Shareholders of Gevo would probably like to forget the past six months even happened. The stock dropped 22.6% and now trades at $2.00. This might have investors contemplating their next move.

Following the pullback, is this a buying opportunity for GEVO? Find out in our full research report, it’s free.

Why Does Gevo Spark Debate?

Operating one of the largest dairy-based renewable natural gas facilities in the United States, Gevo (NASDAQ: GEVO) produces sustainable aviation fuel and other renewable hydrocarbon fuels from plant-based feedstocks like corn.

Two Positive Attributes:

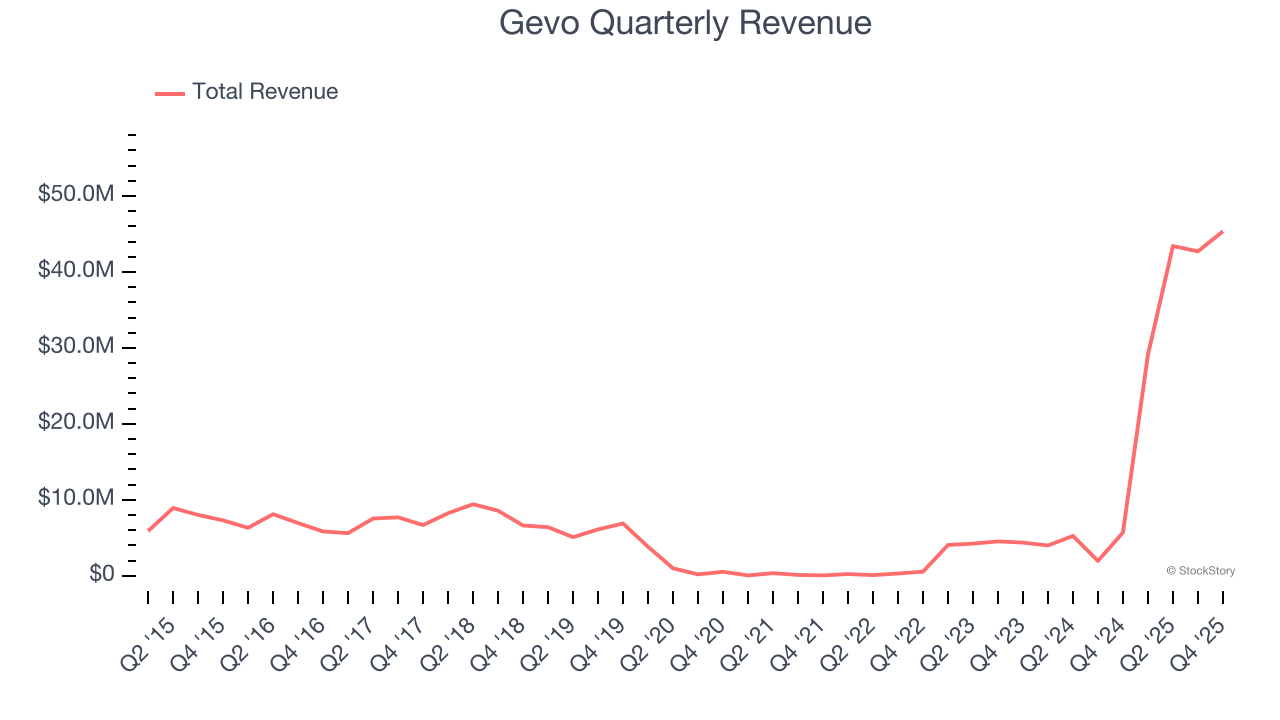

1. Skyrocketing Revenue Shows Strong Momentum

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Over the last five years, Gevo grew its sales at an incredible 96.1% compounded annual growth rate. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

2. EBITDA Margin Rising, Profits Up

Adjusted EBITDA margin is an important measure of profitability for the sector and accounts for the gross margins and operating costs mentioned previously. Unlike operating margin, it is not distorted by accounting conventions around reserves, drilling costs, and assumptions on commodity consumption from the well or basin. Adjusted EBITDA highlights the economic reality of how much cash the rock produces before the capital structure (debt service) and the drilling budget (capex) are considered.

Gevo’s EBITDA margin rose over the last year, as its sales growth gave it operating leverage. Its EBITDA margin for the trailing 12 months was 10.2%.

One Reason to be Careful:

Cash Burn Ignites Concerns

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While Gevo posted positive free cash flow this quarter, the broader story hasn’t been so clean. Gevo’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 251%, meaning it lit $251.26 of cash on fire for every $100 in revenue.

Final Judgment

Gevo’s merits more than compensate for its flaws. With the recent decline, the stock trades at 14.5× forward EV-to-EBITDA (or $2.00 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.