The past six months have been a windfall for Fastly’s shareholders. The company’s stock price has jumped 195%, hitting $24.56 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Fastly, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think Fastly Will Underperform?

We’re happy investors have made money, but we're cautious about Fastly. Here are three reasons there are better opportunities than FSLY and a stock we'd rather own.

1. Customer Churn Hurts Long-Term Outlook

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

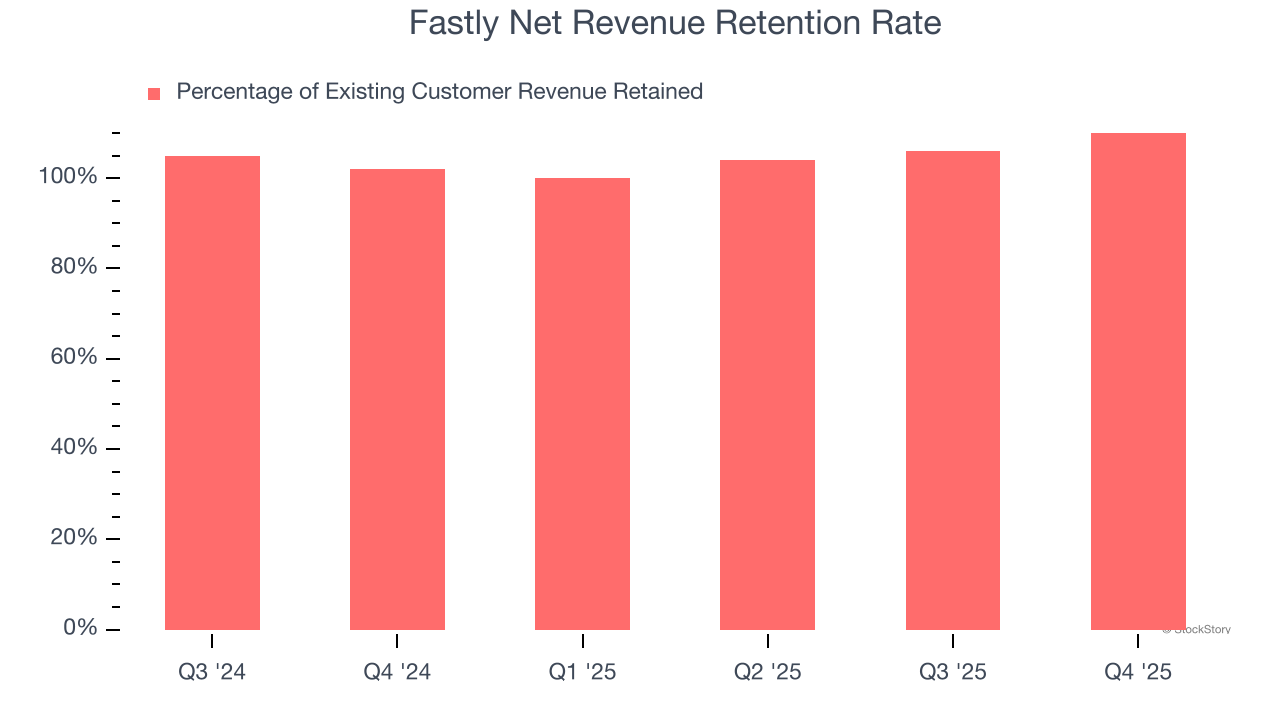

Fastly’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 105% in Q4. This means Fastly would’ve grown its revenue by 5% even if it didn’t win any new customers over the last 12 months.

Trending up over the last year, Fastly has an adequate net retention rate, showing us that it generally keeps customers but lags behind the best SaaS businesses, which routinely post net retention rates of 120%+.

