Although the S&P 500 is down 1.8% over the past six months, Universal Health Services’s stock price has fallen further to $187.24, losing shareholders 7.1% of their capital. This may have investors wondering how to approach the situation.

Following the pullback, is now an opportune time to buy UHS? Find out in our full research report, it’s free.

Why Does Universal Health Services Spark Debate?

With a network spanning 39 states and three countries, Universal Health Services (NYSE: UHS) operates acute care hospitals and behavioral health facilities across the United States, United Kingdom, and Puerto Rico.

Two Things to Like:

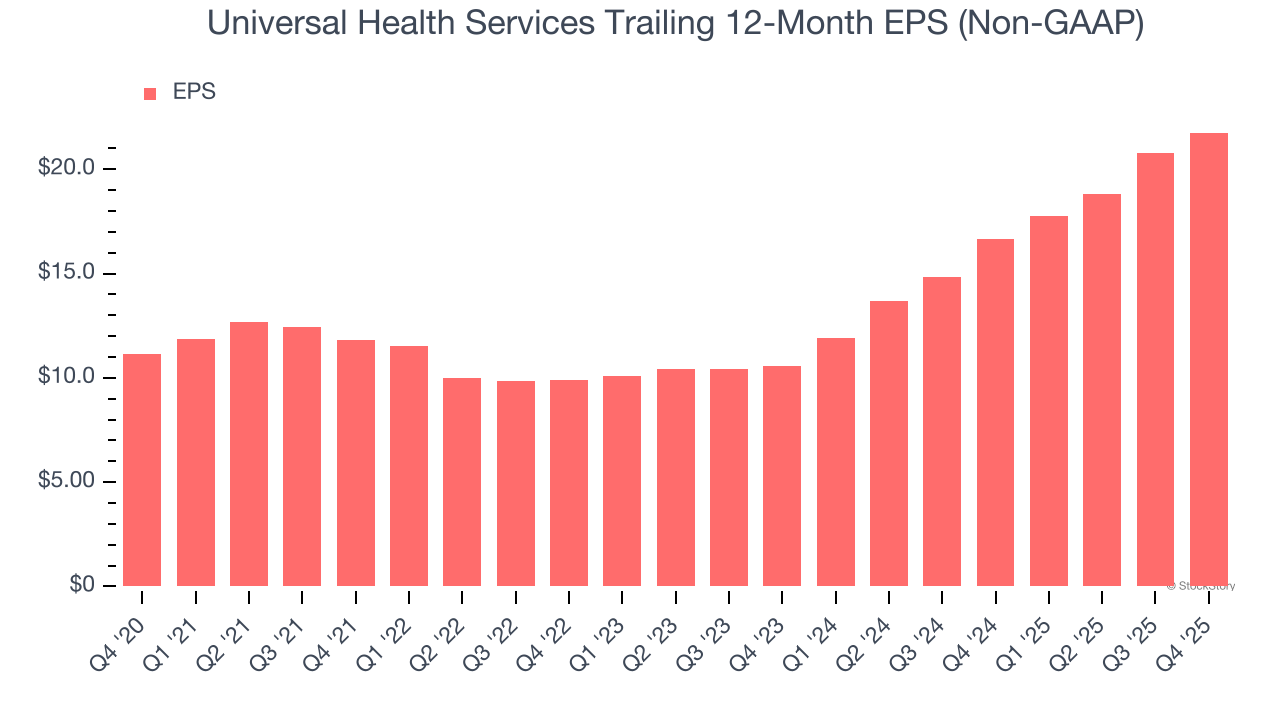

1. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Universal Health Services’s EPS grew at 14.3% compounded annual growth rate over the last five years, higher than its 8.5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

