Shares of Palantir Technologies (PLTR) have been moving up and down in 2026 as investors react to the Iran war and changing market sentiment. Just a few weeks ago, Palantir was one of the hottest names in the market driven by defense demand. But PLTR stock soon started losing steam as concerns of valuations resurfaced. Palantir is closely linked to modern warfare. Its AI software systems are now deployed in defense operations, and the company's Chief Technology Officer recently stated that the conflict in Iran will be recognized as the first significant AI-driven war.

Palantir stock is down 17% year-to-date (YTD), and trades roughly 29% below its 52-week high of $207.52. However, PLTR is up slightly for the day at the time of this writing.

This wild ride has investors divided on whether to buy or avoid the stock. Let’s take a closer look.

Rising Global Tensions Put Palantir in Focus

Valued at $350.3 billion by market capitalization, Palantir builds software platforms like Gotham for government agencies and Foundry for businesses, along with its newer Artificial Intelligence Platform (AIP). These tools help turn large amounts of data into clear, real-time insights. With the Iran war escalating, the bull argument is that Palantir will play a key role in future military strategy. The company continues to win large government contracts and is becoming a core part of U.S. defense systems. Its Maven AI platform, including drone and battlefield operations, is now a long-term Pentagon program, which could bring steady revenue for years.

In 2025, U.S. government revenue jumped 55% year-over-year (YOY) to reach $1.85 billion. New and expanding defense deals, particularly with GE Aerospace (GE) and the U.S. Air Force, are strengthening Palantir’s case with the government. The company also secured a contract worth up to $448 million with the U.S. Navy to enhance shipbuilding operations and streamline production.

What’s more impressive is that governments outside the U.S. are also trusting Palantir’s platform, with international government revenue up 47% YOY to $547 million in 2025. The commercial AI business adds a second growth engine. Notably, U.S. commercial revenue climbed 109% for the full year to $1.46 billion. Overall, total revenue climbed 56% to $4.47 billion in 2025, and management expects a 61% increase in revenue to $7.19 billion in 2026.

The Biggest Concern

The bear case is that the company's valuation remains stretched compared to other software companies. At 143 times forward earnings, Palantir stock remains expensive. In 2026, the market has already been concerned with the high valuations of AI stocks and a lack of earnings growth to justify them. However, this is not the case with Palantir. Analysts expect the company’s earnings to increase by 76% in 2026, followed by 41% growth in 2027.

There are also growing concerns around the company’s ethics, government dependency, and political backlash tied to its defense work, which had kept Wall Street bearish for the last two years. The company has addressed some of these concerns. Palantir is no longer solely a government-focused company. Its commercial business is rapidly expanding, with more firms now adopting its AI platform to move from testing AI ideas to actually using them in daily operations.

I believe the combination of steady government contracts and fast-growing commercial AI demand gives Palantir a more balanced business model now. If both sides continue to grow, Palantir could remain a major player in the AI space for years to come, justifying its premium. For investors supporting the bull case, the recent dip is a huge opportunity.

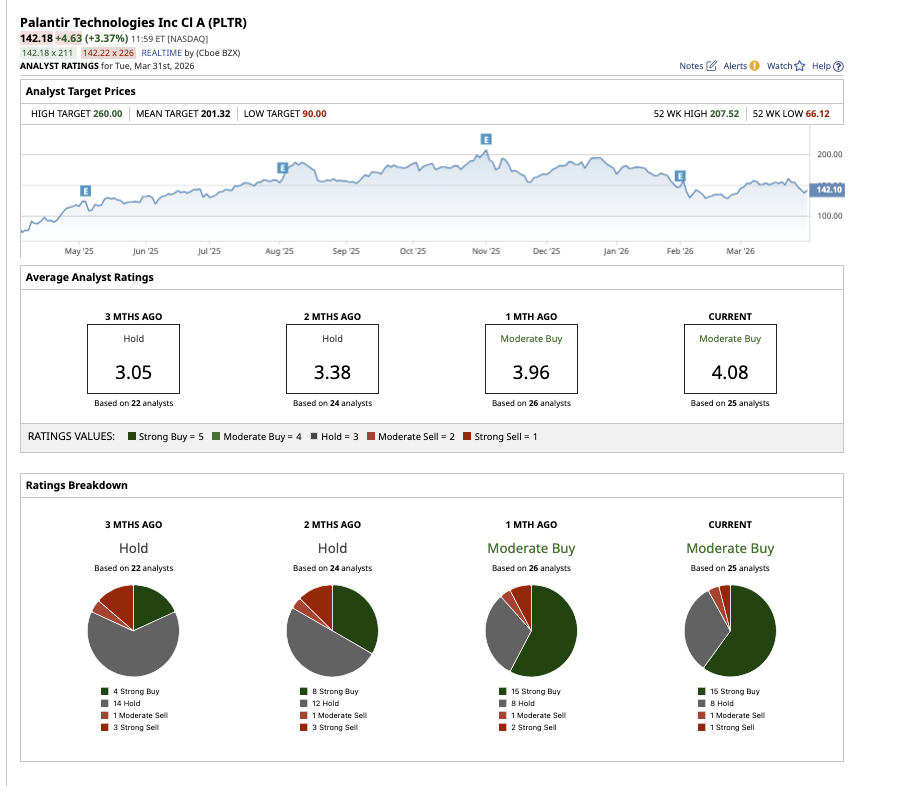

Wall Street Is Split on PLTR Stock

Wall Street now gives Palantir an overall "Moderate Buy" rating. Of the 25 analysts covering PLTR stock, 15 rate it as a “Strong Buy,” eight have a “Hold” rating, one analyst has a “Moderate Sell,” and one analyst has a “Strong Sell" rating. Based on the average price target of $201.32, analysts see PLTR stock climbing as much as 37% from current levels. The high price estimate of $260 suggests potential upside of 77% from here.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart