The old proverb “make hay while the sun shines” can be aptly applied to Japanese memory chipmaker Kioxia (KXIAY). The demand for memory chips has never been higher and is only poised to climb further, thanks to the massive AI infrastructure buildout. With this, shares of companies like Micron (MU), SanDisk (SNDK), and the Korean duo Samsung and SK Hynix have rewarded shareholders with huge returns.

So has Kioxia, as shares have more than quadrupled so far this year. But that's in the Japanese market — what about in the United States?

Kioxia Is Looking to List in the U.S.

Unfortunately, Kioxia is still not listed on a major exchange in the United States. Investors can gain exposure to the company only through the over-the-counter (OTC) markets, which is not desirable for a large section of investors, whether institutional or individual.

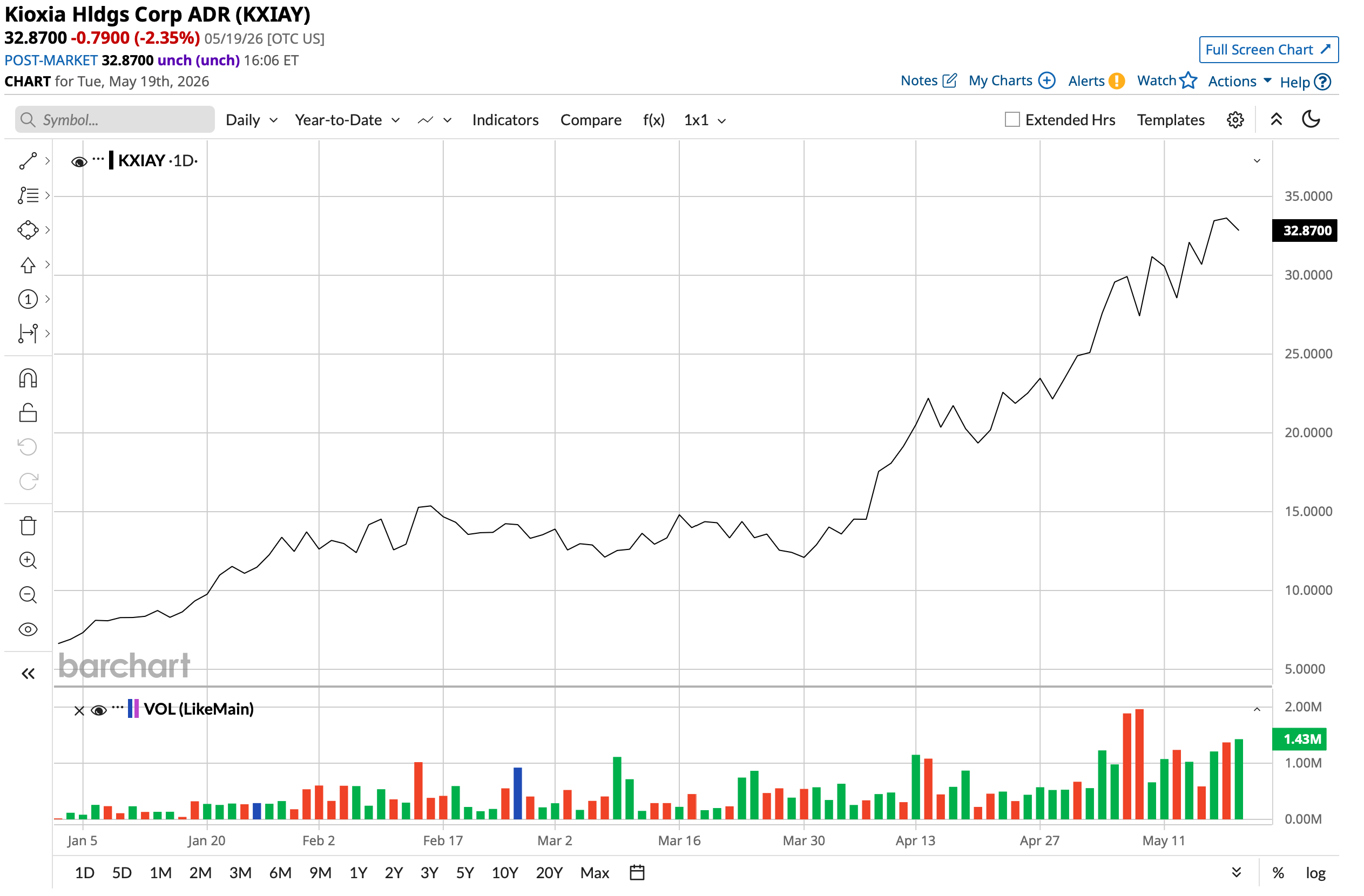

Still, to get a picture of the measure of its outperformance, the KXIAY ADR is up a senstational 460% year-to-date (YTD). For context, Micron shares are up 167% in the same period.

“The Company is preparing to list American depositary shares […] representing its common shares on a U.S. stock exchange to grow its investor base and increase its corporate value,” Kioxia said in a recent notice. "This listing is contingent upon the approval of the relevant authorities. Details of the listing such as the schedule, listing market, and listing method have not yet been decided, and the Company may decide not to continue pursuing the listing depending on the circumstances over the course of the preparation."

