The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Fiserv (NASDAQ: FISV) and the rest of the payment processing stocks fared in Q1.

Payment processors facilitate transactions between merchants, consumers, and financial institutions. Growth comes from e-commerce expansion, declining cash usage globally, and value-added services beyond basic processing. Headwinds include margin pressure from merchant negotiating power, rapid technological change requiring investment, and emerging competition from technology companies entering the payments ecosystem.

The 4 payment processing stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 0.7%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 7.1% since the latest earnings results.

Fiserv (NASDAQ: FISV)

Powering over 1 billion accounts and processing more than 12,000 financial transactions per second globally, Fiserv (NASDAQ: FISV) provides payment processing and financial technology solutions that enable merchants, banks, and credit unions to accept payments and manage financial transactions.

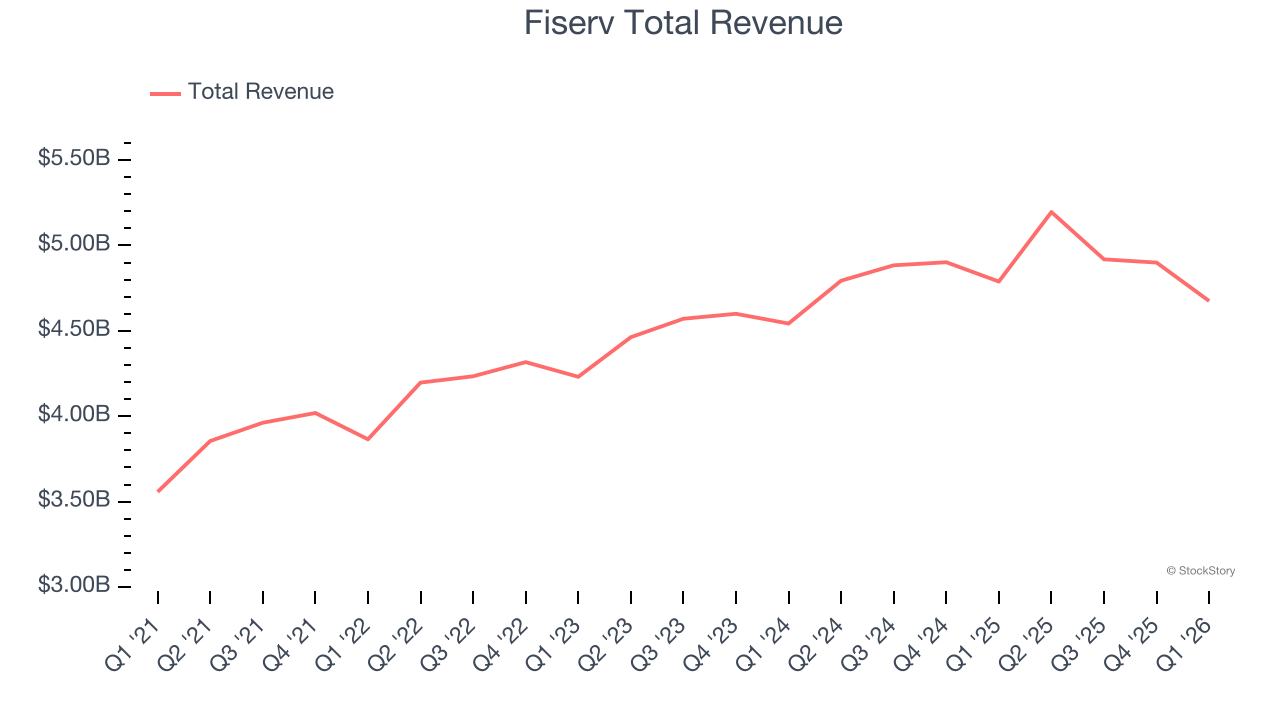

Fiserv reported revenues of $4.68 billion, down 2.4% year on year. This print fell short of analysts’ expectations by 1.2%, but it was still a satisfactory quarter for the company with a beat of analysts’ EPS estimates but a slight miss of analysts’ revenue estimates.

“During the first quarter, we remained in execution mode, delivering results in line with the expectations we shared in February,” said Mike Lyons, Chief Executive Officer of Fiserv.

Fiserv delivered the weakest performance against analyst estimates and slowest revenue growth of the whole group. Unsurprisingly, the stock is down 11.2% since reporting and currently trades at $55.75.

Is now the time to buy Fiserv? Access our full analysis of the earnings results here, it’s free.

Best Q1: Jack Henry (NASDAQ: JKHY)

Founded in 1976 by two entrepreneurs who saw the need for specialized banking software in the early days of financial computing, Jack Henry & Associates (NASDAQ: JKHY) provides technology solutions that help banks and credit unions innovate, differentiate, and compete while serving the evolving needs of their accountholders.

