It’s been a rough year thus far for the precious metals sector, and while gold (GLD) has only given up one-third of last year’s gains, down 7% vs. a 24% gain in 2020, the miners have been slaughtered, to say the least. This is evidenced by the near 40% decline we’ve seen in the Gold Miners Index (GDX), and the fact that some producers have slid as much as 50%. Not surprisingly, this has decimated sentiment in the sector, with many throwing in the towel completely and others booking tax losses on their gold miners and moving money to greener pastures.

However, the trick to investing in miners is to wait for the majority to give up on the trade before putting any real money to work and to only buy the best names when they’re trading at a discount to their net asset value. After the violent correction we’ve seen, these two requirements have now been satisfied, giving the green light for investors looking for a cheap sector to begin entering new positions. In this update, we’ll look at a few of the highest-quality names in the sector:

(Source: TC2000.com)

Many investors prefer to invest in the GDX or GLD to gain exposure to the gold sector, and this used to make complete sense in a market where many producers were poorly managed and few were paying you to hold their shares. However, since Q4 2020, we have seen the average dividend yield for million-ounce gold producers soar to more than 2.0%, with this figure now nearing 3.0% as we begin Q4 2021. This is more than double the dividend yield of the S&P-500 and is a very attractive dividend yield relative to nearly every other sector out there.

Plus, it is very easy to see which companies are managed the best operationally, given that it’s very difficult to hide weaknesses during cyclical and secular bear markets, and there are three companies that have emerged much stronger from the rubble, growing their market caps materially over the past decade and two years. These companies are B2Gold (BTG), Agnico Eagle Mines (AEM), and Alamos Gold (AGI), and they are all what I would consider to be best in breed gold producers. Given each company’s high-quality management and industry-leading margins, these companies have typically traded at large premiums to net asset value, and it’s been difficult to buy them at high single-digit free cash flow yields. However, with even the industry stalwarts being thrown out with the bathwater, all three are now on sale and sitting at very attractive valuations. Let’s take a closer look below:

Beginning with Alamos Gold, the stock is a mid-cap gold producer with two mines in Canada and one mine in Mexico, and the company produced more than 240,000 ounces of gold in the first half of the year, tracking at 49% of its guidance mid-point. Some investors have avoided the company given that its costs are in line with the industry average at $1,050/oz and given that it has been in a very high-capex period. This is because the company was busy for more than two years completing the Lower Mine Expansion at its Young-Davidson Mine in Canada.

However, with the Lower Mine Expansion complete, the Young Davidson Mine is now a cash-flow machine. This has helped push revenue up considerably on a year-over-year basis ($422MM vs. $303MM), and the company’s Island Gold Mine continues to report incredible results, with its highest-grade intercept drilled to date reported last month. This intercept was 21.33 meters of 72.21 grams per tonne gold, which is well above the average reserve grade (12 grams per tonne gold) at Island, suggesting further reserve growth and the potential for a new mine more robust mine plan going forward.

