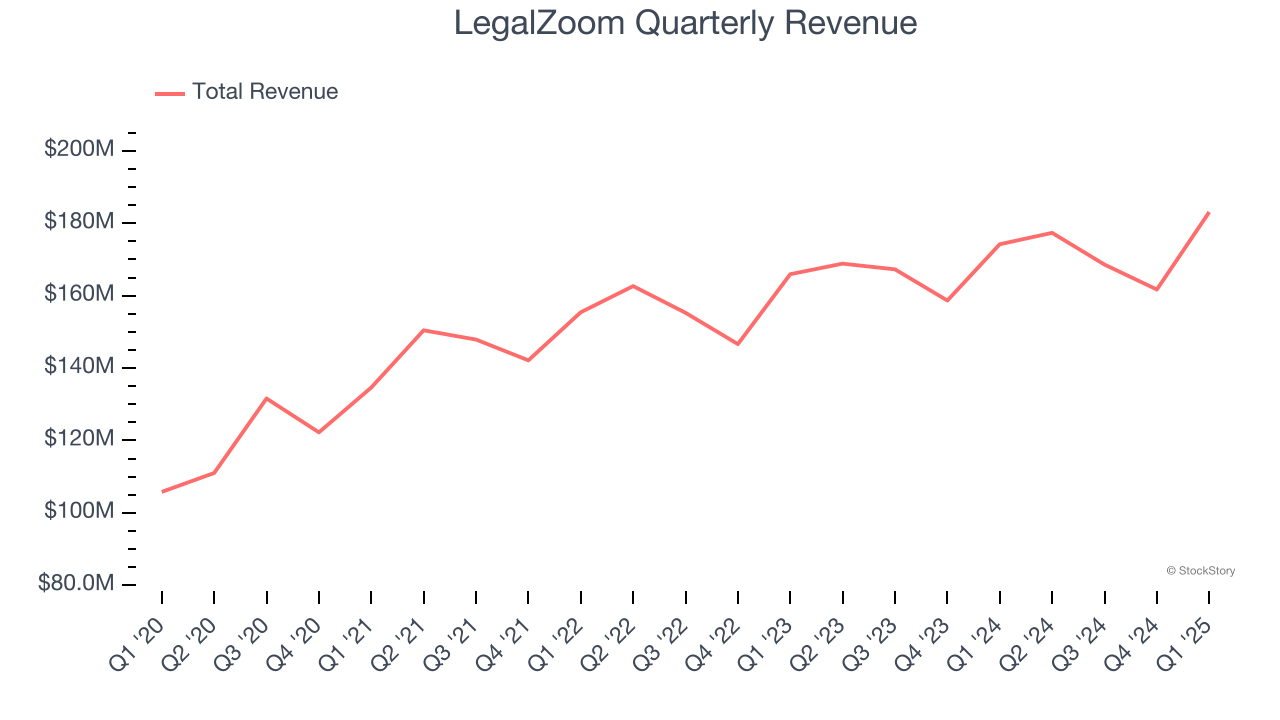

Online legal service provider LegalZoom (NASDAQ: LZ) reported Q1 CY2025 results exceeding the market’s revenue expectations, with sales up 5.1% year on year to $183.1 million. The company expects next quarter’s revenue to be around $183 million, close to analysts’ estimates. Its GAAP profit of $0.03 per share was $0.02 above analysts’ consensus estimates.

Is now the time to buy LegalZoom? Find out by accessing our full research report, it’s free.

LegalZoom (LZ) Q1 CY2025 Highlights:

- Revenue: $183.1 million vs analyst estimates of $177.2 million (5.1% year-on-year growth, 3.4% beat)

- EPS (GAAP): $0.03 vs analyst estimates of $0.01 ($0.02 beat)

- Adjusted EBITDA: $37.01 million vs analyst estimates of $34.91 million (20.2% margin, 6% beat)

- Revenue Guidance for Q2 CY2025 is $183 million at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for the full year is $165 million at the midpoint, in line with analyst expectations

