Shareholders of Erie Indemnity would probably like to forget the past six months even happened. The stock dropped 20.5% and now trades at $253.86. This might have investors contemplating their next move.

Following the drawdown, is this a buying opportunity for ERIE? Find out in our full research report, it’s free.

Why Are We Positive On ERIE?

Operating under a unique business model dating back to 1925, Erie Indemnity (NASDAQ: ERIE) serves as the attorney-in-fact for Erie Insurance Exchange, managing policy issuance, claims handling, and investment services for this reciprocal insurer.

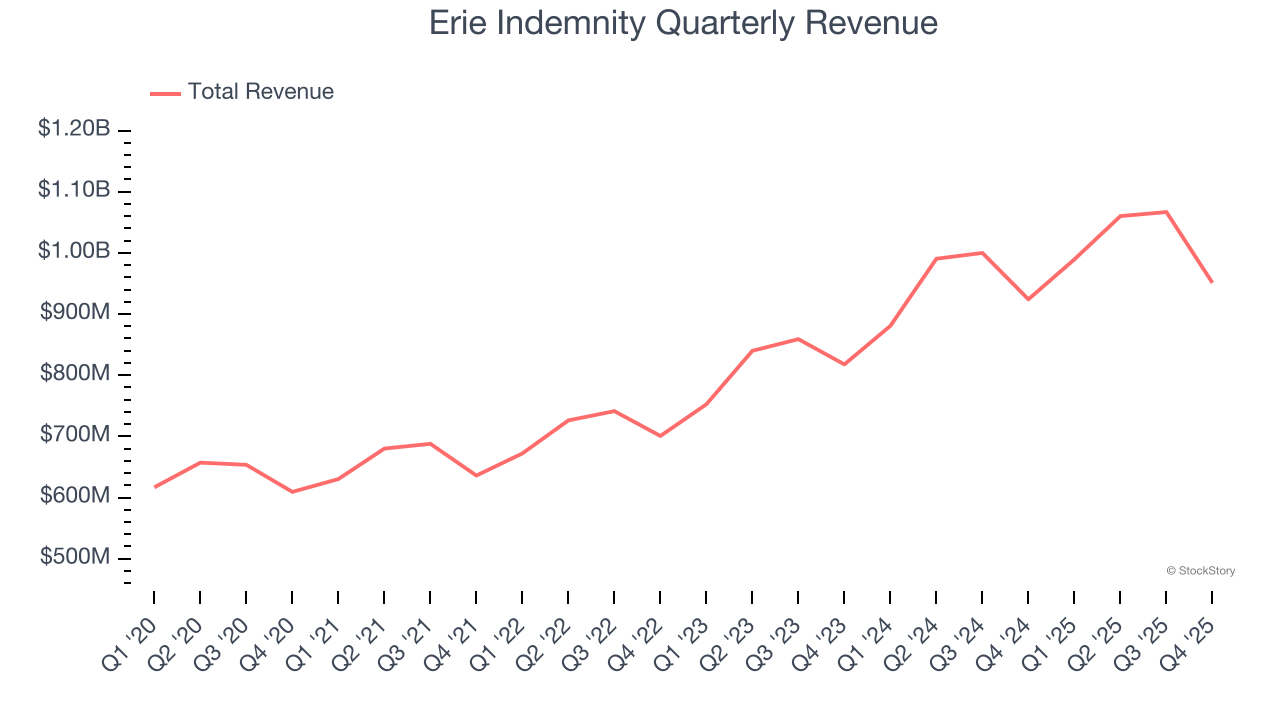

1. Long-Term Revenue Growth Shows Strong Momentum

Insurers earn revenue three ways. The core insurance business itself, often called underwriting and represented in the income statement as premiums earned, is one way. Investment income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities is the second way. Fees from various sources such as policy administration, annuities, or other value-added services is the third.

Over the last five years, Erie Indemnity grew its revenue at a solid 9.9% compounded annual growth rate. Its growth surpassed the average insurance company and shows its offerings resonate with customers.

