Over the last six months, IQVIA’s shares have sunk to $159.91, producing a disappointing 18.5% loss - a stark contrast to the S&P 500’s 5.4% gain. This might have investors contemplating their next move.

Is there a buying opportunity in IQVIA, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is IQVIA Not Exciting?

Even though the stock has become cheaper, we're cautious about IQVIA. Here are three reasons why you should be careful with IQV and a stock we'd rather own.

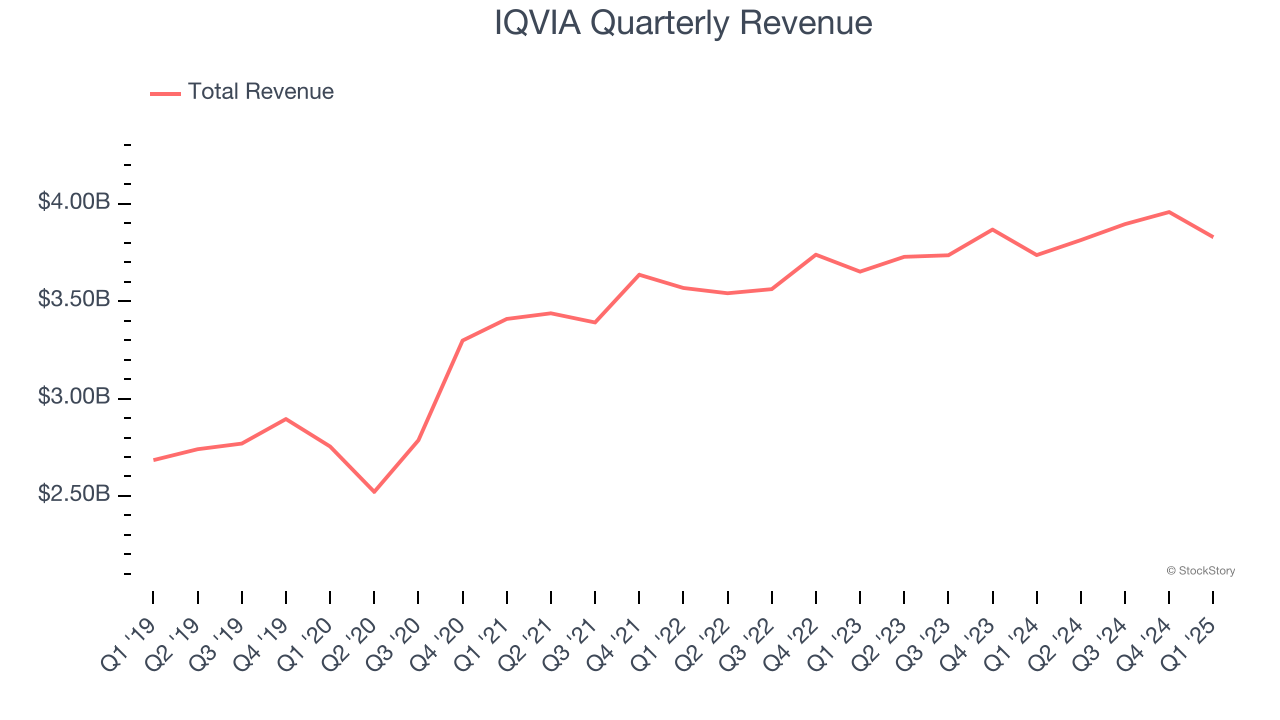

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, IQVIA’s sales grew at a mediocre 6.8% compounded annual growth rate over the last five years. This fell short of our benchmark for the healthcare sector.

