Sprouts has gotten torched over the last six months - since October 2025, its stock price has dropped 33.6% to $75.75 per share. This may have investors wondering how to approach the situation.

Given the weaker price action, is this a buying opportunity for SFM? Find out in our full research report, it’s free.

Why Does SFM Stock Spark Debate?

Playing on the secular trend of healthier living, Sprouts Farmers Market (NASDAQ: SFM) is a grocery store chain emphasizing natural and organic products.

Two Things to Like:

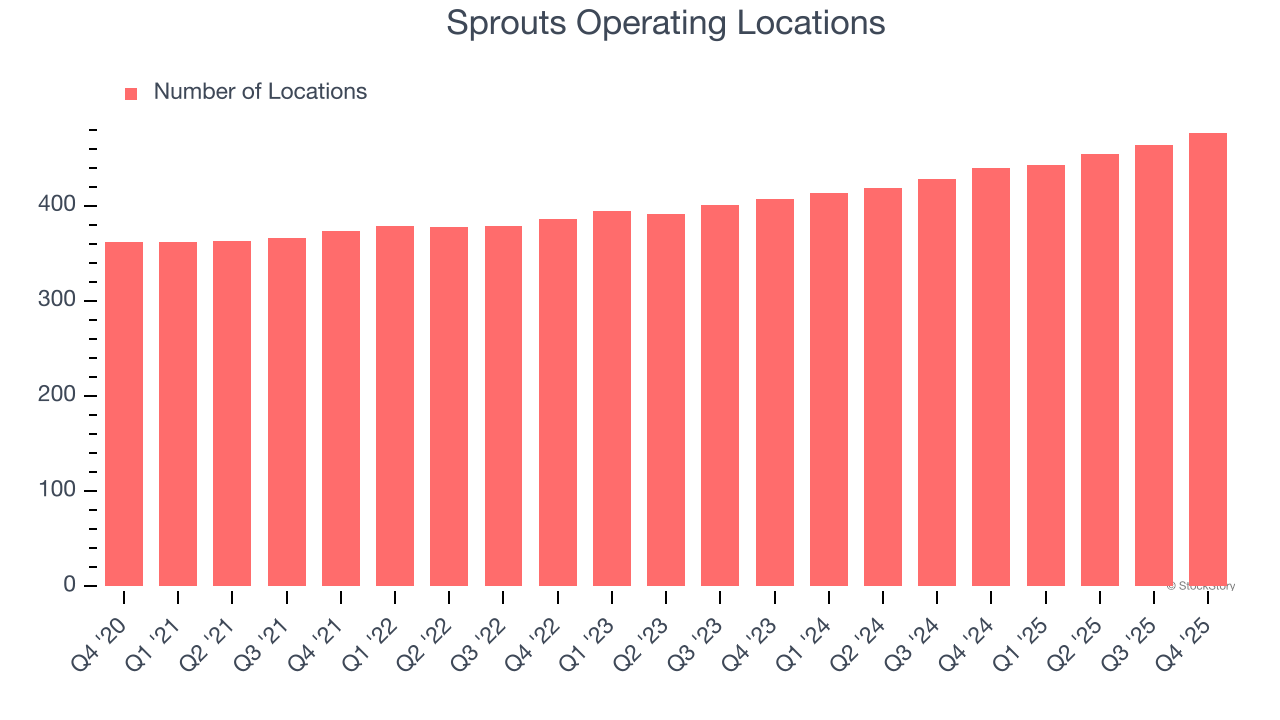

1. Store Growth Signals an Offensive Strategy

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Sprouts operated 477 locations in the latest quarter. It has opened new stores at a rapid clip over the last two years, averaging 7.4% annual growth, much faster than the broader consumer retail sector. This gives it a chance to become a large, scaled business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