About Kioxia Stock

Founded in 2019 with origins tracing to the legendary Toshiba group, Kioxia is one of the world’s major NAND flash memory manufacturers and a critical supplier to the global digital storage ecosystem. It develops and manufactures NAND flash memory, SSDs, and enterprise storage solutions. From personal devices to hyperscalers, data centers, and enterprise servers, Kioxia's customer base is wide and continually expanding.

However, as the company gets set to list amid the hotbed of AI innovation, should investors look upon Kioxia stock favorably and add shares to their portfolios? Or should they adopt a wait-and-watch mode? An analysis is warranted to provide a clearer picture.

What Makes Kioxia Stand Out?

In a report, analyst Kazuyoshi Saito of Cosmo Securities made a simple case for Kioxia. "Kioxia's NAND has strengths including production costs that are 20%-30% lower than those of its competitors, higher storage capacity per unit area, and data read and write speeds that are 10%-20% faster than rival products," the analyst noted.

So, Kioxia is cheaper, faster, and offers more storage capacity. But this has certainly not been an overnight story.

The foundation of Kioxia's real competitive advantage is its BiCS FLASH 3D NAND architecture, a technology it invented in 2007 and has now developed through multiple generations. Kioxia invented NAND flash memory itself in 1987 as Toshiba, and has spent nearly 40 years accumulating institutional knowledge, manufacturing expertise, and intellectual property that no competitor can simply replicate through capital spending alone.

The company's long-term joint venture with SanDisk is another structural pillar that is genuinely difficult to replicate. Kioxia and SanDisk operate some of the world's largest NAND flash production sites in Yokkaichi and Kitakami, sharing the cost of expensive semiconductor equipment and R&D, achieving economies of scale that allow both firms to compete cost-effectively against South Korean memory giants without needing to fund investments independently.

Coming to the here and now, Kioxia's AI product roadmap looks promising. The firm is developing a Super High IOPS SSD targeting over 10 million input and output operations per second by combining XL-FLASH with a new SSD controller, with samples planned for the second half of 2026. It's also developing the CM9 series, a high-performance SSD for AI systems designed specifically to maximize GPU capabilities requiring both high performance and high reliability.

The most ambitious product in the pipeline, however, is the GPU-adjacent SSD. In partnership with Nvidia (NVDA), Kioxia is developing drives that could connect directly to GPUs and partially replace high-bandwidth memory, potentially boosting GPU memory capacity in generative AI servers.

On the silicon side, Kioxia is advancing its 10th-generation BiCS FLASH beyond 300 layers, with production set to begin in 2026, alongside a 9th-generation variant that fully leverages its CBA technology to deliver high performance at reduced investment costs.

Kioxia is also taking a meaningful step toward securing its own stable supply of DRAM, a vulnerability the company had long carried by sourcing all of its requirements from outside vendors. The arrangement involves Kioxia subscribing to a third-party allotment of new shares being issued by Nanya, alongside a long-term supply agreement that the two companies intend to formalize. Prior to this, any industry-wide shortage in DRAM supply would have left Kioxia exposed with limited options and no guaranteed access to necessary components. The capital injection and the accompanying procurement deal together give the company a multiyear window of supply visibility that substantially reduces risk going forward.

However, while the DRAM issue is being addressed, there remains a more structural technological risk. Kioxia has historically focused on triple-level cell processes with strengths in consumer SSDs rather than enterprise SSDs, and as competitors accelerate toward quad-level cell enterprise drives for AI data centers, there is a credible concern that Kioxia is behind the curve on the specific product category that hyperscalers are prioritizing most aggressively.

Notably, SK Hynix has developed its 9th-generation 321-layer QLC NAND and plans to supply enterprise SSDs to major data centers in 2026, while Kioxia has confirmed that it is not currently pursuing high-bandwidth flash development, a product category that SanDisk is developing in collaboration with SK Hynix. That divergence matters because it signals a risk that Kioxia could find itself underrepresented in the highest-growth, highest-margin enterprise segment just as it accelerates.

The Financials Reflect Demand

Kioxia's numbers are a fine indicator that demand remains solid. For the fiscal year ended March 31, 2026, revenue increased by 37% from the previous year to JPY 2,337.6 billion. EPS roughly doubled in the same period to JPY 1,009.15 per share. Not only that, returns and margins improved, too.

While return on equity and return on assets improved to 51.9% and 23.7% from 45.9% and 12.8%, respectively, operating margin rose to 37.2% from 26.5% in the year-ago period. Meanwhile, cash flow from operating activities increased to JPY 616.54 billion from JPY 476.41 billion in the prior year. Overall, the company exited the fiscal year with a cash balance of JPY 470.71 billion, higher than its short-term debt levels of JPY 203.37 billion.

Conclusion

Another memory chipmaker may raise feelings of the same getting commoditized. However, Kioxia is an established player in the segment with some differentiated offerings, operating in an industry which is witnessing unprecedented demand. What's more, the company is making serious efforts to cater to this ongoing AI-focused supercycle. While there are some technological issues, the company's sizeable cash balance and revenue growth leave it enough headroom to invest in innovation and alleviate those concerns.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart