Over the past six months, Universal Display’s stock price fell to $87.50. Shareholders have lost 19.5% of their capital, which is disappointing considering the S&P 500 has climbed by 13.2%. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy Universal Display, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Universal Display Not Exciting?

Even though the stock has become cheaper, we're cautious about Universal Display. Here are two reasons there are better opportunities than OLED and a stock we'd rather own.

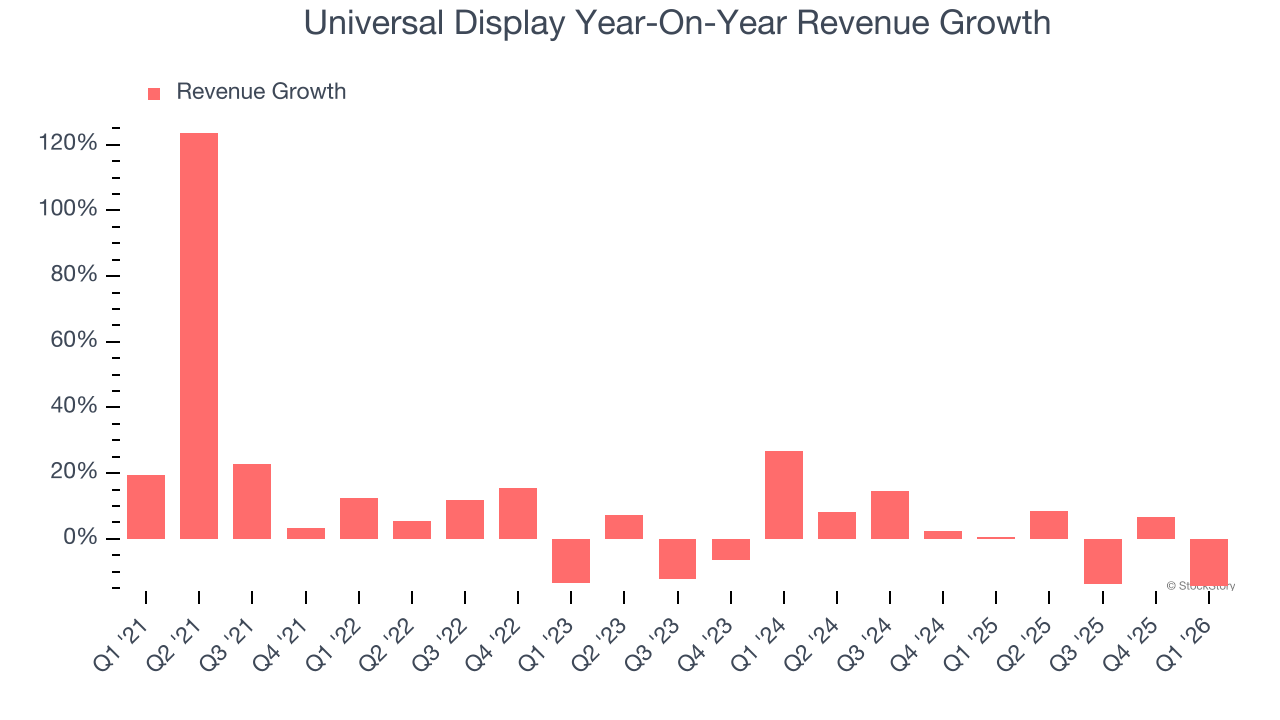

1. Lackluster Revenue Growth

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Universal Display’s recent performance shows its demand has slowed as its annualized revenue growth of 1.2% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Universal Display’s revenue to rise by 6.2%. While this projection suggests its newer products and services will catalyze better top-line performance, it is still below the sector average.

Final Judgment

Universal Display’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 19.3× forward P/E (or $87.50 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at the most entrenched endpoint security platform on the market.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month - FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.