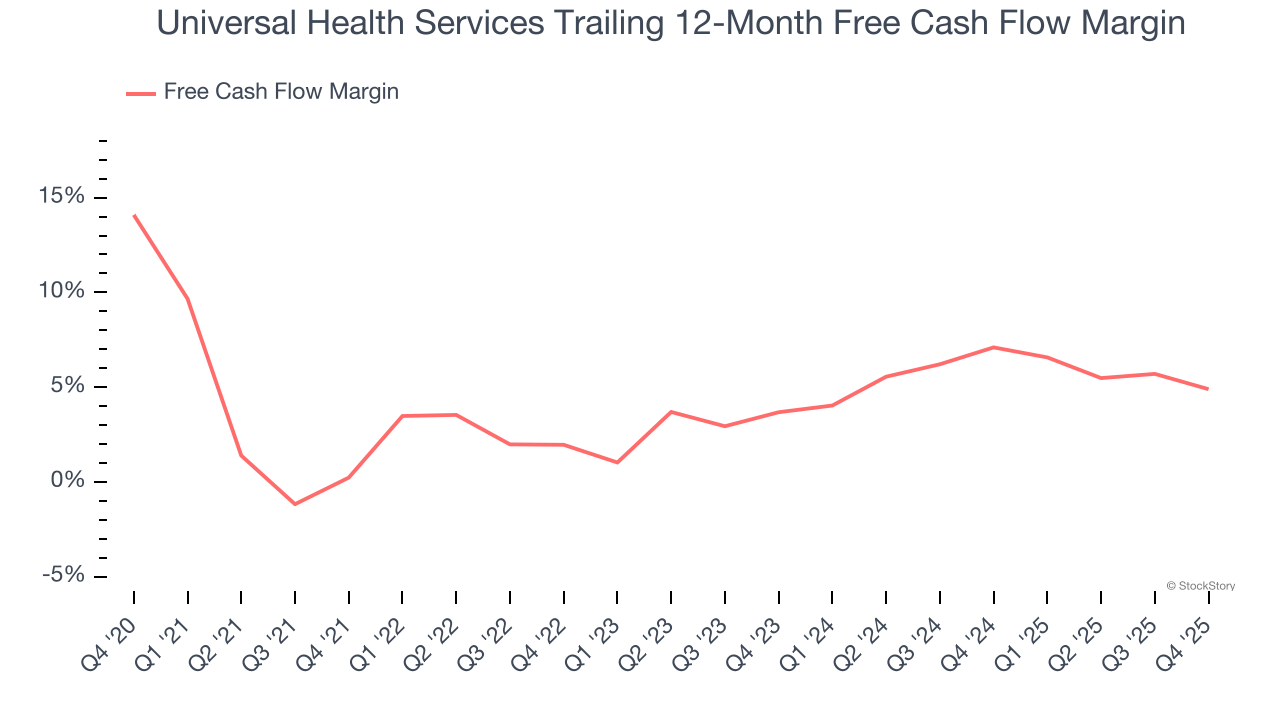

2. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Universal Health Services’s margin expanded by 4.7 percentage points over the last five years. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat. Universal Health Services’s free cash flow margin for the trailing 12 months was 4.9%.

One Reason to be Careful:

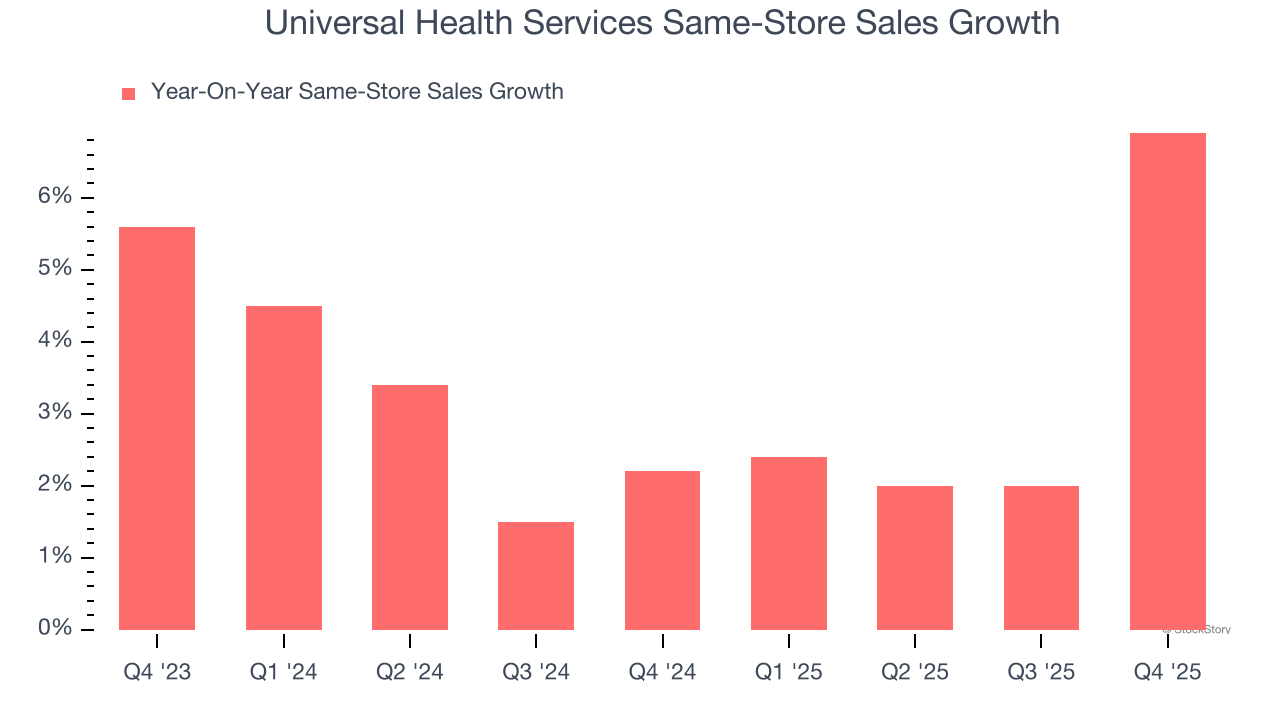

Same-Store Sales Falling Behind Peers

Investors interested in Hospital Chains companies should track same-store sales in addition to reported revenue. This metric measures the change in sales at brick-and-mortar locations that have existed for at least a year, giving visibility into Universal Health Services’s underlying demand characteristics.

Over the last two years, Universal Health Services’s same-store sales averaged 3.1% year-on-year growth. This performance slightly lagged the sector and suggests it might have to change its strategy or pricing, which can disrupt operations.

Final Judgment

Universal Health Services’s positive characteristics outweigh the negatives. After the recent drawdown, the stock trades at 7.7× forward P/E (or $187.24 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Universal Health Services

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.