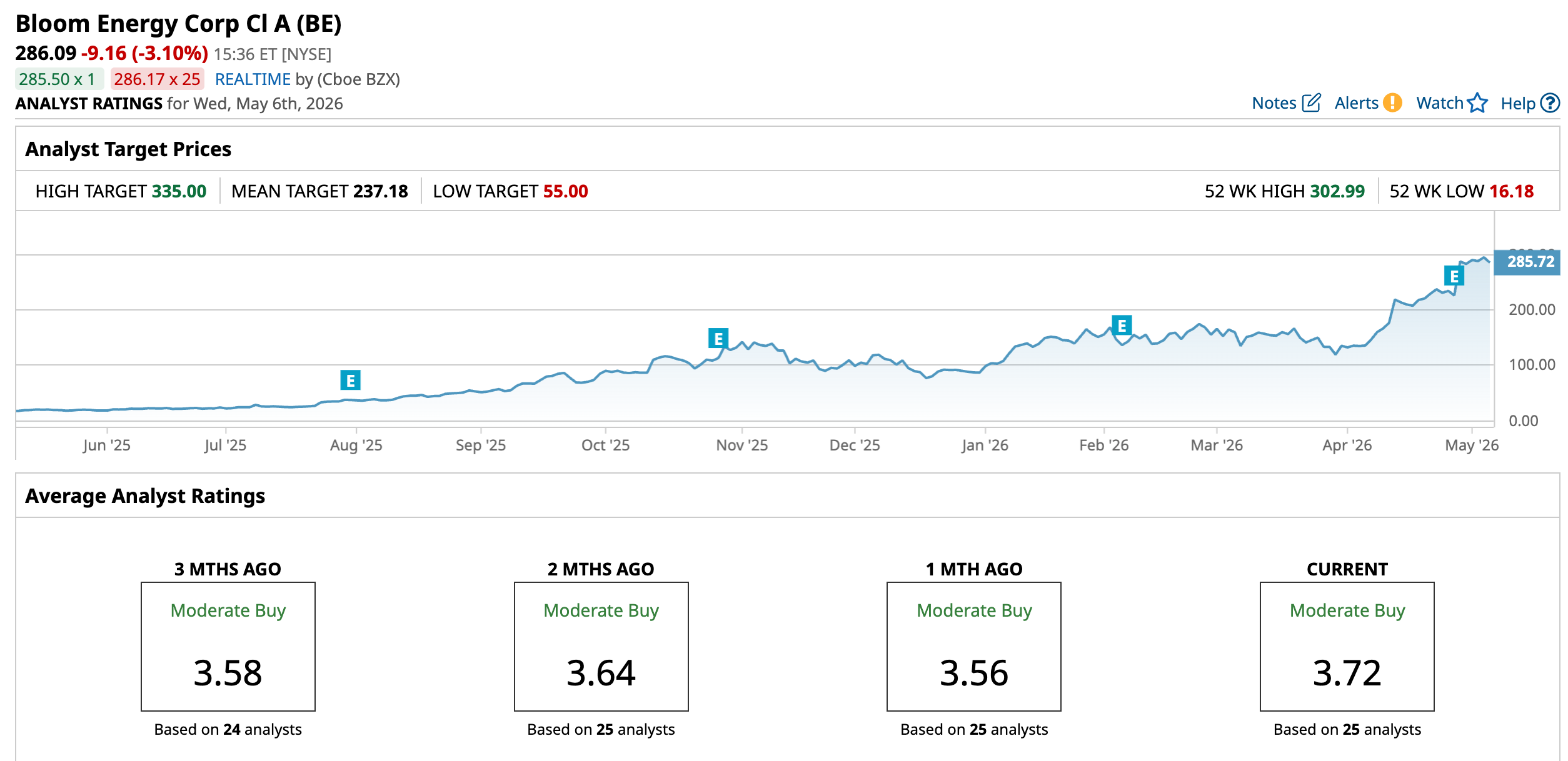

Analysts at financial services firm RBC Capital continues to believe that Bloom Energy (BE) will keep on blooming. The firm maintained a “Buy” rating on the stock with a price target of $335, which denotes an upside of 17.1% from current levels.

