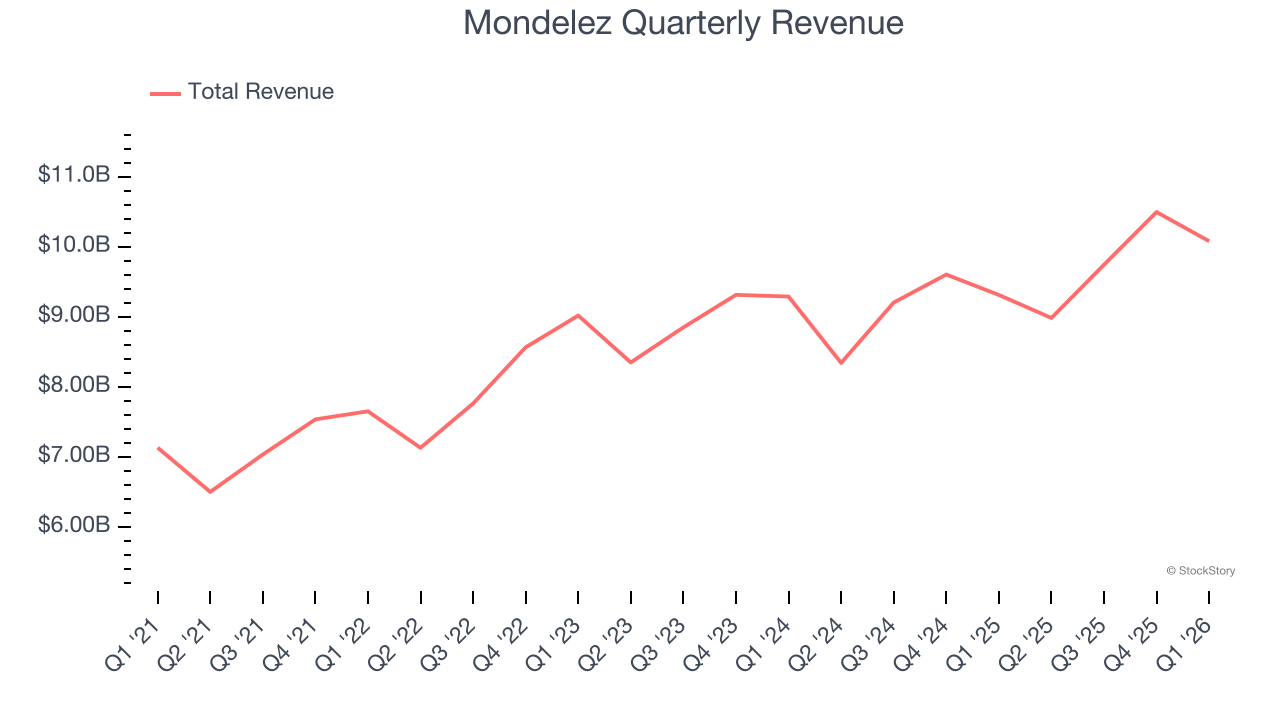

Packaged snacks company Mondelez (NASDAQ: MDLZ) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 8.2% year on year to $10.08 billion. Its non-GAAP profit of $0.67 per share was 10.2% above analysts’ consensus estimates.

Is now the time to buy Mondelez? Find out by accessing our full research report, it’s free.

Mondelez (MDLZ) Q1 CY2026 Highlights:

- Revenue: $10.08 billion vs analyst estimates of $9.79 billion (8.2% year-on-year growth, 3% beat)

- Adjusted EPS: $0.67 vs analyst estimates of $0.61 (10.2% beat)

- Adjusted EBITDA: $1.15 billion vs analyst estimates of $1.46 billion (11.4% margin, 21% miss)

- Operating Margin: 8%, in line with the same quarter last year

- Free Cash Flow Margin: 1.5%, down from 8.8% in the same quarter last year

- Organic Revenue rose 3% year on year (beat)