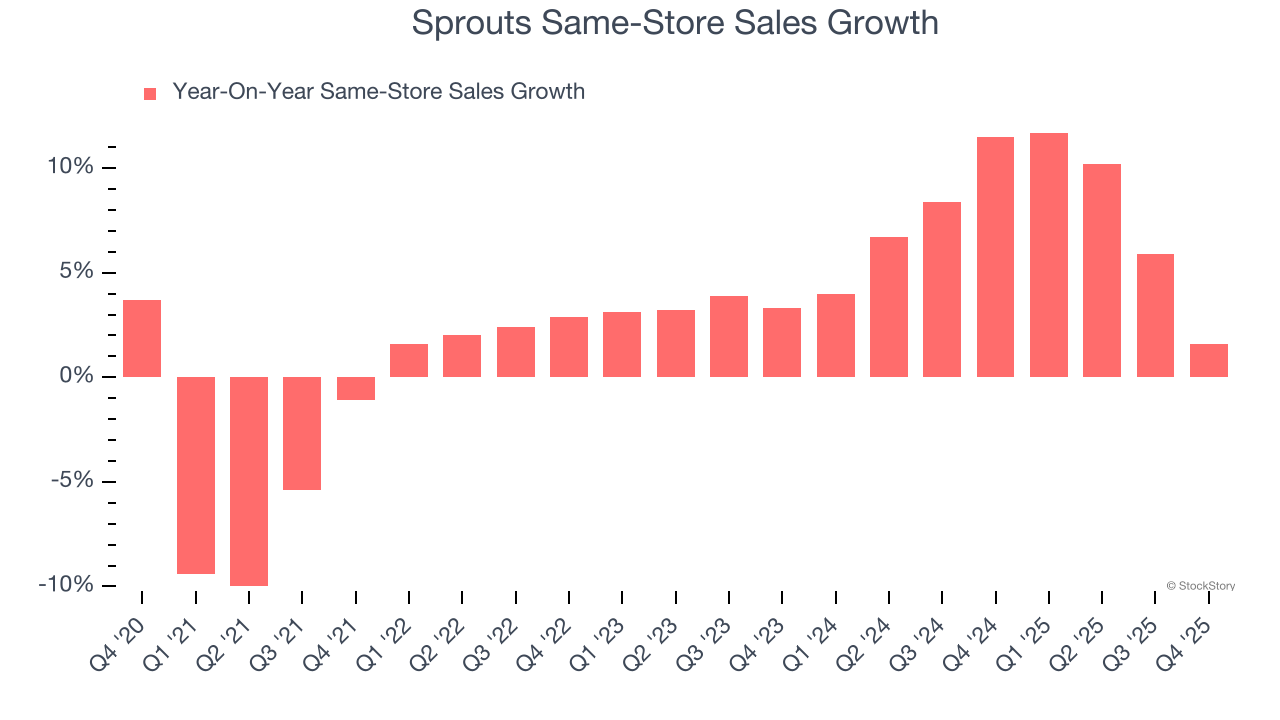

2. Surging Same-Store Sales Show Increasing Demand

Same-store sales show the change in sales for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

Sprouts has been one of the most successful retailers over the last two years thanks to skyrocketing demand within its existing locations. On average, the company has posted exceptional year-on-year same-store sales growth of 7.5%.

One Reason to be Careful:

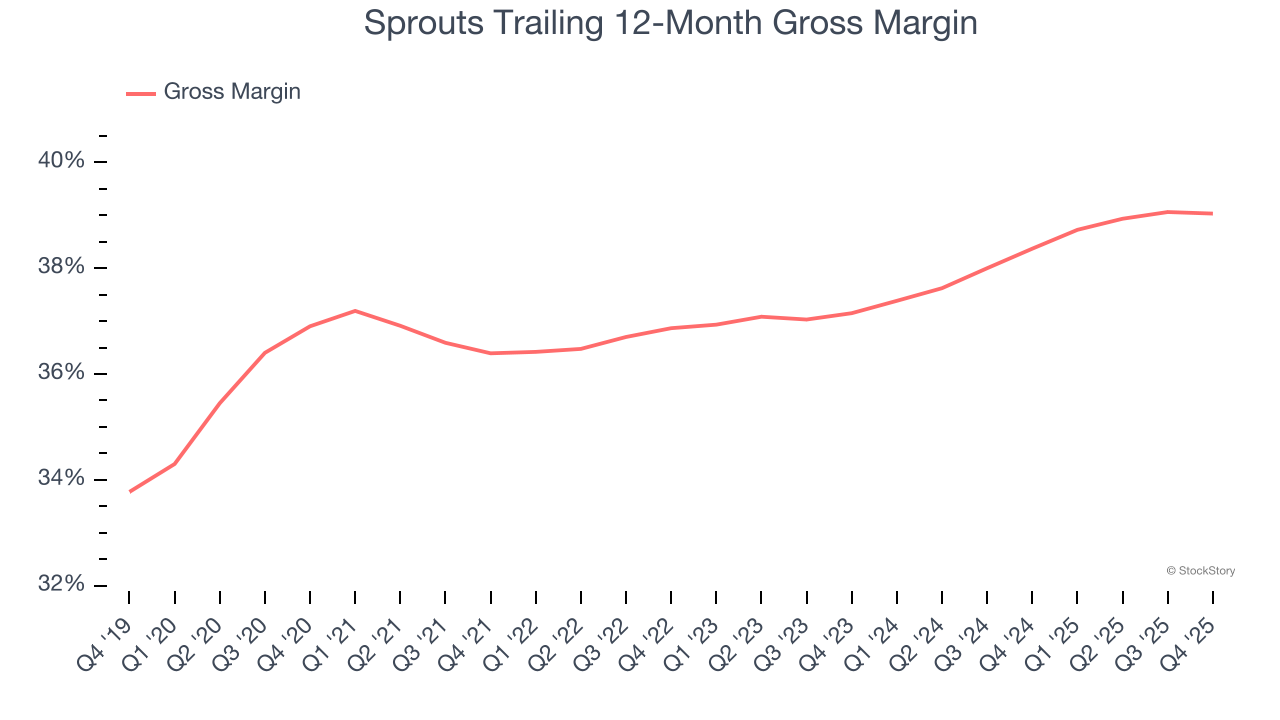

Low Gross Margin Hinders Flexibility

Gross profit margins are an important measure of a retailer’s pricing power, product differentiation, and negotiating leverage.

Sprouts’s gross margin is slightly below the average retailer, giving it less room to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged a 38.7% gross margin over the last two years. That means Sprouts paid its suppliers a lot of money ($61.28 for every $100 in revenue) to run its business.

Final Judgment

Sprouts’s merits more than compensate for its flaws. With the recent decline, the stock trades at 13.7× forward P/E (or $75.75 per share). Is now the time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Sprouts

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.