Initiating coverage on the company in July 2023 with an “Outperform” rating, with the rationale of decarbonization tailwinds and strong fuel cell demand. Now, the massive power demand required for the AI infrastructure buildout has been cited as the reason for the bullishness.

About Bloom Energy

Founded in 2001 and based in San Jose, California, Bloom Energy designs and sells solid oxide fuel cell (SOFC) systems. Bloom Energy serves end markets such as data centers, utilities, hospitals, telecom, and infrastructure, among others.

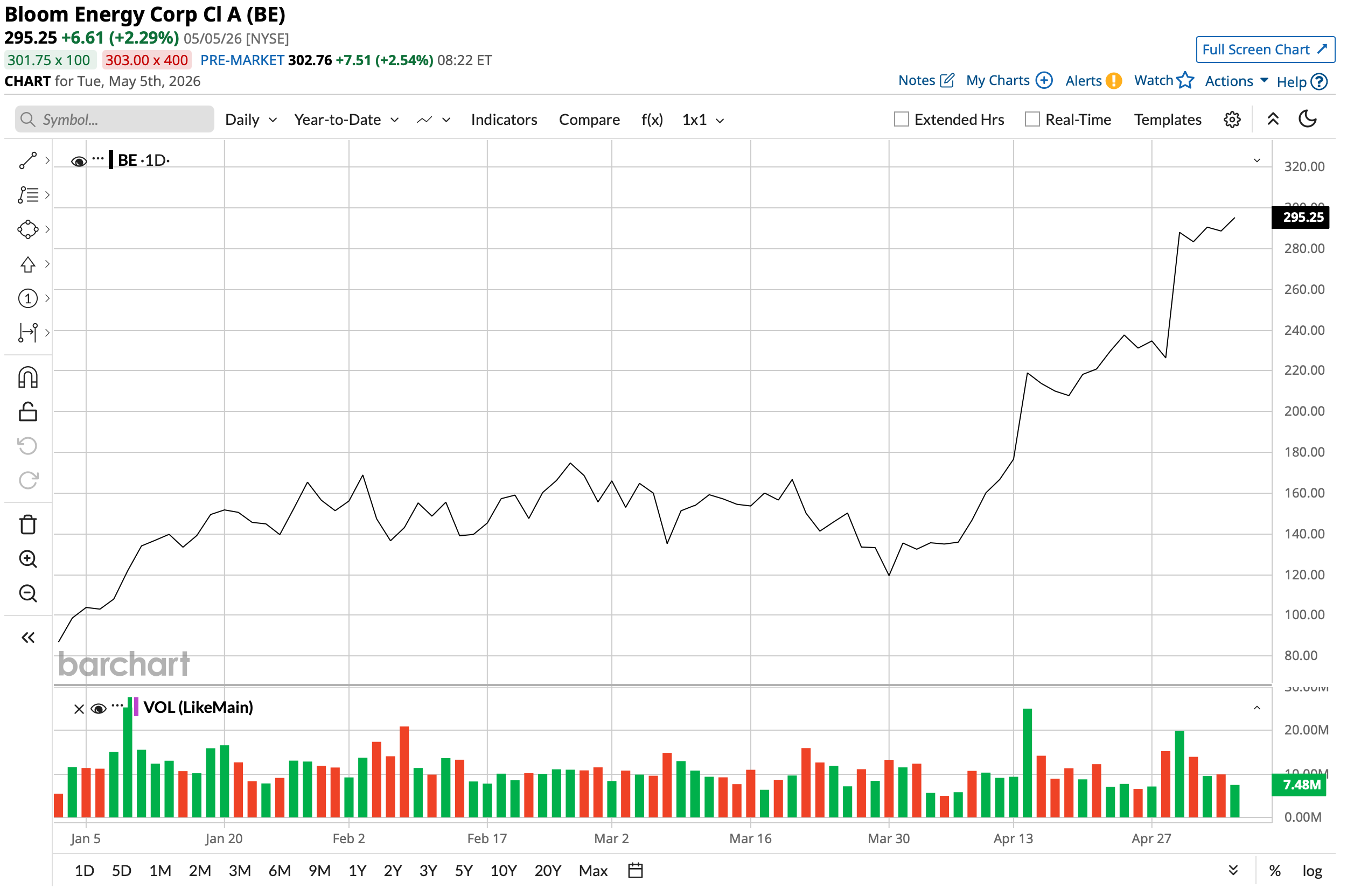

Valued at a market capitalization of $82.83 billion, BE stock is up an impressive 228.58% year-to-date (YTD).

Thus, with a credible firm like RBC Capital reaffirming its bullish stance on Bloom, is its stock an undisputed “Buy”?

Strong Q4 With Punchy Valuations

Bloom Energy brought 2025 to a close on a strong note, with record revenues, a substantial backlog, and earnings that cleared expectations by a comfortable margin. The fourth quarter delivered revenues of $777.7 million, a gain of nearly 36% compared to the same period a year earlier. The product segment, which sits at the heart of the company's revenue base, grew 35% on an annual basis to reach $638.5 million, while the company wrapped up the year carrying a backlog of $20 billion, a figure that speaks to the depth of demand sitting ahead of it.

On the earnings front, diluted EPS came in at $0.45, essentially flat relative to the $0.43 reported in the year ago period, though the result cleared the Street's consensus estimate of $0.31 by a wide margin. Operating cash flow of $418.1 million represented a modest step down from the $484.2 million generated in the prior year, with pressure on net profits flowing through into the cash generation figure. The company ended the quarter holding a cash balance of $2.45 billion.

The strength of the financial results and the rally in the share price have combined to push valuations into territory that warrants attention. Specifically, the RSI stands at 71.93 in the overbought area. Bloom Energy currently trades at a forward price-to-earnings multiple of 138.79 times, a price-to-sales ratio of 22.61 times, and a price-to-cash-flow multiple of 297.70 times. Each of these sits at a pronounced premium relative to the corresponding sector medians, reflecting a market that has priced in a great deal of future execution from a company that is still in the earlier stages of demonstrating its full earnings potential.

