The past six months have been a windfall for Helix Energy Solutions’s shareholders. The company’s stock price has jumped 46.4%, hitting $9.61 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Helix Energy Solutions, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Helix Energy Solutions Not Exciting?

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are two reasons there are better opportunities than HLX and a stock we'd rather own.

1. Fewer Distribution Channels Limit its Ceiling

The size of the revenue base is a way to assess topline, and it tells an investor whether an Energy producer has crossed the line between being a more vulnerable commodity taker and a durable operating platform. Scaled businesses tend to produce and generate revenue from many wells, pads, takeaway routes, and geographies, not just a single field or drilling program.

Helix Energy Solutions’s $1.29 billion of revenue in the last year is pretty small for the industry, suggesting the company hasn’t hit a level of diversification where investors can sleep easy at night.

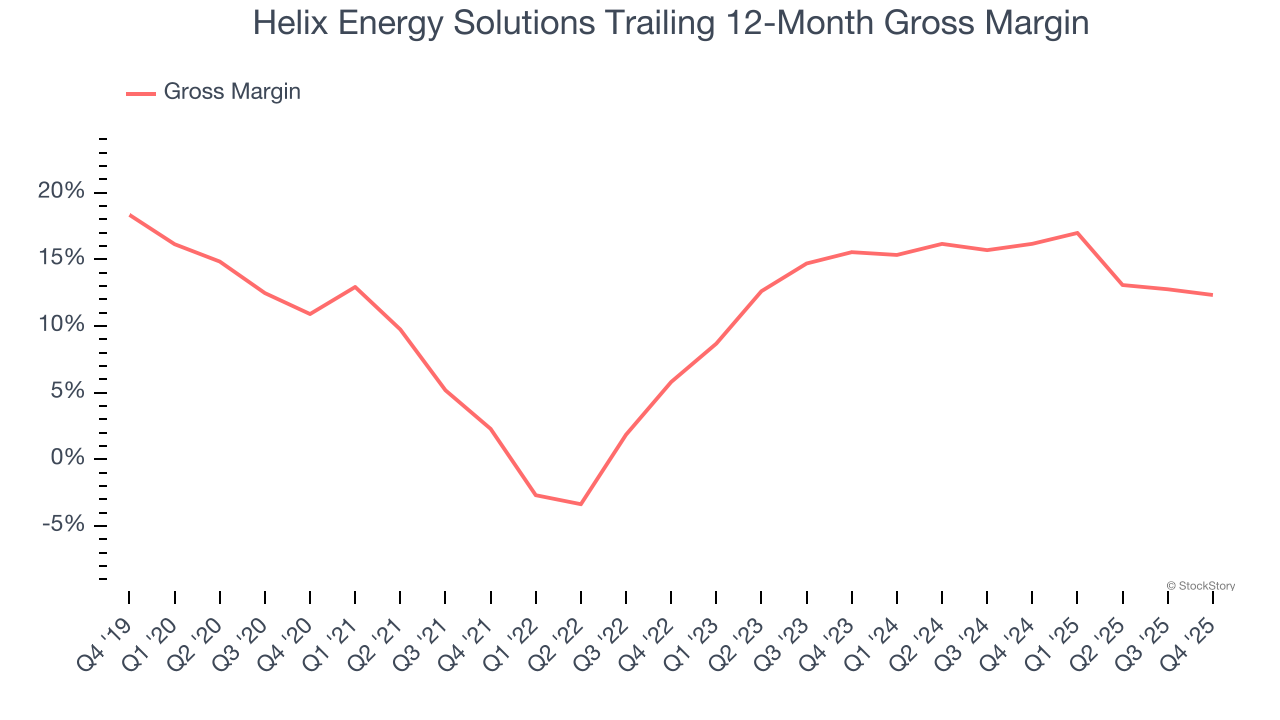

2. Low Gross Margin Reveals Weak Structural Profitability

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

Helix Energy Solutions, which averaged 11.8% gross margin over the last five years, exhibiting bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

Final Judgment

Helix Energy Solutions isn’t a terrible business, but it isn’t one of our picks. After the recent surge, the stock trades at 37.8× forward P/E (or $9.61 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. Let us point you toward one of our top software and edge computing picks.

Stocks We Like More Than Helix Energy Solutions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.