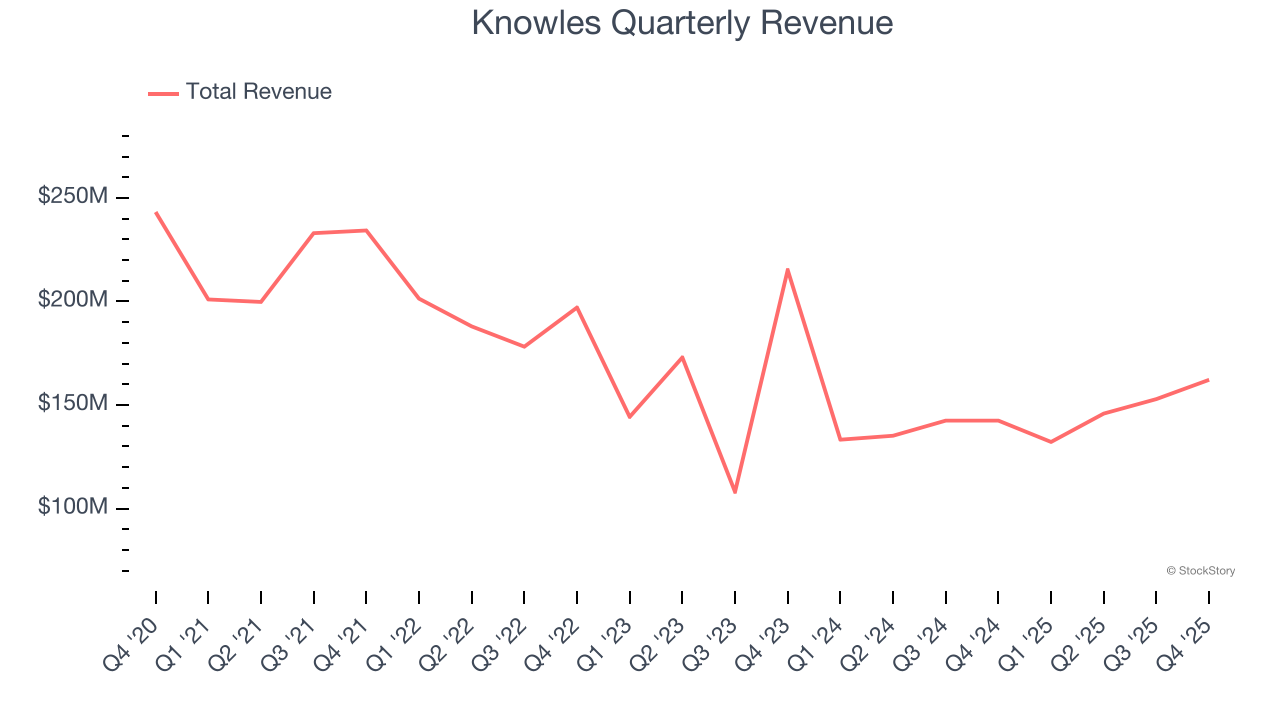

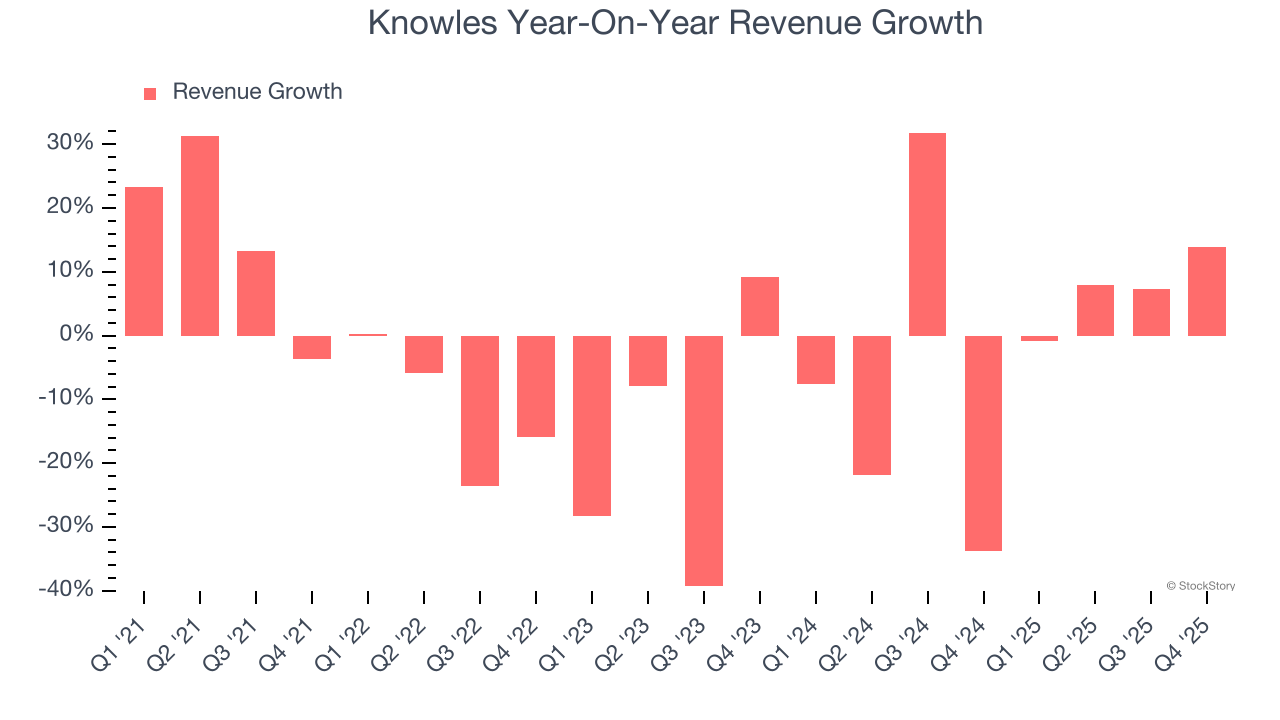

Electronic components manufacturer Knowles (NYSE: KN) announced better-than-expected revenue in Q4 CY2025, with sales up 13.8% year on year to $162.2 million. On top of that, next quarter’s revenue guidance ($148 million at the midpoint) was surprisingly good and 3.4% above what analysts were expecting. Its non-GAAP profit of $0.36 per share was in line with analysts’ consensus estimates.

Is now the time to buy Knowles? Find out by accessing our full research report, it’s free.

Knowles (KN) Q4 CY2025 Highlights:

- Revenue: $162.2 million vs analyst estimates of $156.2 million (13.8% year-on-year growth, 3.8% beat)

