Bumble’s stock price has taken a beating over the past six months, shedding 33.2% of its value and falling to $5.93 per share. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Bumble, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Bumble Not Exciting?

Despite the more favorable entry price, we're swiping left on Bumble for now. Here are three reasons why there are better opportunities than BMBL and a stock we'd rather own.

1. Customer Spending Decreases, Engagement Falling?

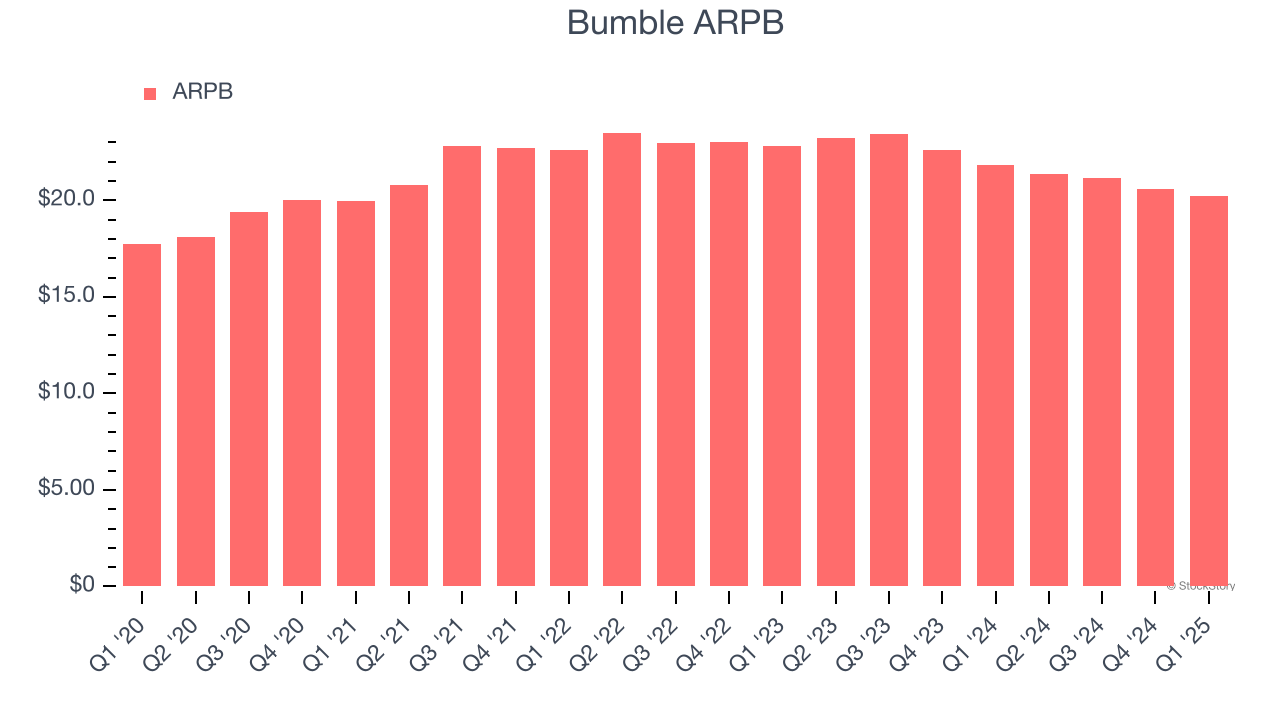

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much the average buyer spends. ARPB is also a key indicator of how valuable its buyers are (and can be over time).

Bumble’s ARPB fell over the last two years, averaging 4.9% annual declines. This isn’t great, but the increase in paying users is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Bumble tries boosting ARPB by taking a more aggressive approach to monetization, it’s unclear whether buyers can continue growing at the current pace.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Bumble’s revenue to drop by 11.1%, a decrease from its 9.4% annualized growth for the past three years. This projection is underwhelming and implies its products and services will see some demand headwinds.

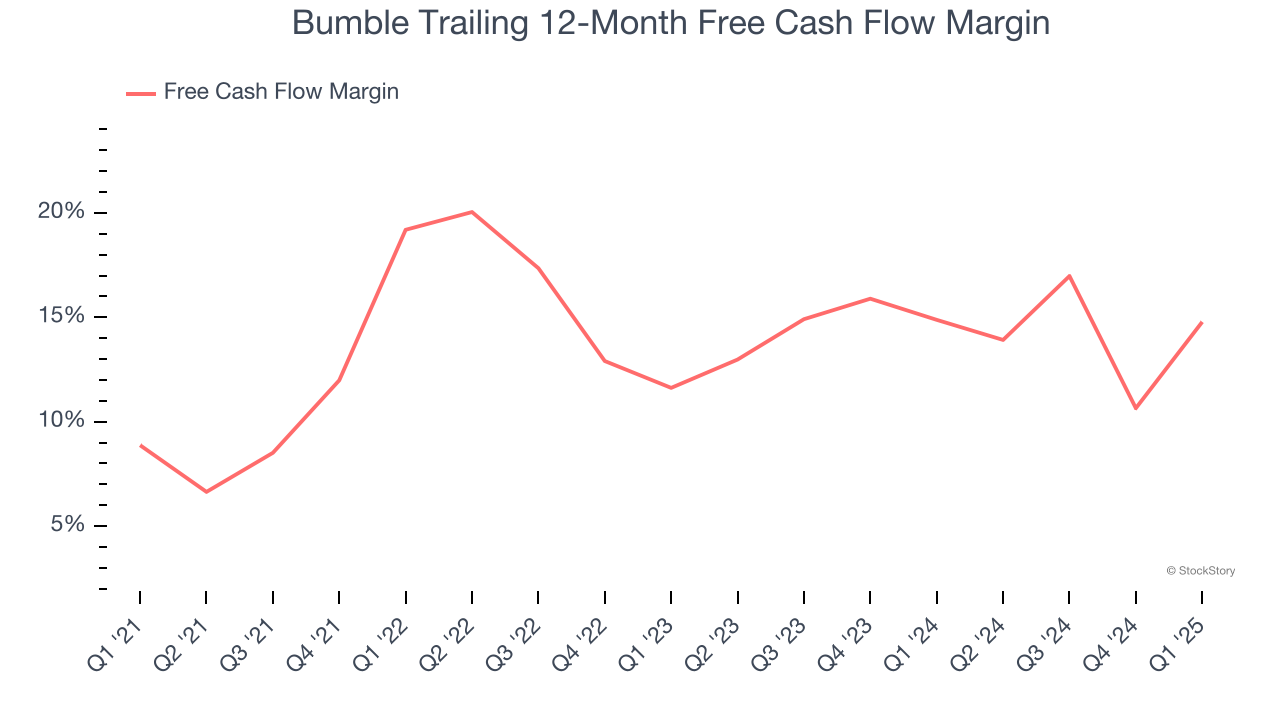

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Bumble’s margin dropped by 4.4 percentage points over the last few years. If its declines continue, it could signal increasing investment needs and capital intensity. Bumble’s free cash flow margin for the trailing 12 months was 14.8%.

Final Judgment

Bumble isn’t a terrible business, but it isn’t one of our picks. After the recent drawdown, the stock trades at 2.6× forward EV/EBITDA (or $5.93 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

Stocks We Would Buy Instead of Bumble

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.