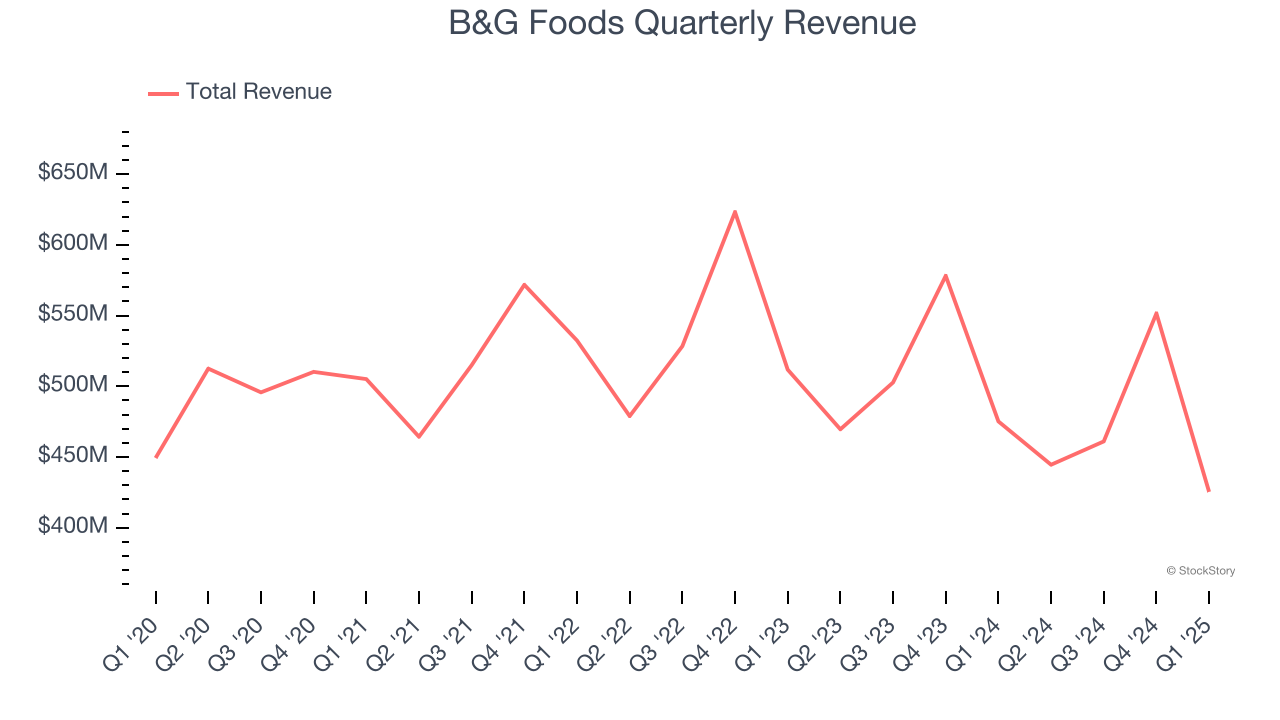

Packaged foods company B&G Foods (NYSE: BGS) missed Wall Street’s revenue expectations in Q1 CY2025, with sales falling 10.5% year on year to $425.4 million. Its non-GAAP profit of $0.04 per share was 72.1% below analysts’ consensus estimates.

Is now the time to buy B&G Foods? Find out by accessing our full research report, it’s free.

B&G Foods (BGS) Q1 CY2025 Highlights:

- Revenue: $425.4 million vs analyst estimates of $456.5 million (10.5% year-on-year decline, 6.8% miss)

- Adjusted EPS: $0.04 vs analyst expectations of $0.16 (72.1% miss)

- Adjusted EBITDA: $59.14 million vs analyst estimates of $70.48 million (13.9% margin, 16.1% miss)

