Top digital banking platforms in Canada with competitive interest rates, minimal fees, and polished mobile experiences that actually help grow your everyday cash.

KOHO

Up to 3.5% interest on balances

Up to 2% cash back on essentials

Strong money management tools

No physical branch access

Tiered monthly plans available

Pricing ranges from $0 to $14.75/month

Tangerine

No-fee daily chequing account

Free access to Scotiabank ATMs

Strong investment tools

Promotional rates drop after expiry

Limited physical café presence

$0/month pricing

Simplii Financial

Free unlimited Interac e-Transfers

Backed by CIBC

Built-in global money transfers

Not available in Quebec

No dedicated physical branches

$0/month pricing

TD Canada Trust

Large branch and ATM network

AI-powered app features

Strong wealth management integration

Higher monthly fees without minimum balances

Lower standard savings rates

Pricing ranges from $3.95 to $29.95/month

How Canadian Banking Has Changed

Digital payments have become the default across Canada. Last year, over 23.3 billion transactions moved through Canadian payment infrastructure, totalling $12.7 trillion. Cash? It's dropped to roughly 12 percent of national payment volume. Most Canadians now rely on their phone or debit card for groceries, bill-splitting, and budgeting.

And yet, a surprising number of people are still stuck with outdated banking experiences that charge steep monthly fees. Sound familiar? If your money's just sitting in a low-yield account, you're leaving real growth on the table.

Financial stress is dominating the national conversation right now. 79 percent of Canadian workers say their income isn't keeping pace with basic living costs. That's a big deal, and it makes the case for switching to a platform that actually rewards your financial habits.

The banking landscape has shifted well beyond traditional branch networks. The most competitive platforms now offer aggressive savings growth, streamlined digital interfaces, and cash back on everyday purchases. Below, you'll find a breakdown of the most rewarding digital banking options available right now.

Canada's regulatory environment is also creating a unique window for proactive consumers. A framework for consumer-driven banking has been introduced, but regulators have taken a cautious stance on a full open banking rollout. That hesitation leaves many legacy institutions comfortable charging high fees for basic digital services.

You don't have to wait around for institutional progress to catch up. Ambitious Canadians are already moving their funds into fintech platforms offering higher yields and automated savings tools. Taking that step puts you in control of your own financial growth, rather than leaving it to a slow-moving bank.

What Makes a Great Digital Bank

Convenience and smart features are quickly overriding traditional brand loyalty, especially among younger Canadians. A recent Leger study found that 64 percent of those aged 18 to 24 are open to adopting new financial products from digital-only firms. That tells you a lot about where the market is heading.

So what actually matters when picking a digital bank? Here's what to look for:

Interest rates on everyday balances: Does your cash actually grow while it sits in the account?

Fee structures: Are monthly maintenance charges and e-Transfer fees eliminated, or just buried?

Digital experience: Seamless mobile deposits, real-time spending analytics, and intuitive navigation are table stakes now.

Security: Bank-level encryption and deposit insurance protection (like CDIC coverage) aren't optional.

KOHO

If you want an account that builds wealth while handling daily expenses, KOHO is worth a close look. It pairs the convenience of a spending platform with the growth of a high-interest savings account, so your entire cash balance earns up to 3.5 percent interest. That rate is calculated daily and paid out monthly, which means your money doesn't just sit there.

Major institutions are testing tokenized bonds and digital dollars, but agile fintech platforms are already delivering real value directly to consumers. The platform removes the traditional friction between short-term spending and long-term saving goals. Plus, you get a prepaid Mastercard earning up to 2 percent cash back on essentials like groceries, transportation, and dining.

Over two million Canadians currently use the platform to get more from their everyday balances. Automated features like RoundUps and Vaults let you stash away extra cash without thinking about it. Adoption of alternative banking platforms continues to show resilient growth across the country, which says a lot about how ready people are to switch.

There's a free 30-day trial on premium tiers, so you can test the highest earning potential before committing. Accounts opted into earning interest are eligible for up to $100,000 in CDIC protection. That gives you the deposit security of a legacy bank paired with a faster, more user-friendly experience.

Why KOHO Stands Out

Earn up to 3.5% interest, calculated daily and paid monthly

Up to 2% cash back on everyday essentials

Essential plan starts at $0/month with a free 30-day premium trial

Eligible for up to $100,000 CDIC protection

Best suited for users who want to grow daily balances automatically

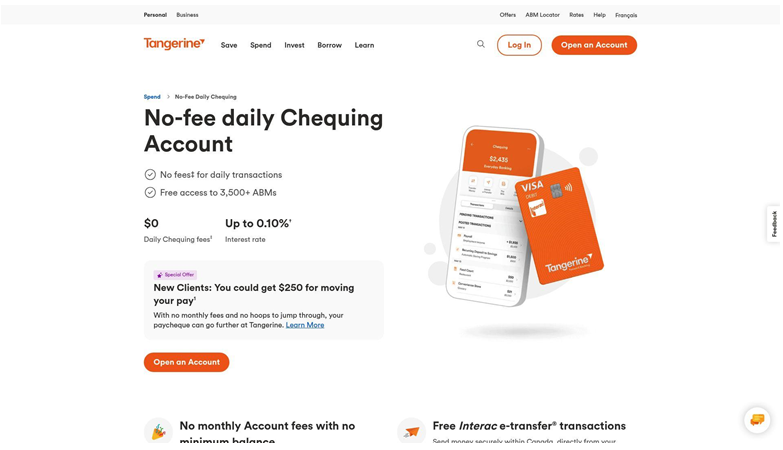

Tangerine

Tangerine pioneered direct-to-consumer digital banking in Canada, and it's still a heavy hitter for no-fee daily banking. As a wholly-owned subsidiary of Scotiabank, it gives you a digital-first interface backed by major national infrastructure. J.D. Power's 2024 study ranked Tangerine highest among mid-size banks for retail banking satisfaction.