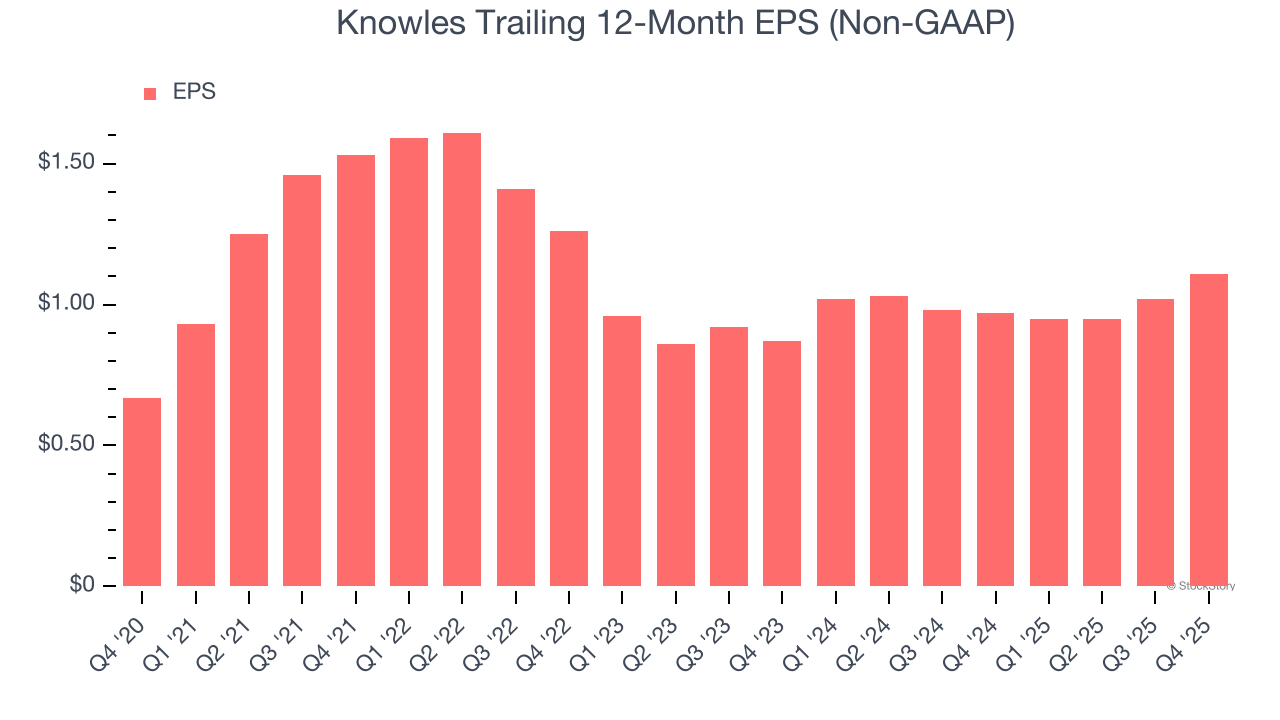

- Adjusted EPS: $0.36 vs analyst estimates of $0.35 (in line)

- Adjusted EBITDA: $41.3 million vs analyst estimates of $40.5 million (25.5% margin, 2% beat)

- Revenue Guidance for Q1 CY2026 is $148 million at the midpoint, above analyst estimates of $143.1 million

- Adjusted EPS guidance for Q1 CY2026 is $0.24 at the midpoint, above analyst estimates of $0.22

