Silgan Holdings currently trades at $37.99 per share and has shown little upside over the past six months, posting a small loss of 1.3%. The stock also fell short of the S&P 500’s 10.8% gain during that period.

Is there a buying opportunity in Silgan Holdings, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Silgan Holdings Will Underperform?

We're cautious about Silgan Holdings. Here are three reasons we avoid SLGN and a stock we'd rather own.

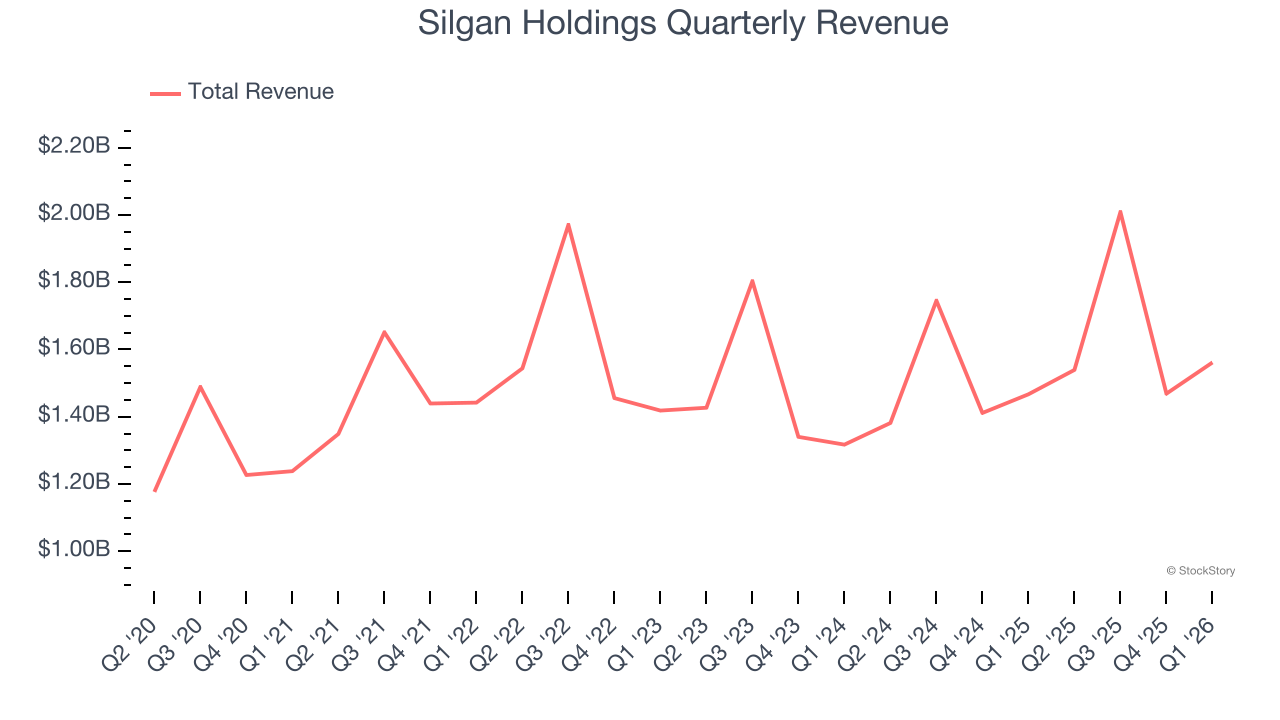

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Silgan Holdings grew its sales at a tepid 5.1% compounded annual growth rate. This was below our standard for the industrials sector.

