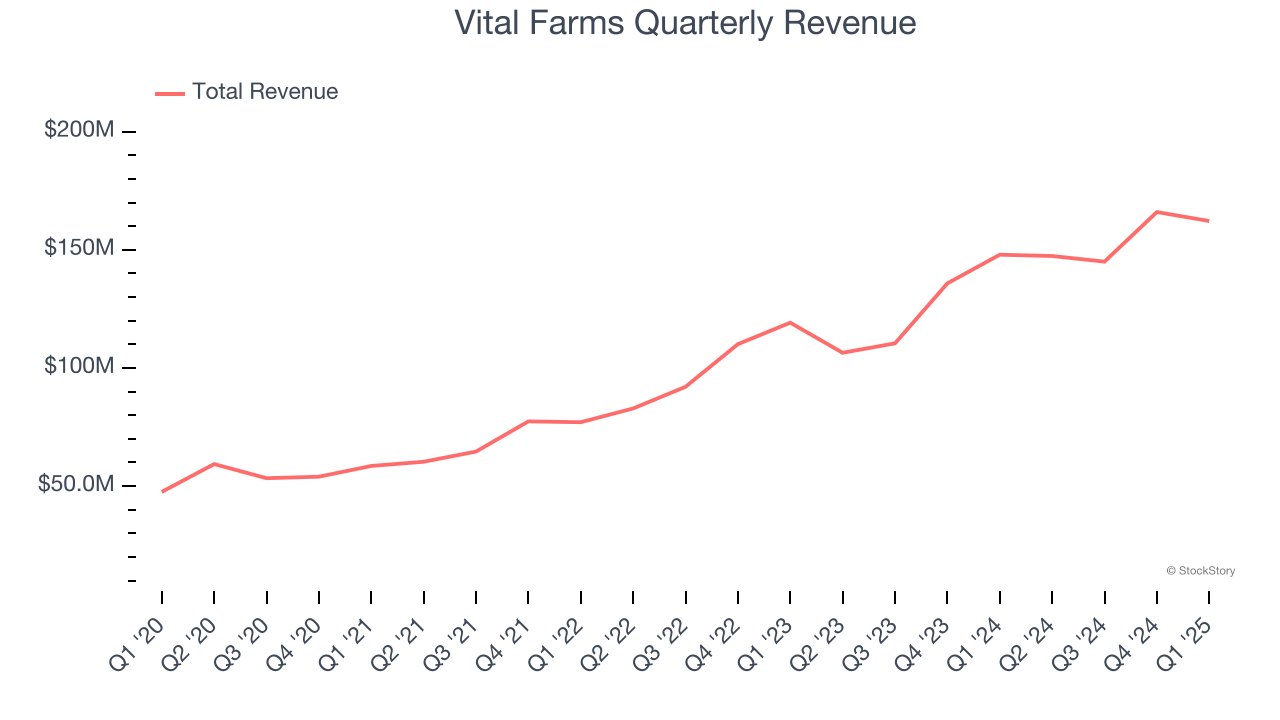

Egg and butter company Vital Farms (NASDAQ: VITL) met Wall Street’s revenue expectations in Q1 CY2025, with sales up 9.6% year on year to $162.2 million. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $740 million at the midpoint. Its GAAP profit of $0.37 per share was 45.1% above analysts’ consensus estimates.

Is now the time to buy Vital Farms? Find out by accessing our full research report, it’s free.

Vital Farms (VITL) Q1 CY2025 Highlights:

- Revenue: $162.2 million vs analyst estimates of $162.6 million (9.6% year-on-year growth, in line)

- EPS (GAAP): $0.37 vs analyst estimates of $0.26 (45.1% beat)

- Adjusted EBITDA: $27.48 million vs analyst estimates of $21.33 million (16.9% margin, 28.8% beat)

- The company reconfirmed its revenue guidance for the full year of $740 million at the midpoint

- EBITDA guidance for the full year is $100 million at the midpoint, below analyst estimates of $100.9 million