What Next?

In a recent analysis of Bloom, I had focused on what makes the company unique in the energy space. That has led to cloud infrastructure services provider Oracle (ORCL) choosing Bloom as its energy partner, too.

However, there are increasing signs that Bloom's rally was not a mere flash in the pan. A major development to that end is on the product side, and the transition to an 800-volt DC architecture. All product shipments are now 800V DC-ready, and management has positioned this as a meaningful differentiator for data centers. This eliminates the 10-15% energy loss typical of AC-to-DC conversion in traditional data centers, which matters enormously at scale when one's talking about facilities consuming hundreds of megawatts. Management describes the new 800-volt DC solution as industry-leading, saying this will make Bloom the standard in data centers by supporting higher efficiency, modernization, and accelerating adoption by major customers.

The second major product track is the Bloom Electrolyzer, which is the company's solid oxide electrolyzer cell (SOEC) offering for hydrogen production. The Bloom Electrolyzer operates at 37.5 kWh per kilogram of hydrogen, which is 20-25% better than competing PEM or alkaline systems. The efficiency advantage here stems from the same high-temperature solid oxide platform that underpins its core fuel cell product. So Bloom is essentially leveraging decades of manufacturing and R&D into a second product line.

In 2024, Bloom also announced a hydrogen solid oxide fuel cell capable of 60% electrical efficiency and 90% high-temperature combined heat and power efficiency, which opens the door for carbon-free hydrogen to be used as a direct fuel input into its Energy Servers. That creates a closed-loop narrative: Bloom's electrolyzer produces hydrogen, and Bloom's fuel cell burns it cleanly, positioning the company as a vertically coherent player in the hydrogen economy rather than just a component supplier.