The everyday chequing account ditches the standard monthly maintenance charges you'd find at most legacy competitors. You also get free access to Scotiabank's ATM network, so physical cash withdrawals are always within reach. It's a solid hybrid approach if you want mobile convenience without completely leaving behind traditional banking.

One thing to watch: Tangerine frequently attracts new clients with promotional rates above 2.05 percent, but those rates tend to drop after the promo window closes. The bank is currently upgrading to a cloud-native platform for faster onboarding and smarter money management tools. Global online banking users are projected to exceed 3.6 billion by 2024, and Tangerine is investing heavily in security upgrades to keep pace.

You can manage mutual fund investments, mortgages, and day-to-day spending from a single, well-rated app. For Canadians looking for a full-service alternative to expensive branch-based accounts, Tangerine delivers consistent value.

Tangerine Key Features

No monthly fee for everyday banking

Free access to all Scotiabank ATMs

Savings rates can reach up to 2.05% during promotional periods

Backed by Scotiabank with high customer satisfaction ratings

Ideal for Canadians seeking full-service no-fee banking

Simplii Financial

Simplii Financial offers a streamlined digital experience backed by the resources and stability of CIBC. It skips proprietary physical branches entirely and passes those operational savings on to you. As a leading online option, Simplii's checking account comes with zero monthly fees and unlimited free Interac e-Transfers.

Your eligible deposits are automatically covered under standard CDIC insurance, so you get the confidence of a federally regulated institution without the branch overhead. Savings rates are competitive, too; you'll currently earn up to 2.10 percent on standard daily balances. The app keeps things intentionally clean, focusing on the core features most Canadians actually use.

Where Simplii really shines is global money transfers. You can send funds internationally right from the mobile app, with transparent fees and competitive exchange rates. Over 80 countries now implement modern open banking frameworks, and that pressure is pushing institutions to modernize international payment rails.

You can also apply for fixed-rate mortgages, personal lines of credit, and mutual fund portfolios without ever visiting a branch. The main downside? It's not available in Quebec. But for digital-heavy users and frequent international senders across the rest of Canada, Simplii is hard to beat on cost.

Simplii Financial Highlights

No monthly banking fees

Free access to all CIBC ATMs

Savings rates up to 2.10%

Built-in global money transfer capabilities

Great for heavy e-Transfer users and international senders

TD Canada Trust

Still want physical branch access alongside a polished digital experience? TD Canada Trust bridges that gap better than most. As one of Canada's largest legacy banks, it offers an extensive physical presence and deep integration with platforms like TD Direct Investing. TD recently deployed AI tools to speed up back-office work, improve fraud monitoring, and shorten mortgage approval times.

The TD app consistently ranks high for mobile satisfaction, with features like instant cheque deposits and real-time spending analytics. So you get the stability of a Big Five institution with a digital experience that doesn't feel stuck in 2010.

The trade-off? Savings rates sit noticeably lower than digital-only competitors, at roughly 0.90 percent. You'll also want to maintain minimum balances to waive the standard monthly fees, which range from $3.95 to $29.95. Canada's largest banks are managing elevated credit loss provisions amid tightening economic conditions, and banking with an institution of TD's size does offer distinct stability during uncertain times.

TD remains the go-to for people with complex financial needs who sometimes require in-person support for business accounts or large loans. Cross-border banking services, wealth management features, and financial planning tools are all under one roof. If you're comfortable navigating traditional tiered account structures, TD delivers a thoroughly integrated banking environment.

TD Canada Trust Features

Monthly fees range from $3.95 to $29.95, with fee waivers available through minimum balances

Access to one of Canada's largest ATM and branch networks

AI-powered fraud detection and faster loan processing

Strong integration with wealth management services

Best for users needing in-person support and advanced financial products

Paying high monthly fees just for the privilege of having a bank hold your money? That era is over. Whether you want to grow your everyday cash balance, ditch maintenance fees, or simply use a better app, Canada's fintech market has a solution. Industry analysis from Deloitte confirms that consumer behaviour is shifting hard toward frictionless, on-demand digital services. Don't let your capital stagnate in a low-yield account that can't keep up with modern financial technology. Compare the platforms above against what you're currently paying, and ask yourself: is your bank actually working for you?

Media Contact

Name: Jay Jangid

Company: Pulse of Strategy

Email: contact@pulseofstrategy.com

Website: https://www.pulseofstrategy.com/

LinkedIn: https://www.linkedin.com/company/pulseofstrategy/