Over the past six months, Best Buy’s shares (currently trading at $63.19) have posted a disappointing 13.5% loss while the S&P 500 was flat. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Best Buy, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Best Buy Will Underperform?

Despite the more favorable entry price, we're swiping left on Best Buy for now. Here are three reasons we avoid BBY and a stock we'd rather own.

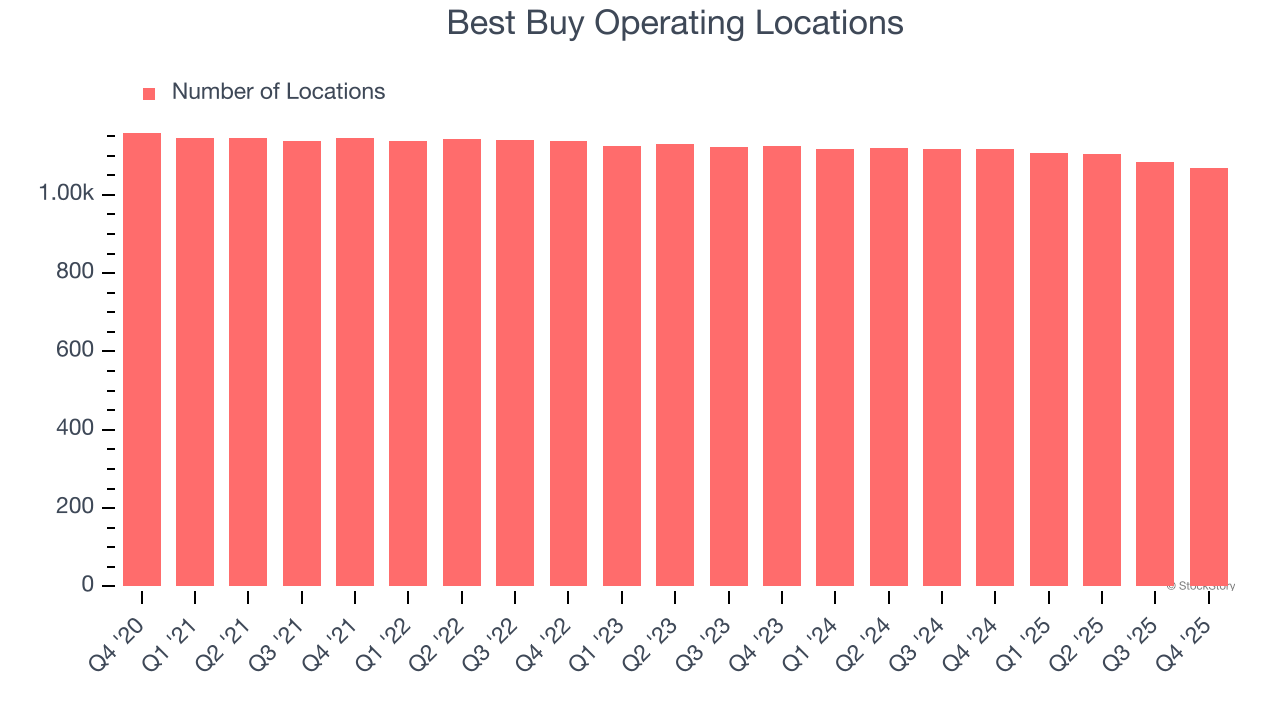

1. Stores Are Closing, a Headwind for Revenue

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Best Buy listed 1,068 locations in the latest quarter and has generally closed its stores over the last two years, averaging 1.5% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

2. Shrinking Same-Store Sales Indicate Waning Demand

Same-store sales is an industry measure of whether revenue is growing at existing stores, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Best Buy’s demand has been shrinking over the last two years as its same-store sales have averaged 1% annual declines.

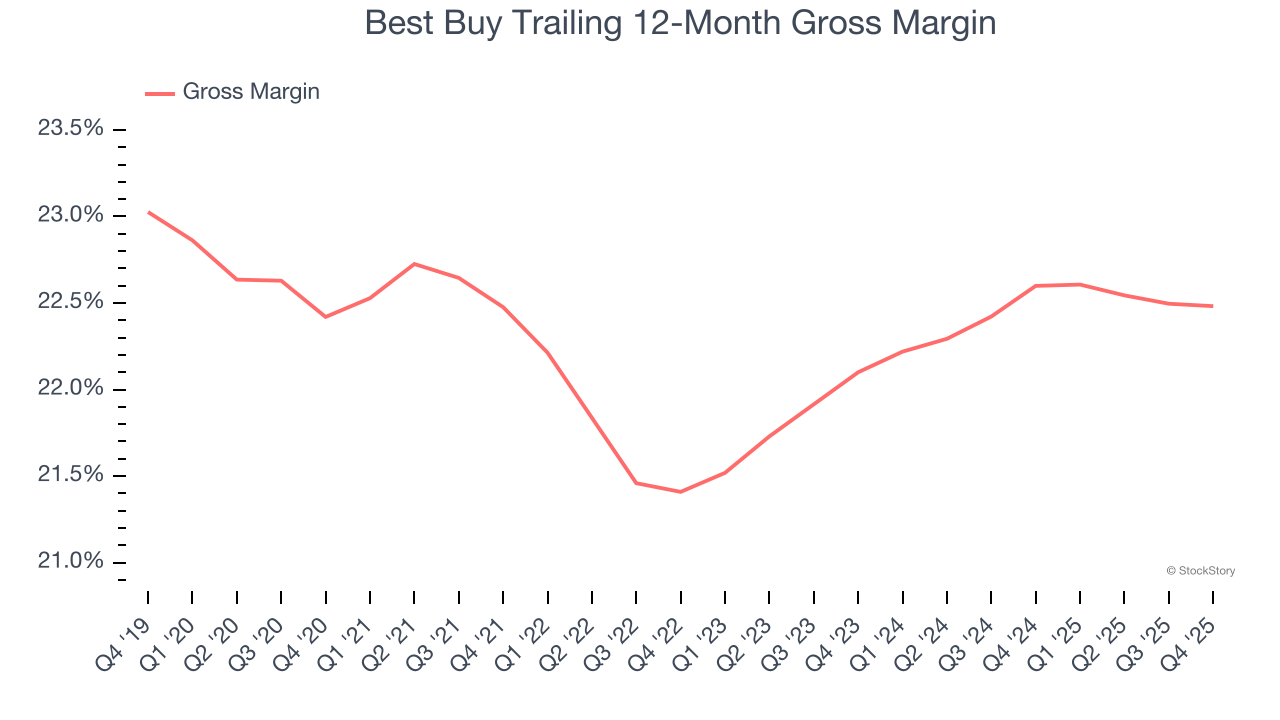

3. Low Gross Margin Reveals Weak Structural Profitability

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

Best Buy has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 22.5% gross margin over the last two years. That means Best Buy paid its suppliers a lot of money ($77.46 for every $100 in revenue) to run its business.

Final Judgment

We see the value of companies helping consumers, but in the case of Best Buy, we’re out. Following the recent decline, the stock trades at 9.8× forward P/E (or $63.19 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment. Let us point you toward the Amazon and PayPal of Latin America.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.