- Operating Margin: 4.9%, up from 2.9% in the same quarter last year

- Free Cash Flow Margin: 22.6%, similar to the previous quarter

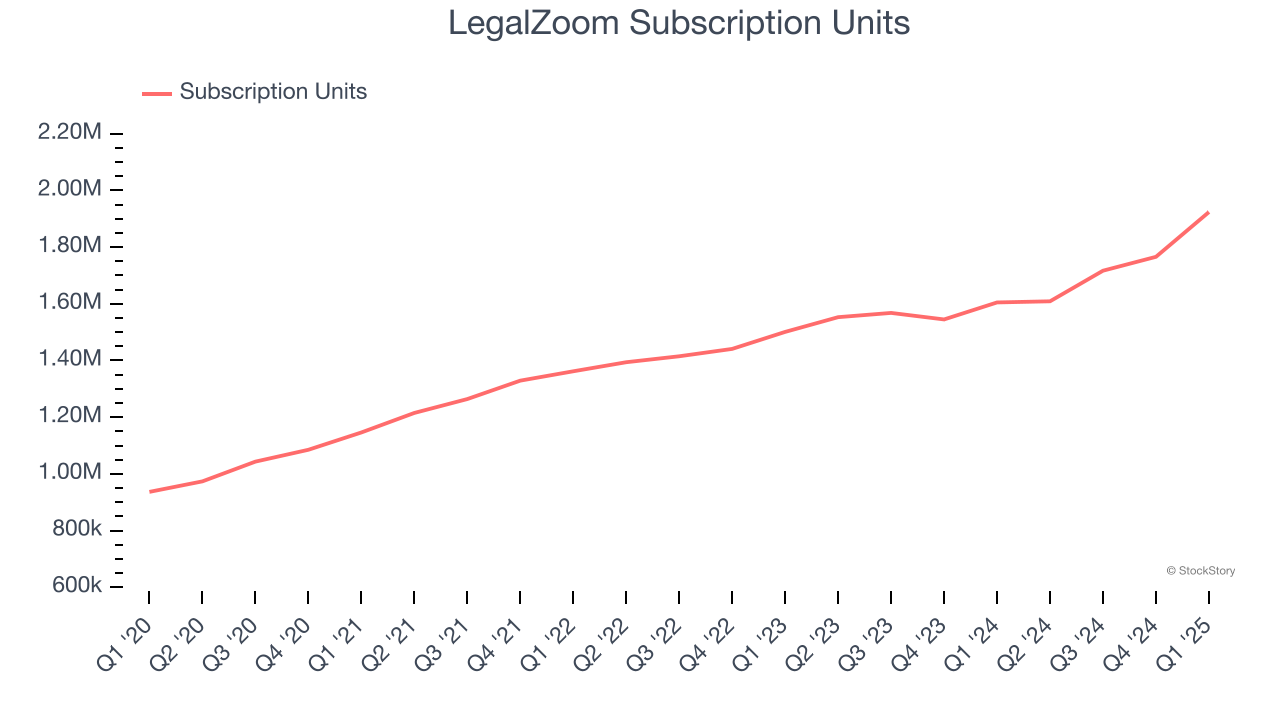

- Subscription Units: 1.92 million, up 319,000 year on year

- Market Capitalization: $1.32 billion

“Our first quarter results reflect accelerating subscription growth and solid progress towards our goal of double-digit subscription revenue growth in the fourth quarter,” said Jeff Stibel, Chairman and Chief Executive Officer of LegalZoom.

Company Overview

Founded by famous lawyer Robert Shapiro, LegalZoom (NASDAQ: LZ) offers online legal services and documentation assistance for individuals and businesses.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, LegalZoom grew its sales at a sluggish 5% compounded annual growth rate. This fell short of our benchmark for the consumer internet sector and is a poor baseline for our analysis.

This quarter, LegalZoom reported year-on-year revenue growth of 5.1%, and its $183.1 million of revenue exceeded Wall Street’s estimates by 3.4%. Company management is currently guiding for a 3.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.7% over the next 12 months, similar to its three-year rate. This projection doesn't excite us and suggests its newer products and services will not lead to better top-line performance yet.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Subscription Units

User Growth

As an online marketplace, LegalZoom generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, LegalZoom’s subscription units, a key performance metric for the company, increased by 10.5% annually to 1.92 million in the latest quarter. This growth rate is solid for a consumer internet business and indicates people are excited about its offerings.

