Ulta has followed the market’s trajectory closely. The stock is down 5.2% to $537.41 per share over the past six months while the S&P 500 has lost 2.3%. This might have investors contemplating their next move.

Following the pullback, is now a good time to buy ULTA? Find out in our full research report, it’s free.

Why Does Ulta Spark Debate?

Offering high-end prestige brands as well as lower-priced, mass-market ones, Ulta Beauty (NASDAQ: ULTA) is an American retailer that sells makeup, skincare, haircare, and fragrance products.

Two Positive Attributes:

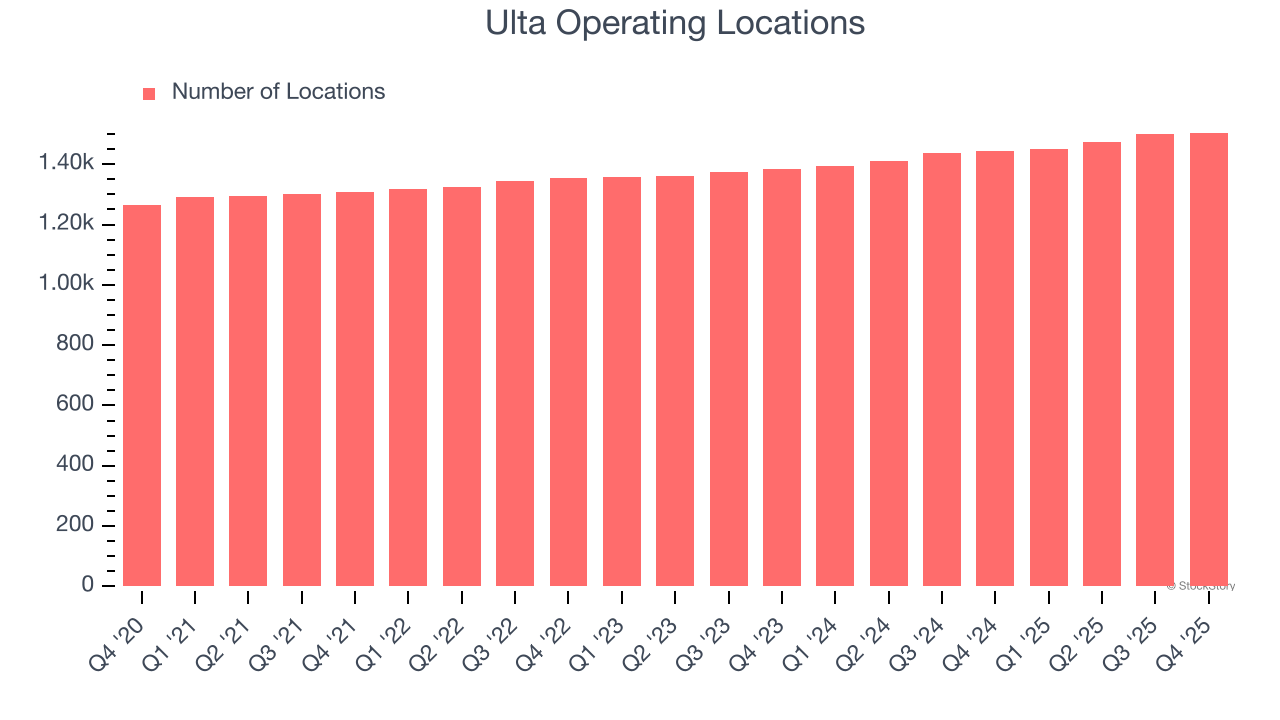

1. Store Growth Signals an Offensive Strategy

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Ulta operated 1,505 locations in the latest quarter. It has opened new stores at a rapid clip over the last two years, averaging 4% annual growth, much faster than the broader consumer retail sector. This gives it a chance to become a large, scaled business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