- Operating Margin: 13.4%, down from 16.3% in the same quarter last year

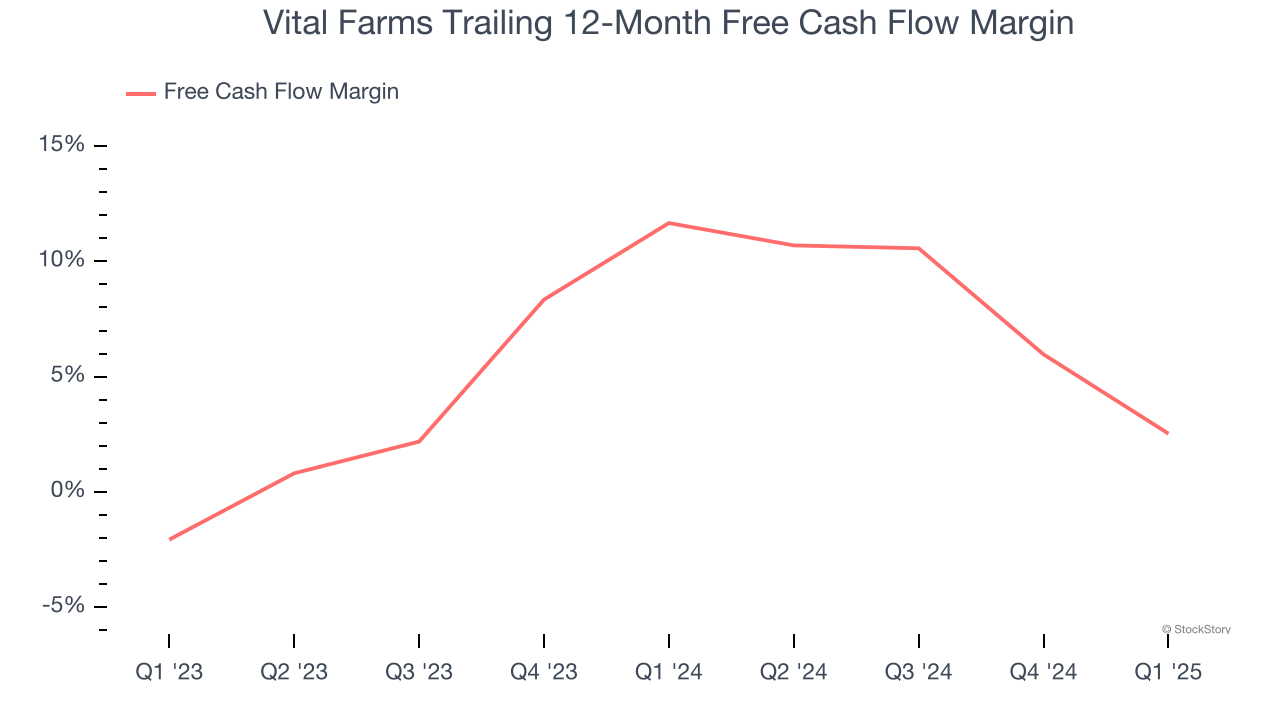

- Free Cash Flow Margin: 1.3%, down from 15.3% in the same quarter last year

- Market Capitalization: $1.6 billion

“We delivered first quarter results that were in-line with our overall expectations and made good progress on our key 2025 strategic initiatives", said Russell Diez-Canseco, Vital Farms’ President and Chief Executive Officer. “We demonstrated solid execution, ongoing business momentum, and our continued focus on bringing ethical food to the table."

Company Overview

With an emphasis on ethically produced products, Vital Farms (NASDAQ: VITL) specializes in pasture-raised eggs and butter.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $620.6 million in revenue over the past 12 months, Vital Farms is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, Vital Farms grew its sales at an incredible 30.5% compounded annual growth rate over the last three years as consumers bought more of its products.

This quarter, Vital Farms grew its revenue by 9.6% year on year, and its $162.2 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 25% over the next 12 months, a deceleration versus the last three years. Still, this projection is noteworthy and indicates the market sees success for its products.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Vital Farms has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.6% over the last two years, slightly better than the broader consumer staples sector.

Taking a step back, we can see that Vital Farms’s margin dropped by 9.1 percentage points over the last year. If its declines continue, it could signal increasing investment needs and capital intensity.

Vital Farms’s free cash flow clocked in at $2.15 million in Q1, equivalent to a 1.3% margin. The company’s cash profitability regressed as it was 14 percentage points lower than in the same quarter last year, which isn’t ideal considering its longer-term trend.

Key Takeaways from Vital Farms’s Q1 Results

We were impressed by how significantly Vital Farms blew past analysts’ EPS and EBITDA expectations this quarter. On the other hand, its full-year EBITDA guidance slightly missed. Overall, we think this was still a solid quarter. The stock remained flat at $36.01 immediately following the results.

Sure, Vital Farms had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.