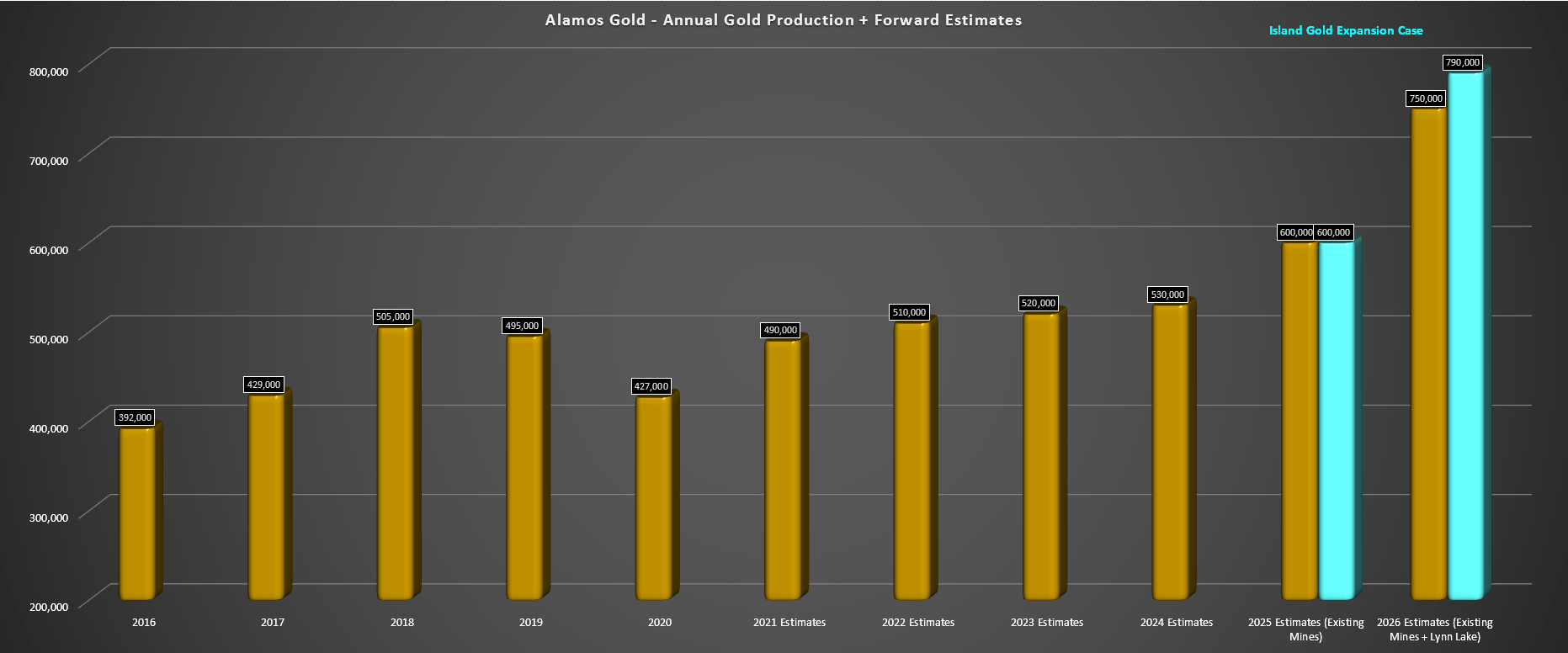

(Source: Company Filings, Author’s Chart & Estimates)

As the chart above shows, Island Gold is just a year away from beginning work on a Phase III Expansion with the plan to sink a shaft at the project to increase mine production to more than 2,000 tonnes per day. This is expected to boost annual production from ~150,000 ounces per year to ~240,000 ounces per year and push costs down from $750/oz to barely $525/oz by 2025. However, if the reserve base continues to grow, I would not be surprised if Alamos increased its mill capacity further, allowing it to process more material than currently projected in the Phase III Study. This could potentially increase production to closer to 300,000 ounces per annum by 2026, helping Alamos to grow production by more than 55% over the next five years at 20% lower costs.