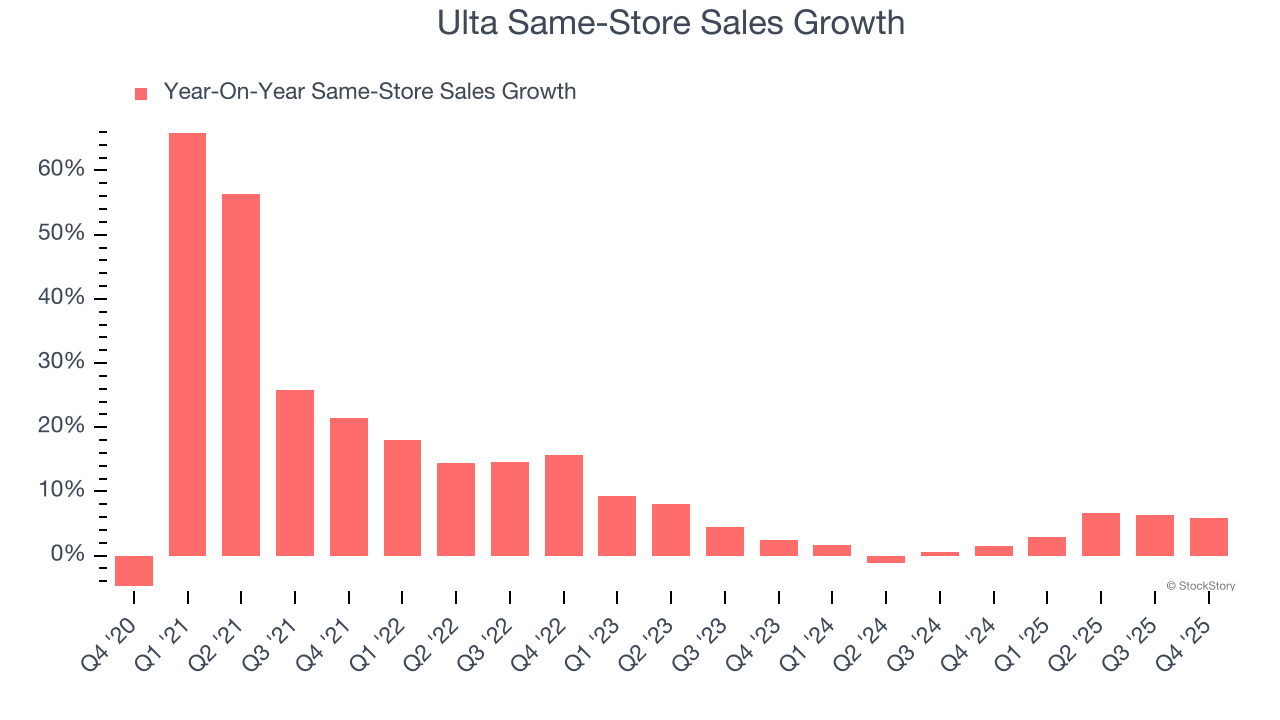

2. Solid Same-Store Sales Suggest Increasing Demand

Same-store sales show the change in sales for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

Ulta’s demand has been healthy for a retailer over the last two years. On average, the company has grown its same-store sales by a robust 3% per year.

One Reason to be Careful:

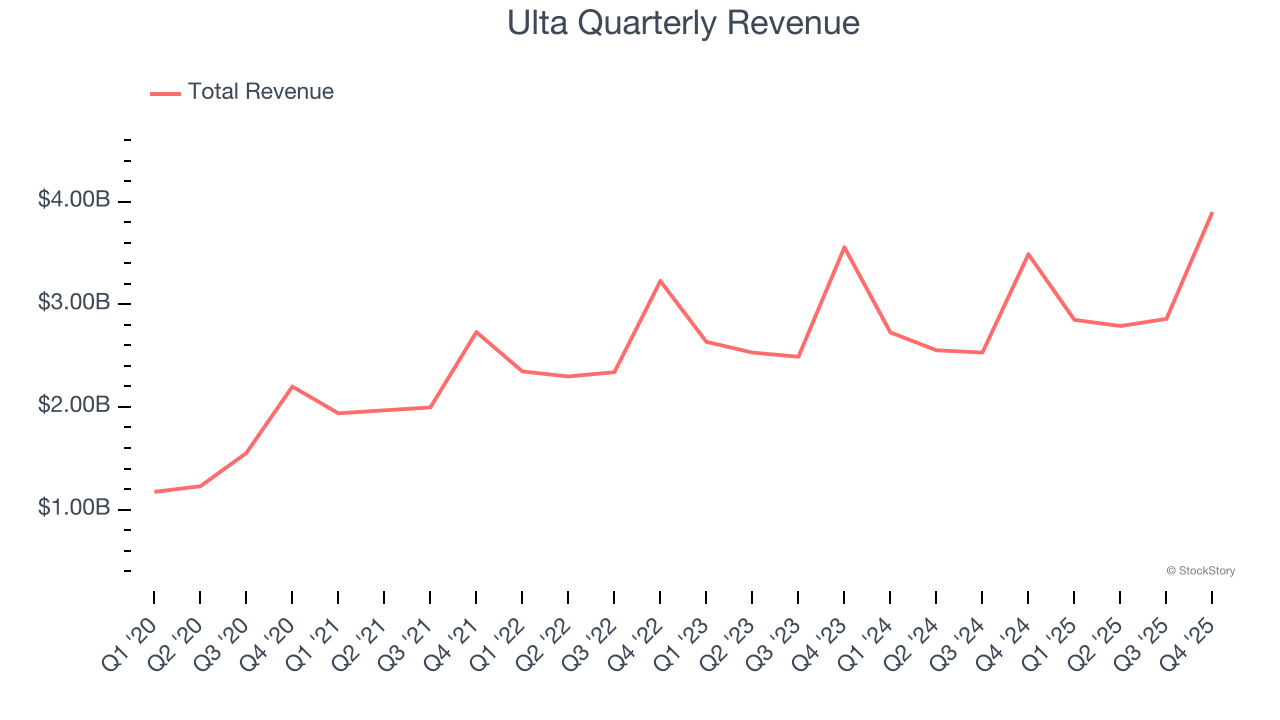

Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Ulta’s sales grew at a tepid 6.7% compounded annual growth rate over the last three years. This wasn’t a great result compared to the rest of the consumer retail sector, but there are still things to like about Ulta.

Final Judgment

Ulta’s merits more than compensate for its flaws. After the recent drawdown, the stock trades at 18.8× forward P/E (or $537.41 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Ulta

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.