In Q1, LegalZoom added 319,000 subscription units, leading to 19.9% year-on-year growth. The quarterly print was higher than its two-year result, suggesting its new initiatives are accelerating user growth.

Revenue Per User

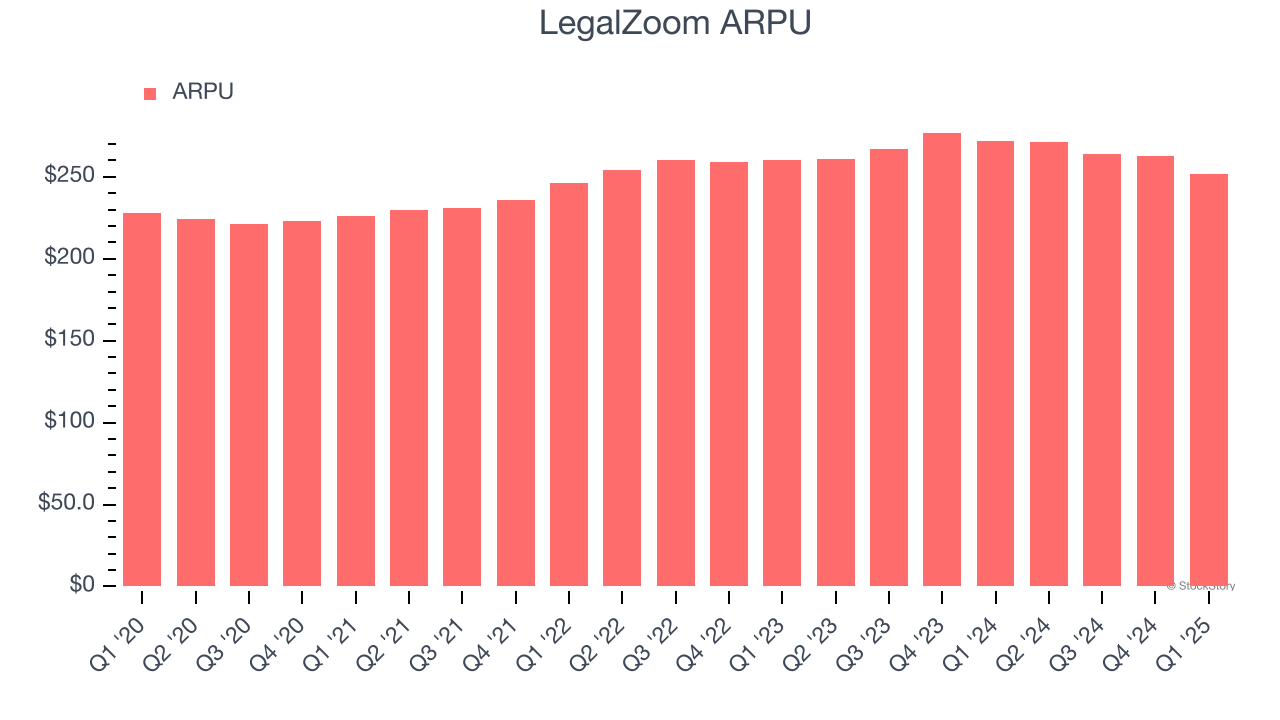

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns in transaction fees from each user. ARPU also gives us unique insights into a user’s average order size and LegalZoom’s take rate, or "cut", on each order.

LegalZoom’s ARPU has been roughly flat over the last two years. This isn’t great, but the increase in subscription units is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if LegalZoom tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether users can continue growing at the current pace.

This quarter, LegalZoom’s ARPU clocked in at $252. It declined 7.4% year on year, worse than the change in its subscription units.

Key Takeaways from LegalZoom’s Q1 Results

We enjoyed seeing LegalZoom beat analysts’ revenue, EPS, and EBITDA expectations this quarter. We were also glad its number of subscription units outperformed Wall Street’s estimates. On the other hand, its EBITDA guidance for next quarter slightly missed, though its full-year outlook was in line. Overall, we think this was a solid quarter with some key metrics above expectations. The stock traded up 8.7% to $7.90 immediately following the results.

LegalZoom put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.