Finally, there's an international dimension that deserves attention beyond the AI headline. The 2025 partnerships with France-based GTT and Ponant for marine applications, along with an installation for Japan's MOL, show a clear intent to capture the global maritime decarbonization market.

Analyst Opinion

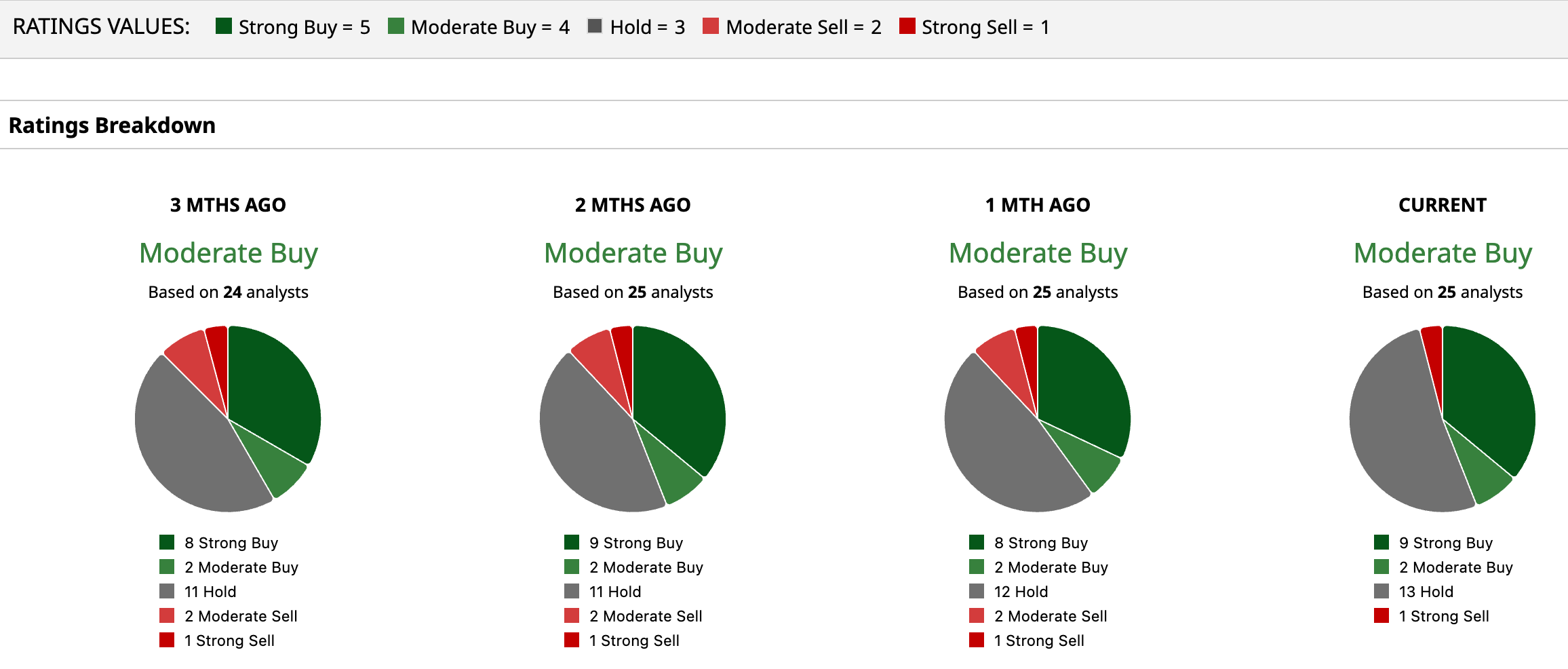

Thus, analysts have deemed BE stock as a “Moderate Buy”. While the mean target price has already been surpassed, the high target price of $335 (which is by RBC itself) indicates an upside potential of 17.1% from current levels. Out of 25 analysts covering BE stock, nine have a “Strong Buy” rating, two have a “Moderate Buy” rating, 13 analysts have a “Hold” rating, and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart