ThredUp has gotten torched over the last six months - since October 2025, its stock price has dropped 57% to $4.04 per share. This may have investors wondering how to approach the situation.

Is there a buying opportunity in ThredUp, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think ThredUp Will Underperform?

Even though the stock has become cheaper, we're swiping left on ThredUp for now. Here are three reasons there are better opportunities than TDUP and a stock we'd rather own.

1. Decline in Orders Points to Weak Demand

Revenue growth can be broken down into changes in price and volume (for companies like ThredUp, our preferred volume metric is orders). While both are important, the latter is the most critical to analyze because prices have a ceiling.

ThredUp’s orders came in at 1.65 million in the latest quarter, and over the last two years, averaged 7.6% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests ThredUp might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

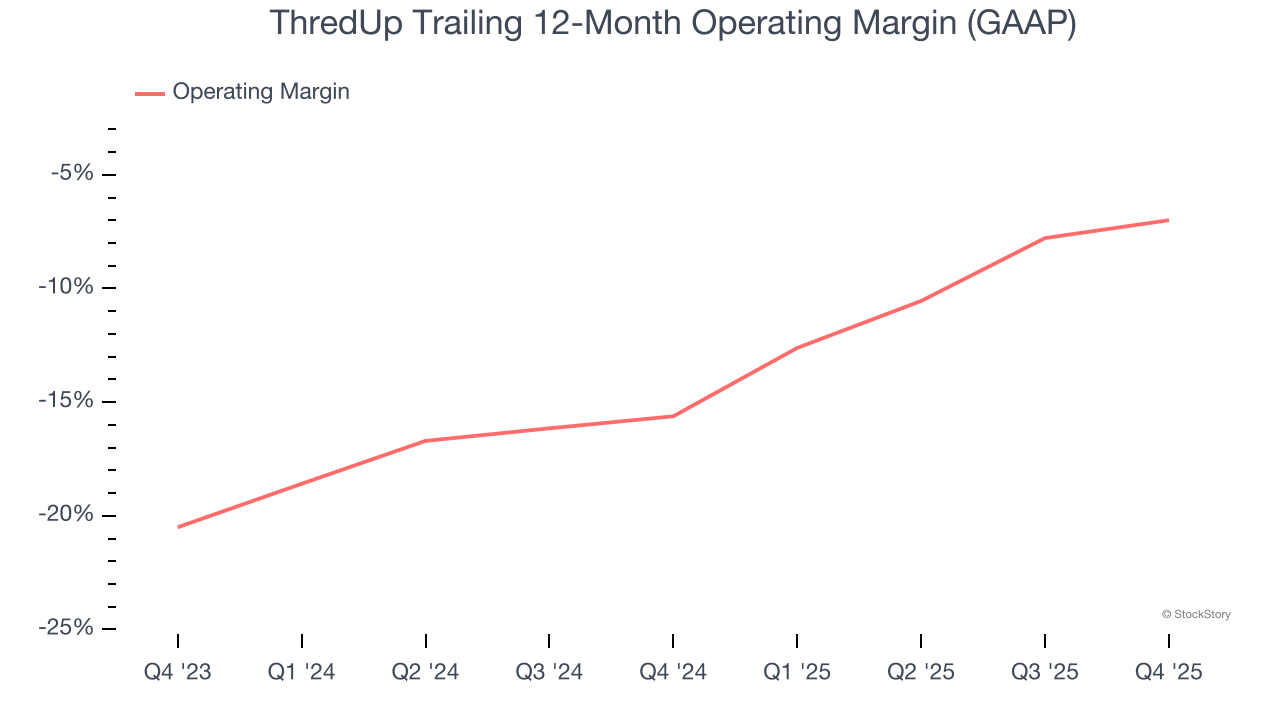

2. Operating Losses Sound the Alarms

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

ThredUp’s operating margin has been trending up over the last 12 months, but it still averaged negative 10.9% over the last two years. This is due to its large expense base and inefficient cost structure.

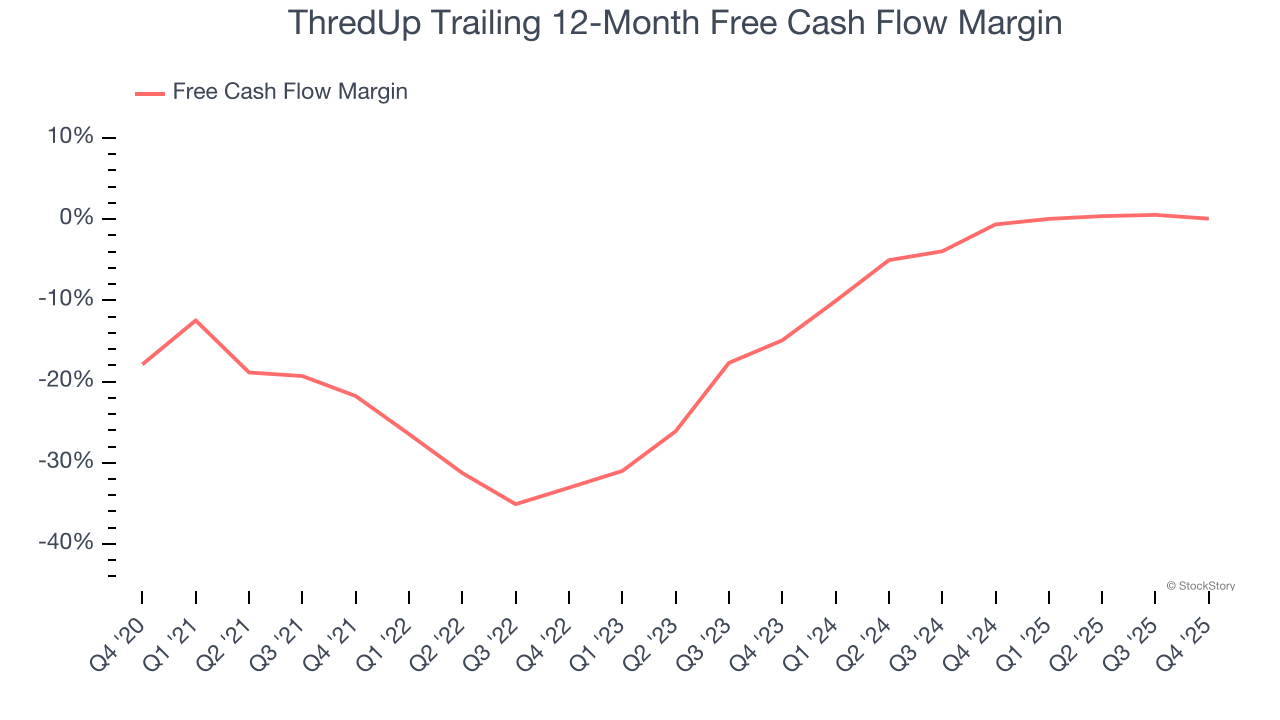

3. Breakeven Free Cash Flow Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

ThredUp broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of ThredUp, we’ll be cheering from the sidelines. Following the recent decline, the stock trades at 23.7× forward EV-to-EBITDA (or $4.04 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. We’d suggest looking at an all-weather company that owns household favorite Taco Bell.

Stocks We Like More Than ThredUp

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.