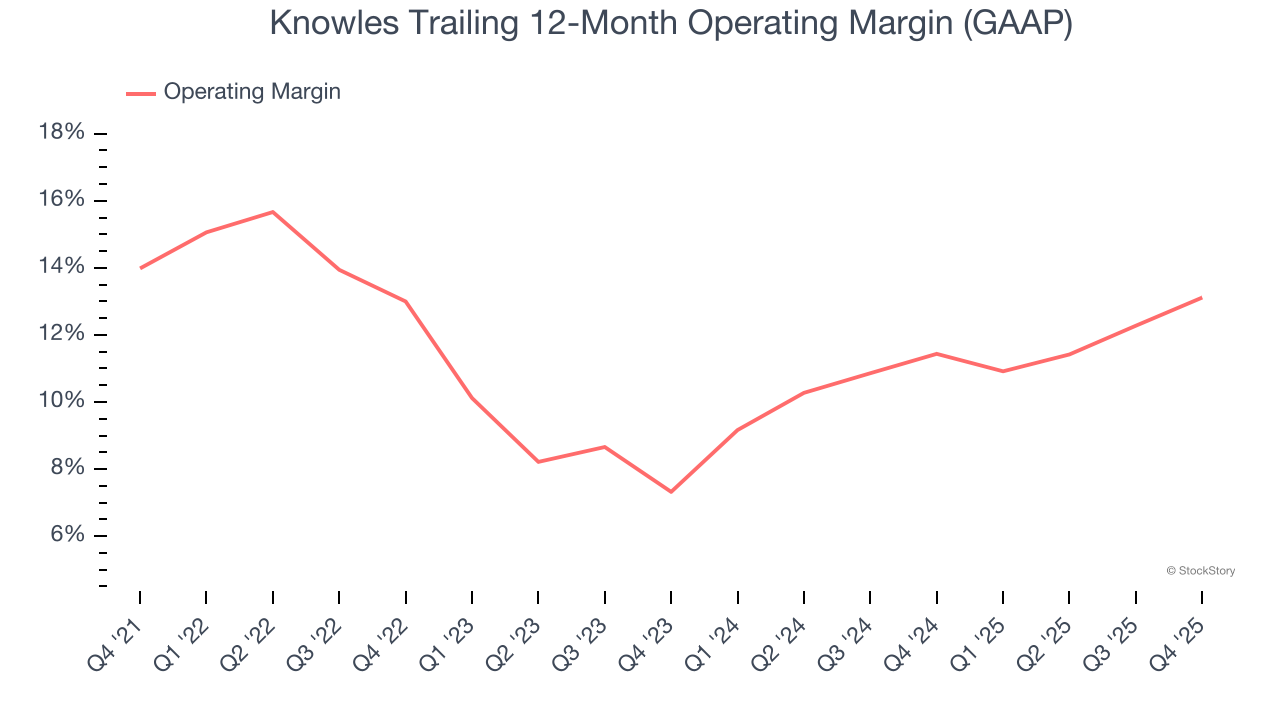

- Operating Margin: 15.9%, up from 12.9% in the same quarter last year

- Free Cash Flow Margin: 20.5%, similar to the same quarter last year

- Market Capitalization: $2.07 billion

“We finished 2025 with fourth quarter revenues and cash provided by operating activities exceeding the high end of our guided range, and non-GAAP diluted EPS from continuing operations above the mid-point of our guided range. We are executing on our strategy and delivered full year revenue growth of 7%, exceeding the high end of our five-year organic growth target. Our full year cash provided by operating activities was robust as we generated $114 million or 19.2% of revenues allowing us to further reduce our debt and continue to buy back shares,” commented Jeffrey Niew, President, and CEO of Knowles.

Company Overview

With roots dating back to 1946 and a focus on components that must perform flawlessly in critical situations, Knowles (NYSE: KN) designs and manufactures specialized electronic components like high-performance capacitors, microphones, and speakers for medical technology, defense, and industrial applications.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $593.2 million in revenue over the past 12 months, Knowles is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels.

As you can see below, Knowles’s revenue declined by 4.9% per year over the last five years, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Knowles’s annualized revenue declines of 3.8% over the last two years suggest its demand continued shrinking.

This quarter, Knowles reported year-on-year revenue growth of 13.8%, and its $162.2 million of revenue exceeded Wall Street’s estimates by 3.8%. Company management is currently guiding for a 12% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.8% over the next 12 months. While this projection implies its newer products and services will spur better top-line performance, it is still below the sector average.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Knowles’s operating margin has risen over the last 12 months and averaged 12% over the last five years. Its profitability was higher than the broader business services sector, showing it did a decent job managing its expenses.

Analyzing the trend in its profitability, Knowles’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. Shareholders will want to see Knowles grow its margin in the future.

This quarter, Knowles generated an operating margin profit margin of 15.9%, up 3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Knowles’s EPS grew at a remarkable 10.6% compounded annual growth rate over the last five years, higher than its 4.9% annualized revenue declines. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Knowles, its two-year annual EPS growth of 13% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Knowles reported adjusted EPS of $0.36, up from $0.27 in the same quarter last year. This print beat analysts’ estimates by 2.1%. Over the next 12 months, Wall Street expects Knowles’s full-year EPS of $1.11 to grow 9.9%.

Key Takeaways from Knowles’s Q4 Results

We were impressed by how significantly Knowles blew past analysts’ EPS guidance for next quarter expectations this quarter. We were also glad its revenue guidance for next quarter trumped Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $24.99 immediately after reporting.

Sure, Knowles had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).