Cosmetics company e.l.f. Beauty (NYSE: ELF) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 35.1% year on year to $449.3 million. On the other hand, the company’s full-year revenue guidance of $1.85 billion at the midpoint came in 0.7% below analysts’ estimates. Its non-GAAP profit of $0.32 per share was 12.2% above analysts’ consensus estimates.

Is now the time to buy e.l.f. Beauty? Find out by accessing our full research report, it’s free.

e.l.f. Beauty (ELF) Q1 CY2026 Highlights:

- Revenue: $449.3 million vs analyst estimates of $424.8 million (35.1% year-on-year growth, 5.8% beat)

- Adjusted EPS: $0.32 vs analyst estimates of $0.29 (12.2% beat)

- Adjusted EBITDA: $58.83 million vs analyst estimates of $49.85 million (13.1% margin, 18% beat)

- Adjusted EPS guidance for the upcoming financial year 2027 is $3.30 at the midpoint, missing analyst estimates by 8.6%

- EBITDA guidance for the upcoming financial year 2027 is $382 million at the midpoint, below analyst estimates of $383.9 million

- Operating Margin: -11.2%, down from 13.3% in the same quarter last year

- Free Cash Flow Margin: 22.4%, down from 37.6% in the same quarter last year

- Market Capitalization: $3.13 billion

“Fiscal 26 marked our 7th consecutive year of net sales and market share growth—a track record that reflects the strength of our team, strategy and portfolio of brands,” said Tarang Amin, e.l.f.

Company Overview

Short for "eyes, lips, face", e.l.f. Beauty (NYSE: ELF) is a developer of high-quality beauty products at accessible price points.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $1.64 billion in revenue over the past 12 months, e.l.f. Beauty is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, e.l.f. Beauty’s sales grew at an incredible 41.4% compounded annual growth rate over the last three years. This is an encouraging starting point for our analysis because it shows e.l.f. Beauty’s demand was higher than many consumer staples companies.

This quarter, e.l.f. Beauty reported wonderful year-on-year revenue growth of 35.1%, and its $449.3 million of revenue exceeded Wall Street’s estimates by 5.8%.

Looking ahead, sell-side analysts expect revenue to grow 14.3% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is commendable and implies the market is baking in success for its products.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

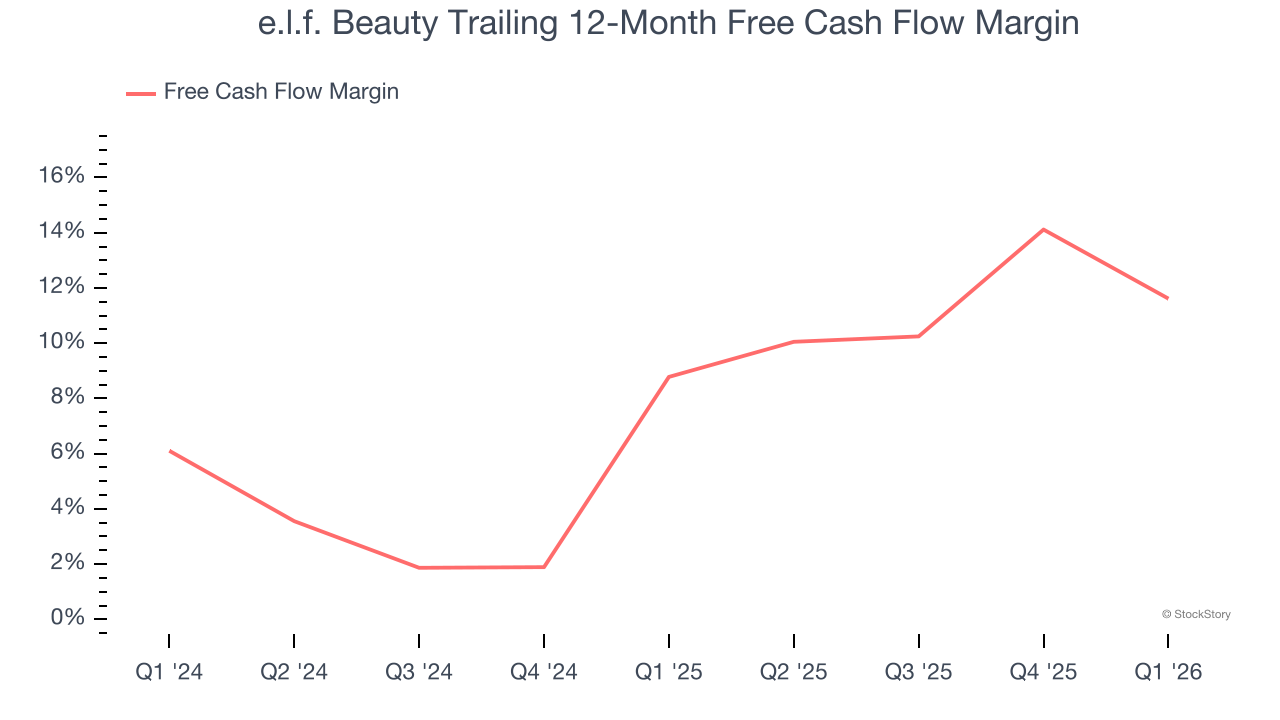

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

e.l.f. Beauty has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.4% over the last two years, quite impressive for a consumer staples business.

Taking a step back, we can see that e.l.f. Beauty’s margin expanded by 2.8 percentage points over the last year. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

e.l.f. Beauty’s free cash flow clocked in at $100.6 million in Q1, equivalent to a 22.4% margin. The company’s cash profitability regressed as it was 15.2 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, leading to short-term swings. Long-term trends are more important.

Key Takeaways from e.l.f. Beauty’s Q1 Results

We were impressed by how significantly e.l.f. Beauty blew past analysts’ EBITDA expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its adjusted operating income missed and its full-year revenue guidance fell slightly short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock traded up 5.1% to $53.44 immediately following the results.

Is e.l.f. Beauty an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).