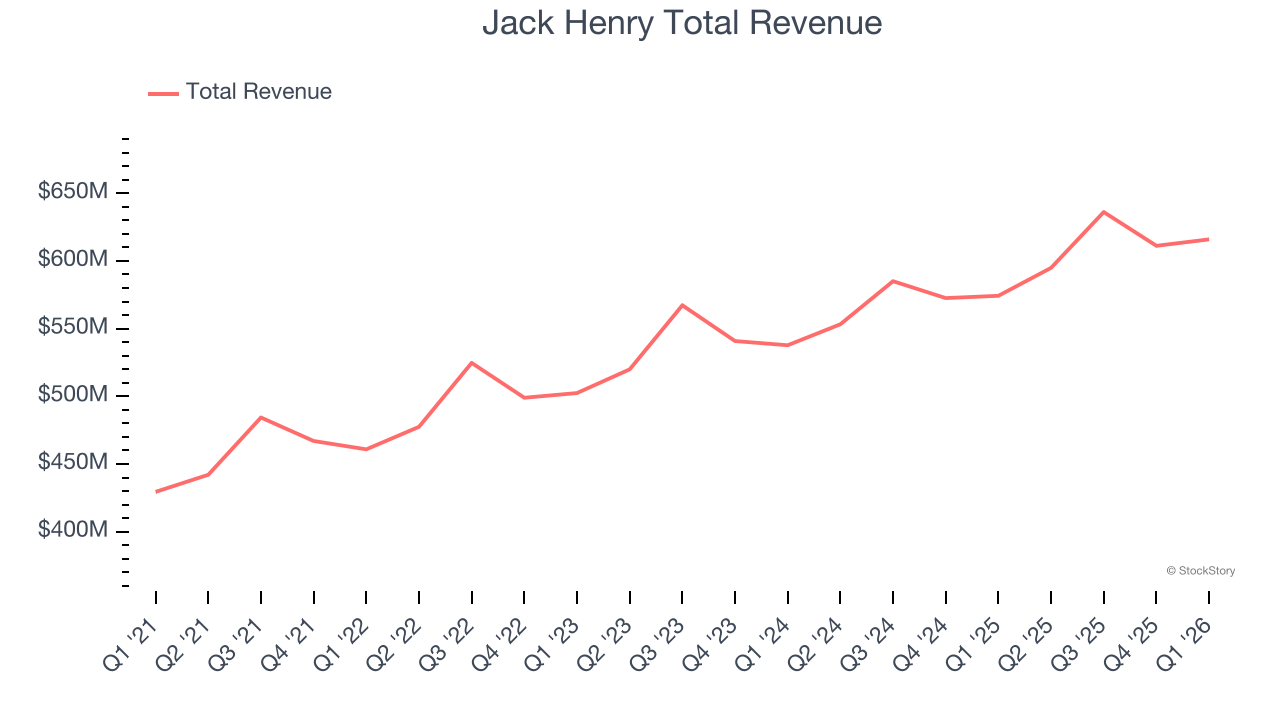

Jack Henry reported revenues of $615.9 million, up 7.3% year on year, outperforming analysts’ expectations by 1.3%. The business had a strong quarter with a beat of analysts’ EPS and EBITDA estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 6.5% since reporting. It currently trades at $139.60.

Is now the time to buy Jack Henry? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Shift4 (NYSE: FOUR)

Starting as a payment gateway provider in 1999 and now processing over $200 billion in annual payment volume, Shift4 Payments (NYSE: FOUR) provides integrated payment processing solutions and software that help businesses accept and manage transactions across in-store, online, and mobile channels.

Shift4 reported revenues of $1.12 billion, up 32.1% year on year, exceeding analysts’ expectations by 3.2%. Still, it was a slower quarter as it posted full-year revenue guidance missing analysts’ expectations significantly.

Shift4 delivered the weakest full-year guidance update in the group. Interestingly, the stock is up 1.7% since the results and currently trades at $43.63.

Read our full analysis of Shift4’s results here.

EVERTEC (NYSE: EVTC)

Operating one of Latin America's leading PIN debit networks called ATH, EVERTEC (NYSE: EVTC) is a payment transaction processor and financial technology provider that enables merchants and financial institutions across Latin America and the Caribbean to accept and process electronic payments.

EVERTEC reported revenues of $247.9 million, up 8.4% year on year. This result lagged analysts' expectations by 0.6%. Taking a step back, it was still a strong quarter as it put up full-year revenue guidance exceeding analysts’ expectations.

EVERTEC scored the highest full-year guidance raise among its peers. The stock is down 12.5% since reporting and currently trades at $24.65.

Read our full, actionable report on EVERTEC here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.