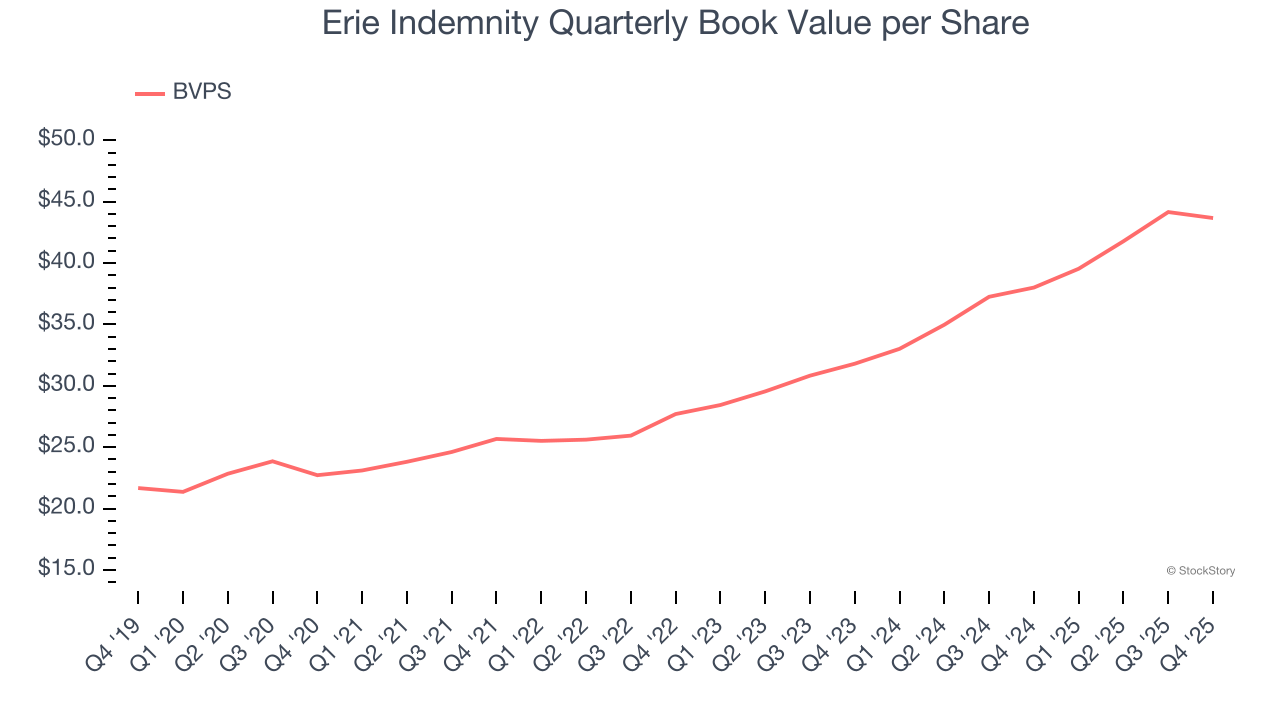

2. Steady Increase in BVPS Highlights Solid Asset Growth

In the insurance industry, book value per share (BVPS) provides a clear picture of shareholder value, as it represents the total equity backing a company’s insurance operations and growth initiatives.

Erie Indemnity’s BVPS increased by 14% annually over the last five years, and growth has recently accelerated as BVPS grew at a solid 17.2% annual clip over the past two years (from $31.80 to $43.67 per share).

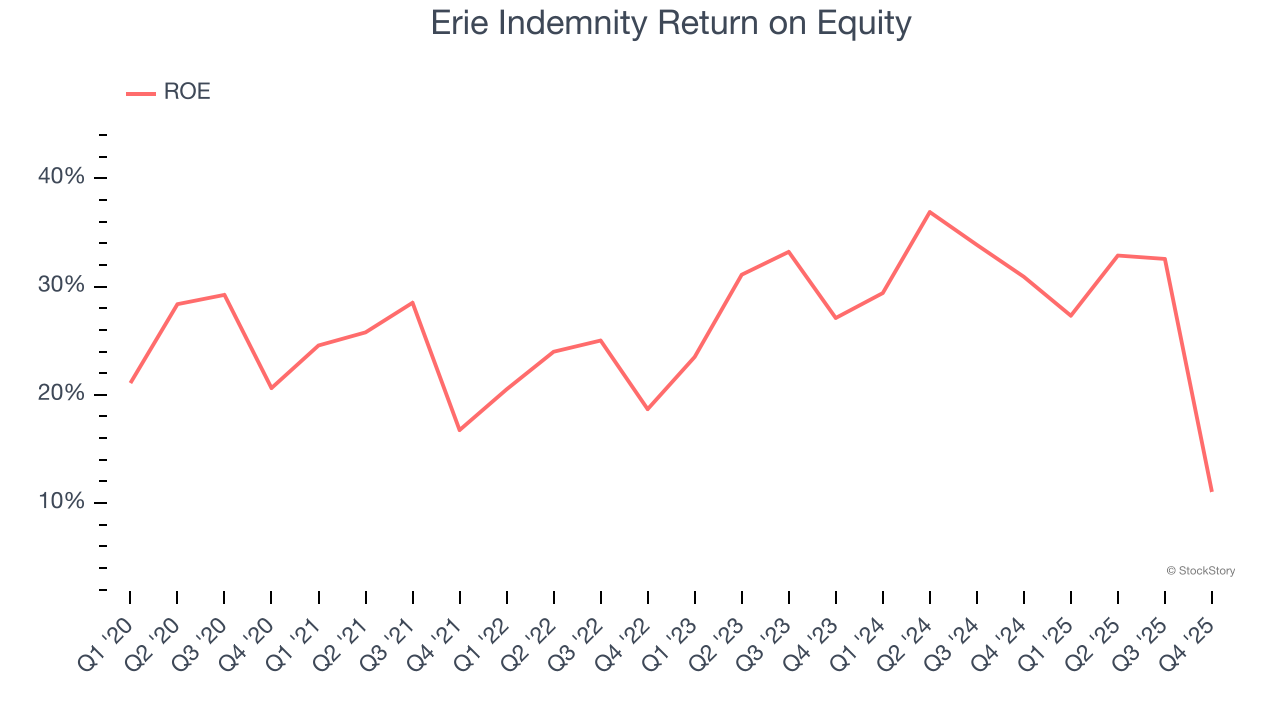

3. Stellar ROE Showcases Lucrative Growth Opportunities

Return on equity (ROE) serves as a comprehensive measure of an insurer's performance, showing how efficiently it converts shareholder capital into profits. Strong ROE performance typically translates to better returns for investors through a combination of earnings retention, share repurchases, and dividend distributions.

Over the last five years, Erie Indemnity has averaged an ROE of 26.7%, exceptional for a company operating in a sector where the average shakes out around 12.5% and those putting up 20%+ are greatly admired. This shows Erie Indemnity has a strong competitive moat.

Final Judgment

These are just a few reasons why we think Erie Indemnity is a high-quality business. After the recent drawdown, the stock trades at 19× forward P/E (or $253.86 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Erie Indemnity

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.