2. Low Gross Margin Reveals Weak Structural Profitability

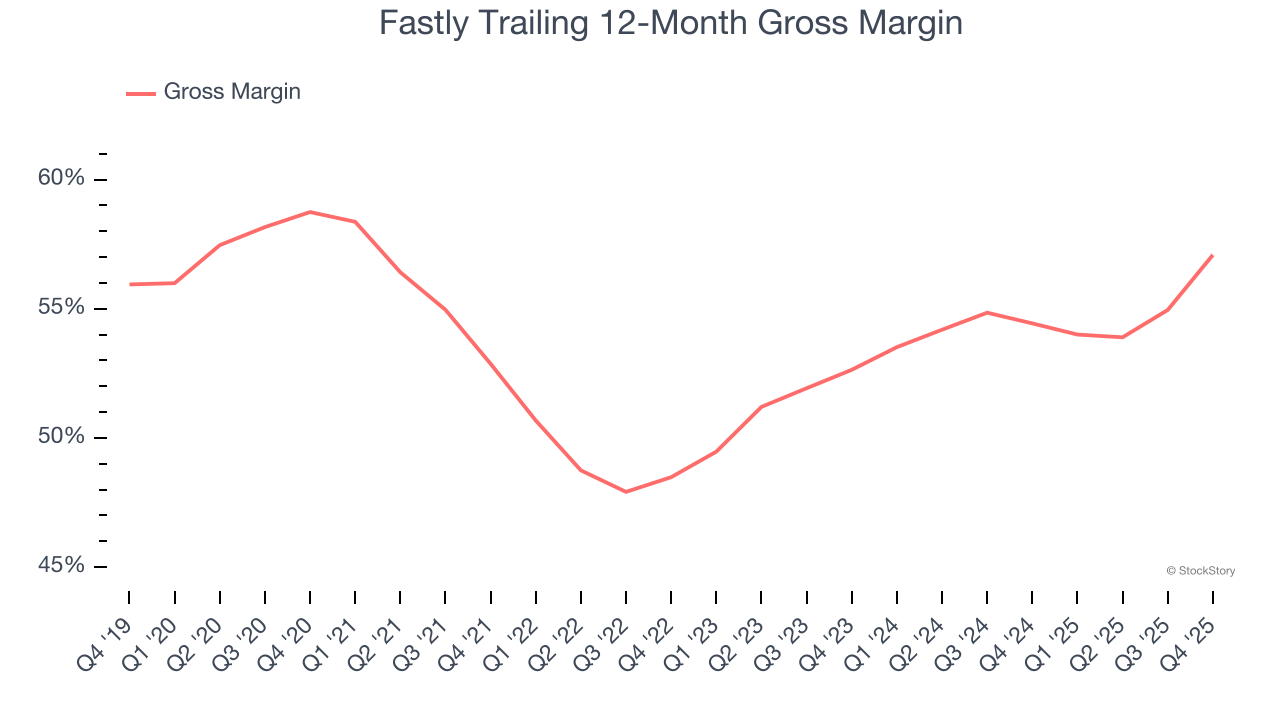

For software companies like Fastly, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Fastly’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 57.1% gross margin over the last year. That means Fastly paid its providers a lot of money ($42.92 for every $100 in revenue) to run its business.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Fastly has seen gross margins improve by 4.4 percentage points over the last 2 year, which is very good in the software space.

3. Operating Losses Sound the Alarms

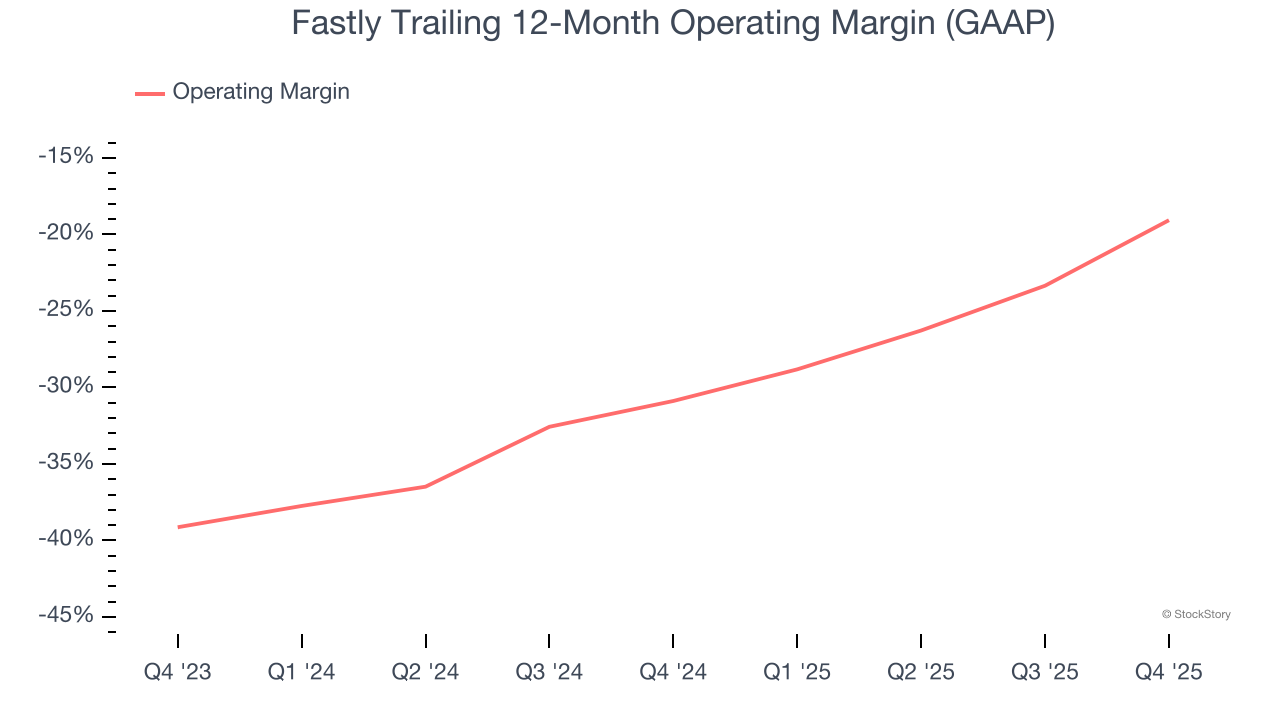

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Fastly’s expensive cost structure has contributed to an average operating margin of negative 19.1% over the last year. Unprofitable software companies require extra attention because they spend heaps of money to capture market share. As seen in its historically underwhelming revenue performance, this strategy hasn’t worked so far, and it’s unclear what would happen if Fastly reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

Final Judgment

We see the value of companies addressing major business pain points, but in the case of Fastly, we’re out. Following the recent rally, the stock trades at 5.2× forward price-to-sales (or $24.56 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. Let us point you toward a top digital advertising platform riding the creator economy.

Stocks We Like More Than Fastly

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.