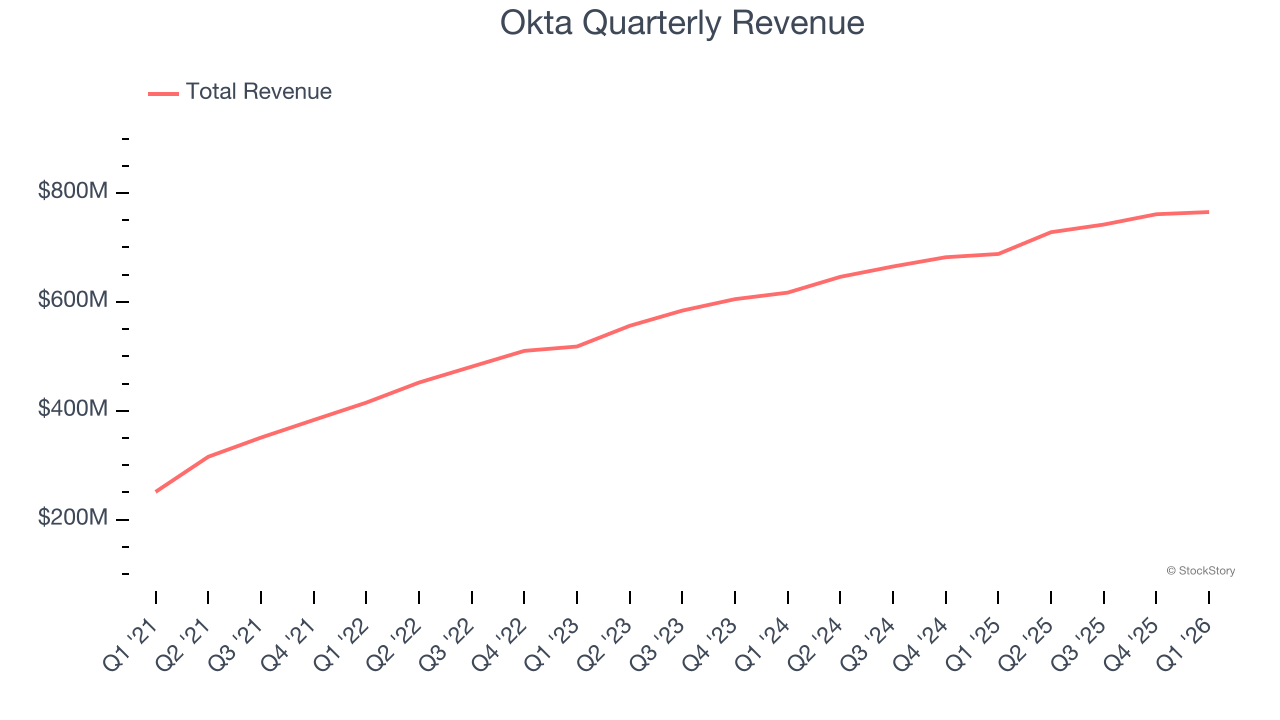

Identity management company Okta (NASDAQ: OKTA) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 11.2% year on year to $765 million. The company expects next quarter’s revenue to be around $792 million, close to analysts’ estimates. Its non-GAAP profit of $0.91 per share was 6.7% above analysts’ consensus estimates.

Is now the time to buy Okta? Find out by accessing our full research report, it’s free.