- Operating Margin: 8.4%, up from -3.3% in the same quarter last year

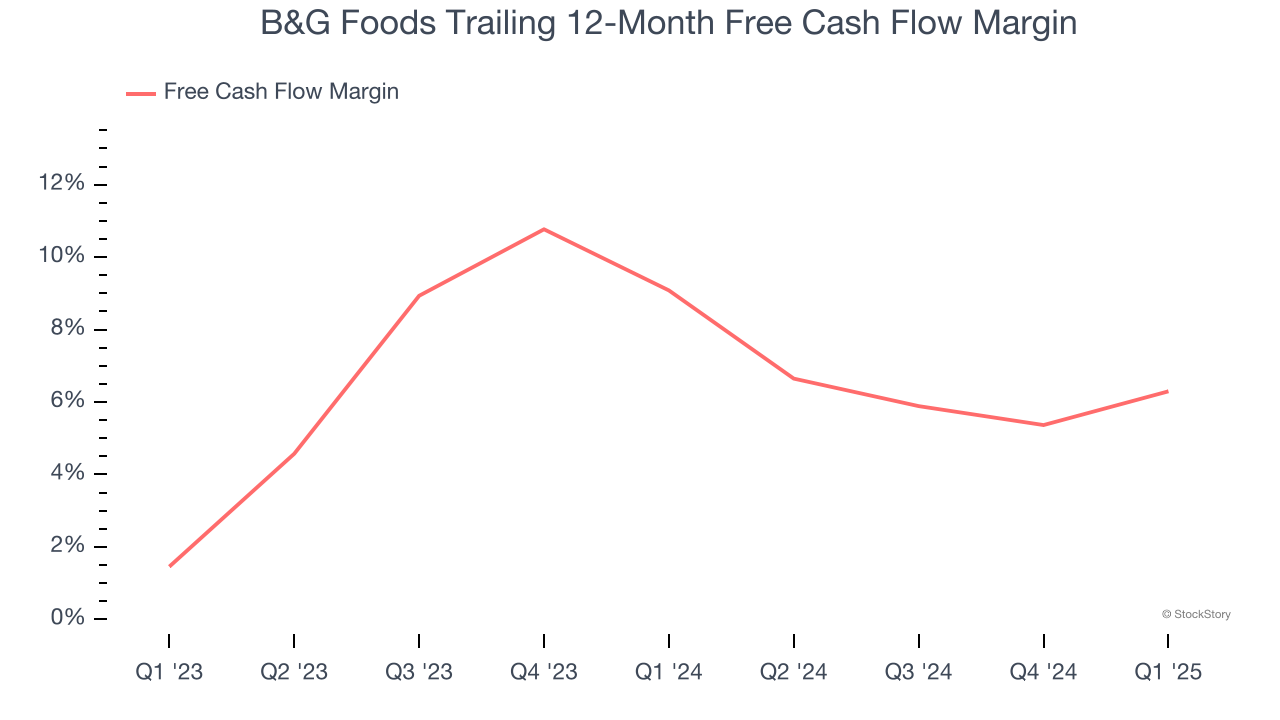

- Free Cash Flow Margin: 10%, up from 5.8% in the same quarter last year

- Market Capitalization: $503.5 million

Commenting on the results, Casey Keller, President and Chief Executive Officer of B&G Foods, stated, “Our first quarter results reflect the challenging environment in the packaged foods industry at the start of 2025, including the impact of retailer inventory reductions and a shift in Easter timing into the second quarter. While January and February were especially difficult, recent net sales in March, April and early May have begun to show stabilizing trends versus last year. We remain laser focused on our critical priorities: improving our core business net sales trends, reshaping our portfolio for future growth and higher margins, and reducing leverage through divestitures and excess cash flow to facilitate strategic acquisitions. We have also accelerated our cost reduction efforts and expect to achieve significant cost savings during the remainder of the year.”

Company Overview

Started as a small grocery store in New York City, B&G Foods (NYSE: BGS) is an American packaged foods company with a diverse portfolio of more than 50 brands.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $1.88 billion in revenue over the past 12 months, B&G Foods is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, B&G Foods’s demand was weak over the last three years. Its sales fell by 3.3% annually despite consumers buying more of its products. We’ll explore what this means in the "Volume Growth" section.

This quarter, B&G Foods missed Wall Street’s estimates and reported a rather uninspiring 10.5% year-on-year revenue decline, generating $425.4 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 1.8% over the next 12 months. While this projection suggests its newer products will catalyze better top-line performance, it is still below the sector average.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

B&G Foods has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 7.7% over the last two years, better than the broader consumer staples sector. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that B&G Foods’s margin dropped by 2.8 percentage points over the last year. Continued declines could signal it is in the middle of an investment cycle.

B&G Foods’s free cash flow clocked in at $42.36 million in Q1, equivalent to a 10% margin. This result was good as its margin was 4.2 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

Key Takeaways from B&G Foods’s Q1 Results

We struggled to find many positives in these results as its revenue, EPS, and EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $4.72 immediately after reporting.

So should you invest in B&G Foods right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.