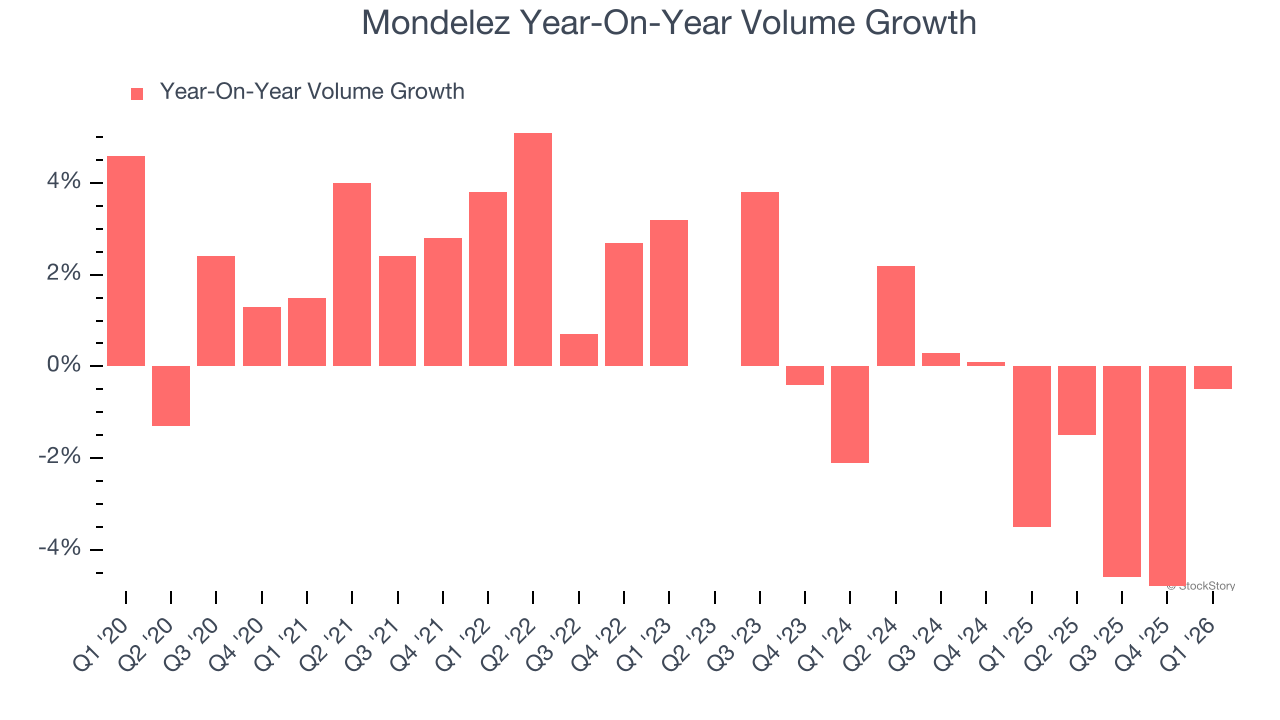

- Sales Volumes were flat year on year (-3.5% in the same quarter last year)

- Market Capitalization: $73.7 billion

“We posted solid first quarter results led by strong top-line growth in our Emerging Markets while Developed Market growth showed signs of improvement. These results reflect strong execution of our consumer-centric strategy supported by increased investments behind our brands and growth platforms despite ongoing macro volatility,” said Dirk Van de Put, Chair and Chief Executive Officer.

Company Overview

Founded as Nabisco in 1903, Mondelez (NASDAQ: MDLZ) is a packaged snacks powerhouse best known for its Oreo, Cadbury, Toblerone, Ritz, and Trident brands.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $39.3 billion in revenue over the past 12 months, Mondelez is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because there are only so many big store chains to sell into, making it harder to find incremental growth. For Mondelez to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

As you can see below, Mondelez grew its sales at a mediocre 6.6% compounded annual growth rate over the last three years as consumers bought less of its products. We’ll explore what this means in the "Volume Growth" section.

This quarter, Mondelez reported year-on-year revenue growth of 8.2%, and its $10.08 billion of revenue exceeded Wall Street’s estimates by 3%.

Looking ahead, sell-side analysts expect revenue to grow 1.6% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and suggests its products will face some demand challenges.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

To analyze whether Mondelez generated its growth from changes in price or volume, we can compare its volume growth to its organic revenue growth, which excludes non-fundamental impacts on company financials like mergers and currency fluctuations.

Over the last two years, Mondelez’s average quarterly sales volumes have shrunk by 1.5%. This decrease isn’t ideal as the quantity demanded for consumer staples products is typically stable. Luckily, Mondelez was able to offset fewer customers purchasing its products by charging higher prices, enabling it to generate 4.2% average organic revenue growth. We hope the company can grow its volumes soon, however, as consistent price increases (on top of inflation) aren’t sustainable over the long term unless the business is really really special.

In Mondelez’s Q1 2026, year on year sales volumes were flat. This result was a well-appreciated turnaround from its historical levels, showing the company is heading in the right direction.

Key Takeaways from Mondelez’s Q1 Results

We enjoyed seeing Mondelez beat analysts’ organic revenue expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its adjusted operating income missed and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded up 1.6% to $59.50 immediately following the results.

So do we think Mondelez is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).