Okta (OKTA) Q1 CY2026 Highlights:

- Revenue: $765 million vs analyst estimates of $751.9 million (11.2% year-on-year growth, 1.7% beat)

- Adjusted EPS: $0.91 vs analyst estimates of $0.85 (6.7% beat)

- Adjusted Operating Income: $191 million vs analyst estimates of $179.5 million (25% margin, 6.4% beat)

- The company slightly lifted its revenue guidance for the full year to $3.20 billion at the midpoint from $3.18 billion

- Management raised its full-year Adjusted EPS guidance to $3.83 at the midpoint, a 1.3% increase

- Operating Margin: 7.3%, up from 5.7% in the same quarter last year

- Free Cash Flow Margin: 35.4%, up from 33.1% in the previous quarter

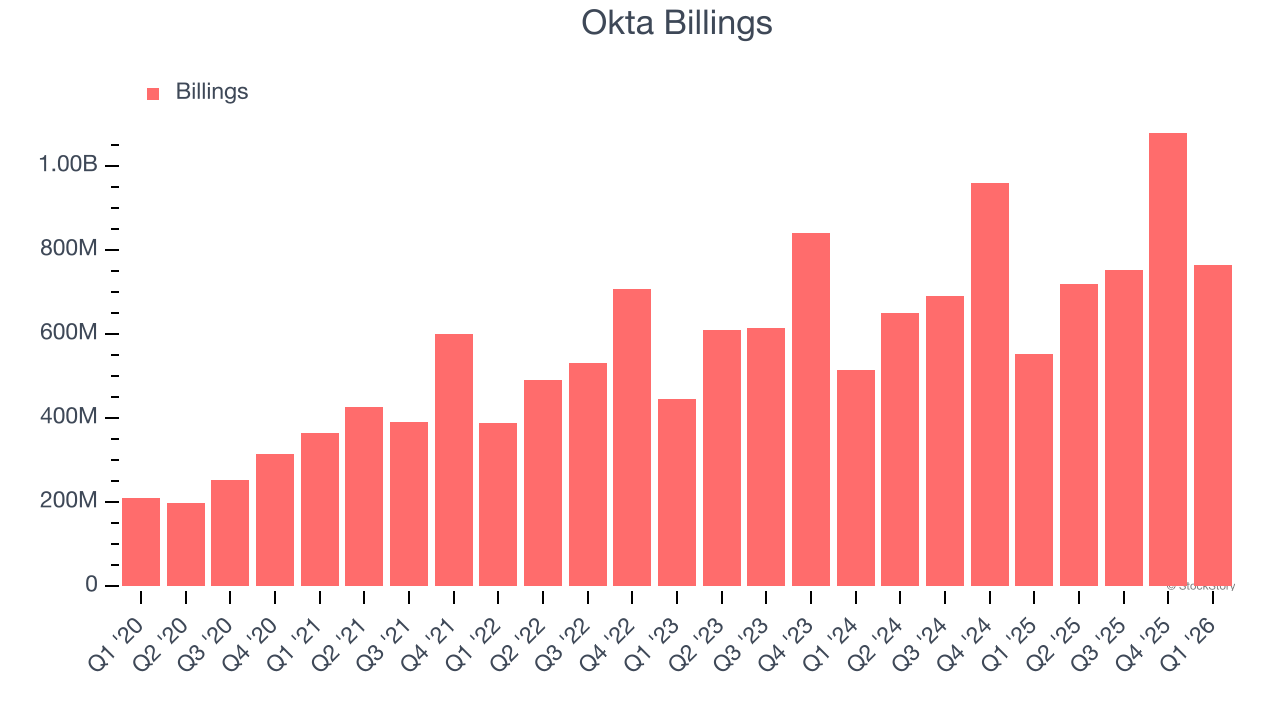

- Billings: $764.8 million at quarter end, up 38.6% year on year

- Market Capitalization: $15.69 billion

Company Overview

Named after the meteorological measurement for cloud cover, Okta (NASDAQ: OKTA) provides cloud-based identity management solutions that help organizations securely connect their employees, partners, and customers to the right applications and services.