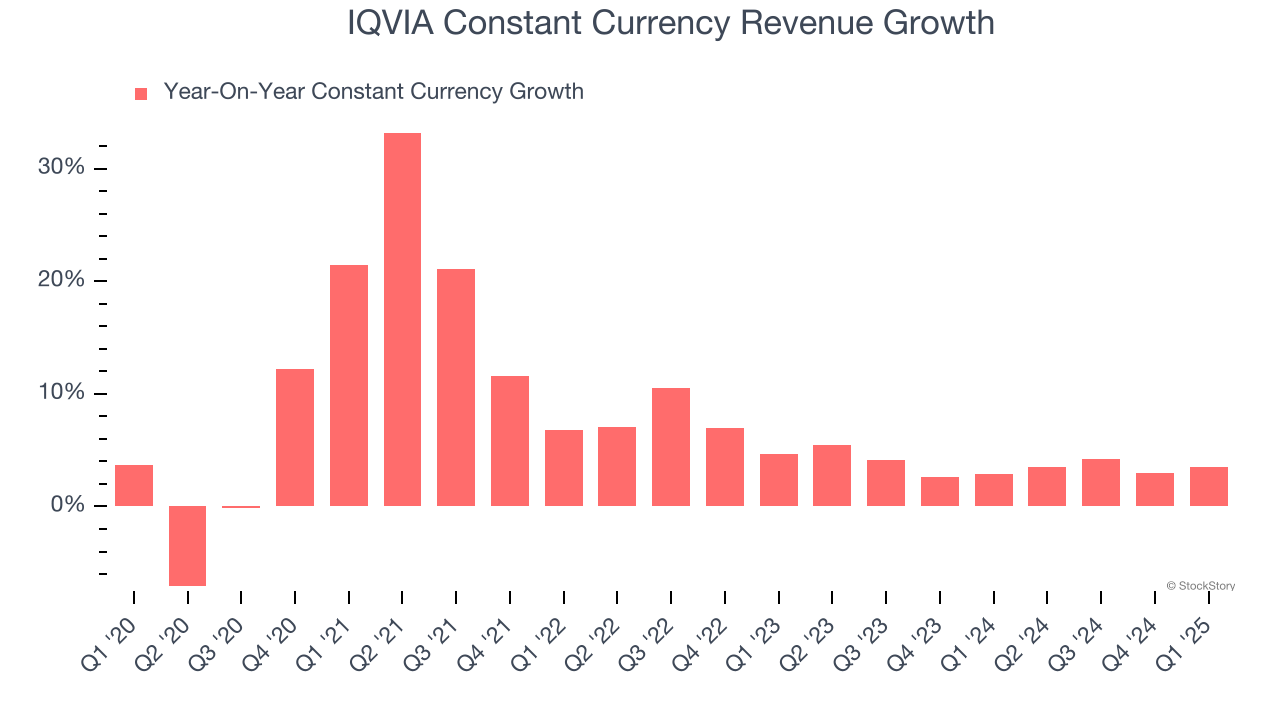

2. Weak Constant Currency Growth Points to Soft Demand

In addition to reported revenue, constant currency revenue is a useful data point for analyzing Drug Development Inputs & Services companies. This metric excludes currency movements, which are outside of IQVIA’s control and are not indicative of underlying demand.

Over the last two years, IQVIA’s constant currency revenue averaged 3.7% year-on-year growth. This performance slightly lagged the sector and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

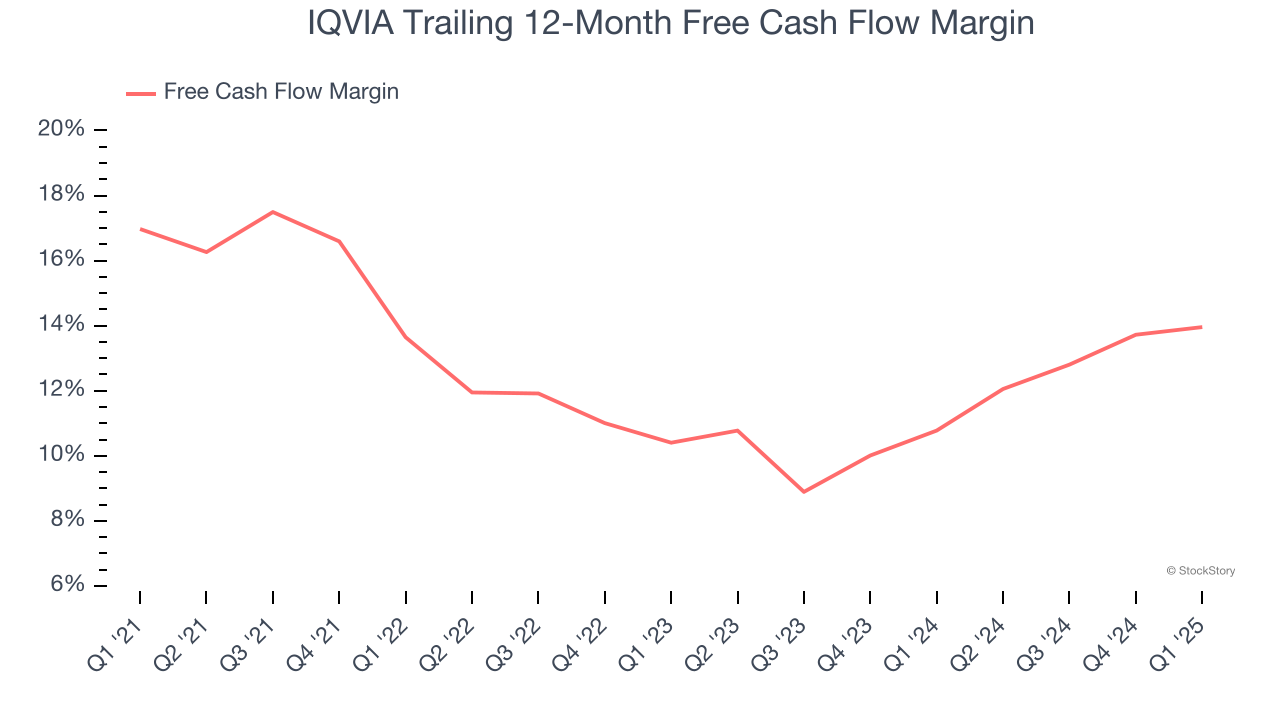

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, IQVIA’s margin dropped by 3 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal increasing investment needs and capital intensity. IQVIA’s free cash flow margin for the trailing 12 months was 14%.

Final Judgment

IQVIA’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 13.1× forward P/E (or $159.91 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at a dominant Aerospace business that has perfected its M&A strategy.

Stocks We Would Buy Instead of IQVIA

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.