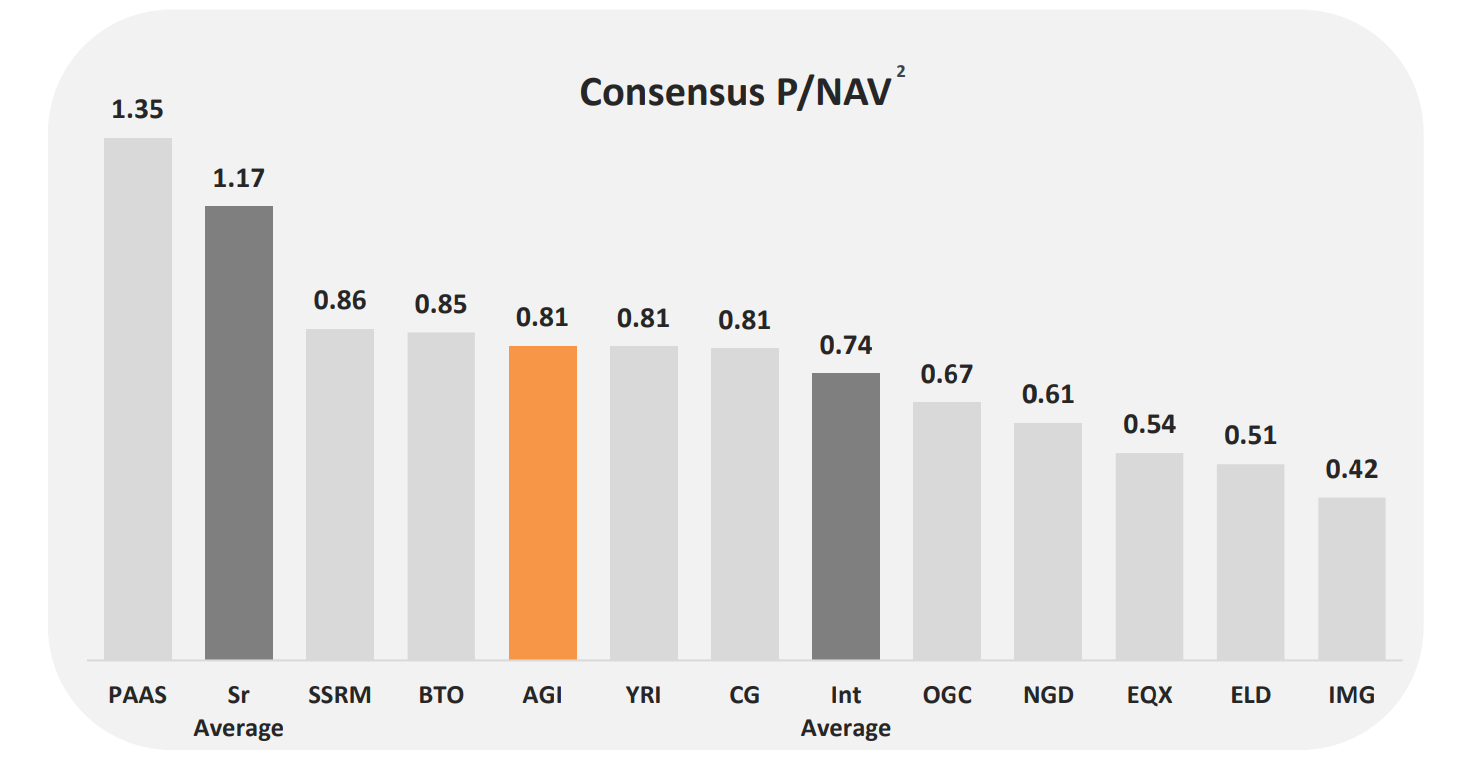

This would be a major catalyst for a re-rating, but despite this, the stock trades at a dirt-cheap valuation of just 0.70x consensus P/NAV (recent chart is dated). This makes Alamos a steal at the current share price of $7.50, and I see a fair value for the stock at least 50% higher at $11.25 per share. So, I plan to continue to add on weakness and recently increased my position below $7.70.

(Source: Alamos Gold Company Presentation)

The next company worth paying close attention to is Agnico Eagle Mines, and we’ve seen major news recently, with the company planning to merge with Kirkland Lake Gold to create the 3rd largest gold producer globally. The two companies would complement each other with a mid-single-digit compound annual production growth rate over the next three years, a shift from 3 mines for KL to 13 mines total, and significant operational synergies in the Kirkland Lake mining camp in Ontario, Canada.

Notably, AEM would be able to leverage KL’s mill in the area, which is currently sitting idle, with the goal of putting another mine into operation within the next four years. This would come at a significantly reduced cost and help to unlock value for these two assets, which are not being appropriately valued, given that AEM currently has orphaned resources with no way to process them. KL has a mill with no high-grade material to process, meaning that the combination of these two assets can create a mine with limited permitting work and the potential for up to $400MM in annual revenue from this mine alone by FY2024.

In summary, the deal looks very beneficial to both companies, with AEM set to the lowest-cost million-ounce producer, the lowest-risk producer given that more than 95% of production will come from Tier-1 jurisdictions, and also one of the highest-growth producers, with multiple mines set to be put into production between now and 2028. In fact, if the combined entity can deliver on its plans, production should grow from 3.3MM ounces in 2022 to more than 4.3MM ounces in 2028. This would command a premium multiple for the company and make it the most attractive gold producer in the sector for both funds and generalist investors.

(Source: TC2000.com)

Despite this exciting combination, AEM currently sits at its most oversold level in several years. Previous dips to these oversold conditions have led to 40% forward returns over the following 12 months on average. While history doesn’t have to repeat itself, this suggests that the stock looks very attractive after the recent pullback, especially with a conservative fair value close to $73.00 per share. Besides, AEM also pays a very attractive dividend yield of 2.7% and has noted that it is open to special dividends in the future combined with its industry-leading track record of dividend growth.

So, at a current share price of $54.00, I see the stock as a steal and by far the most attractive way to get exposure to the gold sector for long-term investors. Currently, I remain long AEM from $51.00 per share, and I would strongly consider adding to my position on further weakness.