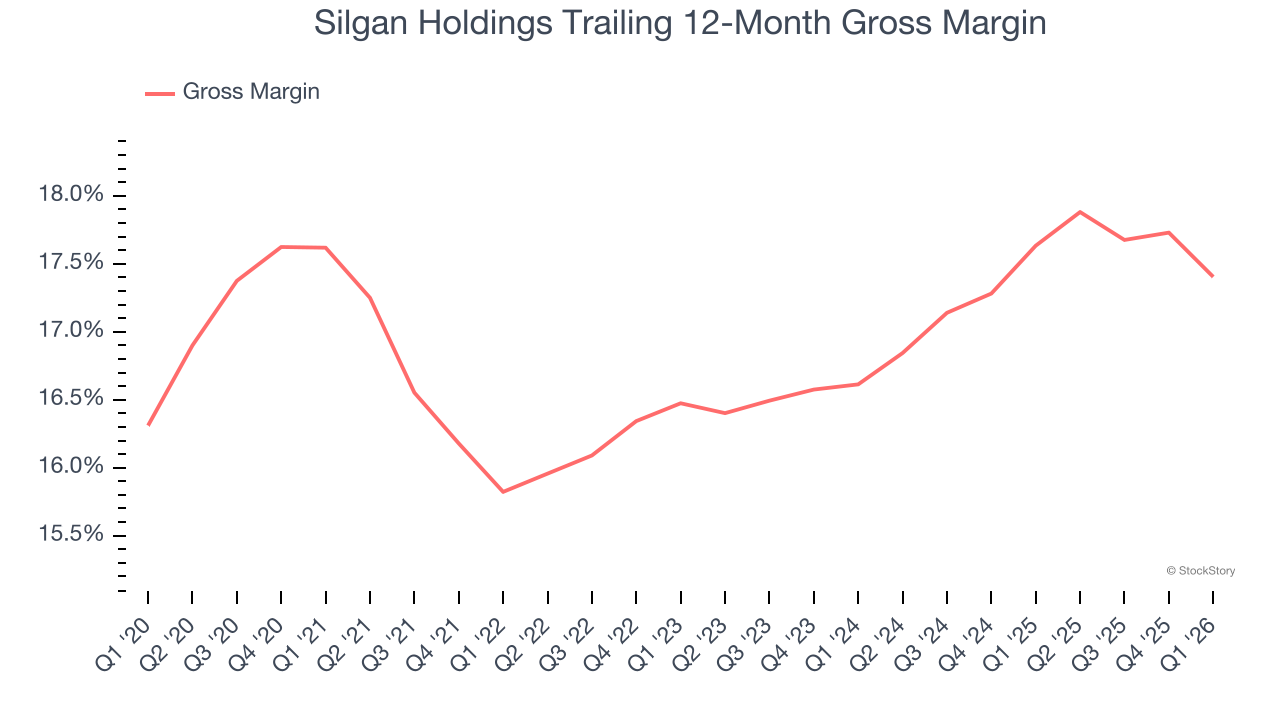

2. Low Gross Margin Reveals Weak Structural Profitability

Cost of sales for an industrials business is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics.

Silgan Holdings has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 16.8% gross margin over the last five years. That means Silgan Holdings paid its suppliers a lot of money ($83.20 for every $100 in revenue) to run its business.

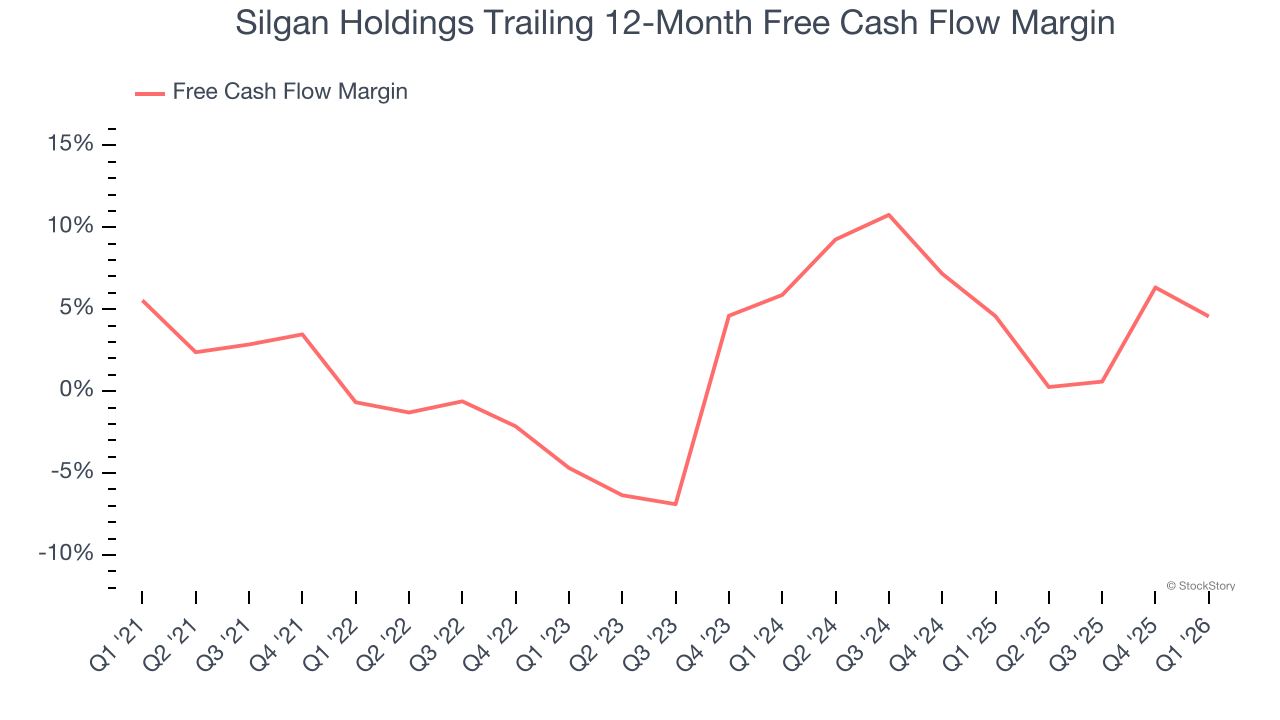

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Silgan Holdings has shown poor cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.9%, below what we’d expect for an industrials business.

Final Judgment

Silgan Holdings falls short of our quality standards. With its shares lagging the market recently, the stock trades at 9.9× forward P/E (or $37.99 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere. Let us point you toward a fast-growing restaurant franchise with an A+ ranch dressing sauce.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.