Revenue Growth

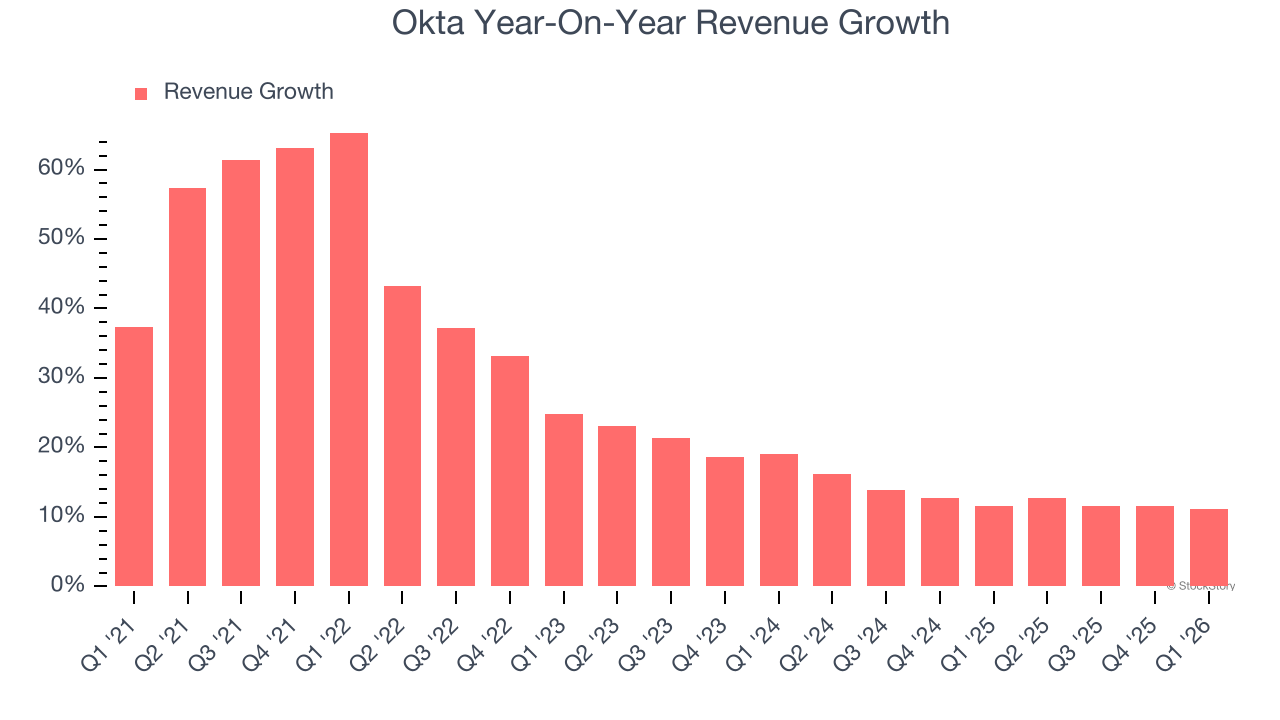

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Okta’s 27.1% annualized revenue growth over the last five years was impressive. Its growth beat the average software company and shows its offerings resonate with customers.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Okta’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 12.6% over the last two years was well below its five-year trend.

This quarter, Okta reported year-on-year revenue growth of 11.2%, and its $765 million of revenue exceeded Wall Street’s estimates by 1.7%. Company management is currently guiding for a 8.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.6% over the next 12 months, a deceleration versus the last two years. This projection doesn’t excite us and indicates its products and services will see some demand headwinds.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Okta’s billings punched in at $764.8 million in Q1, and over the last four quarters, its growth was solid as it averaged 17.7% year-on-year increases. This alternate topline metric grew faster than total sales, meaning the company collects cash upfront and then recognizes the revenue over the length of its contracts - a boost for its liquidity and future revenue prospects.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

It’s relatively expensive for Okta to acquire new customers as its CAC payback period checked in at 100.2 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a highly competitive market and must invest to stand out, even if the return on that investment is low.

Key Takeaways from Okta’s Q1 Results

We were impressed by how significantly Okta blew past analysts’ billings expectations this quarter. We were also glad its full-year EPS guidance slightly exceeded Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $95.37 immediately after reporting.

Sure, Okta had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).