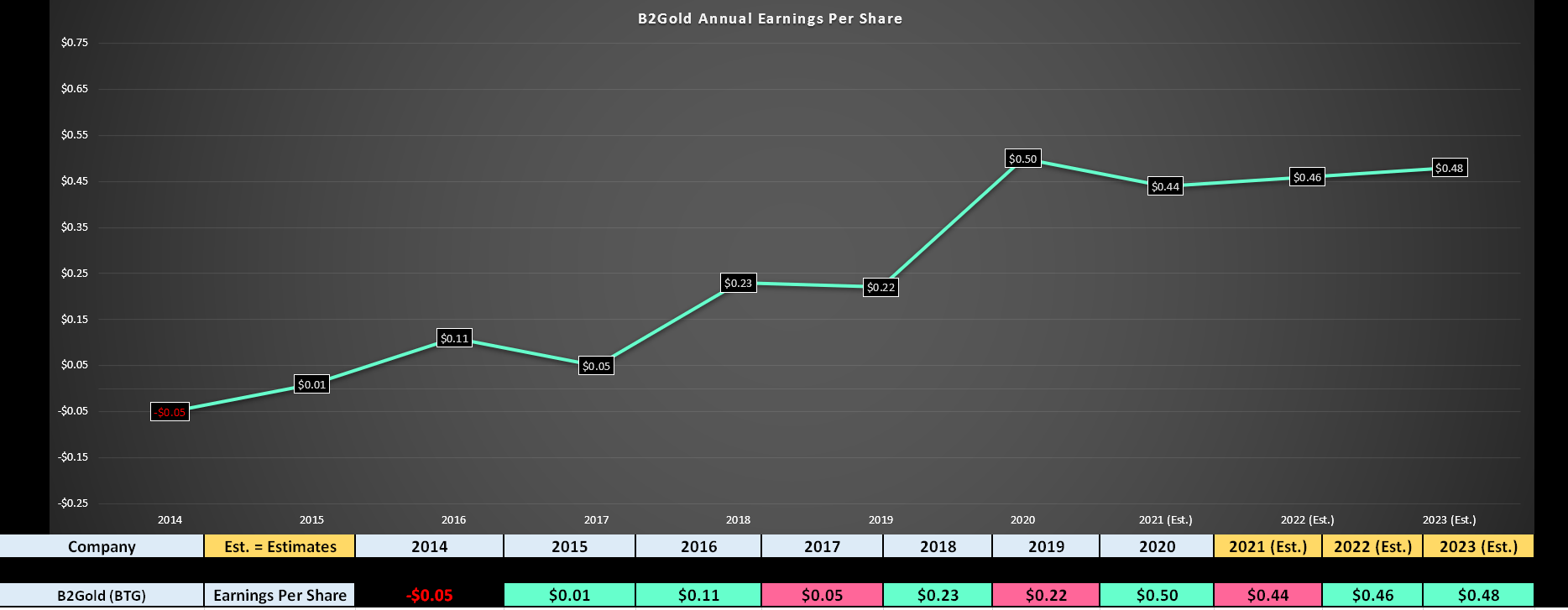

The final name on the list is B2Gold, a mid-cap gold producer that just came off a tough H1 performance given that it was up against very difficult comps on a year-over-year basis. This led to a decline in H1 earnings per share and revenue, with H1 2021 revenue of $725MM, down over 10% from H1 2020 revenue of $821MM.

However, it’s important to note that BTG was up against record results in the prior year, so some softness was to be expected. Importantly, though, the stock is now sitting at barely 7.8x FY2022 earnings estimates of $0.46 and paying a dividend yield of nearly 4.5% at a share price of $4.60. This is a more than reasonable valuation for BTG, with this sell-off looking overdone due to the difficult year-over-year comps. In summary, I see this pullback as a low-risk buying opportunity, and I may look to start a position in the stock if we see a re-test of the $4.45 level where the stock has proven that it has strong support.

(Source: YCharts.com, Author’s Chart)

After a year of horrid returns it’s easy to be negative on the gold sector, but I think this is the time to be optimistic, given that so many investors have thrown in the towel. As the saying goes, the best time to buy is when blood is in the streets, and the last time we saw this much carnage in the sector, the gold price was below $1,300/oz, the average dividend yield was below 1.0%, and these companies had operating margins below 20%. Currently, operating margins sit north of 35% on average, the average million-ounce producer is paying nearly 3.0% per annum, and the gold price is above $1,700/oz.

This suggests that the recent weakness is irrationality and forced selling, providing a very low-risk entry into the sector to diversify one’s portfolio. Given the recent selling pressure, I have built positions in 2 of the 3 higher-quality names (AEM, KL, AGI), and I may look to start a position in BTG on further weakness.

Disclosure: I am long GLD, AGI, AEM, KL

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

KL shares were trading at $43.36 per share on Friday afternoon, up $0.25 (+0.58%). Year-to-date, KL has gained 6.03%, versus a 18.25% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 3 Gold Miners to Buy on the Dip appeared first on StockNews.com