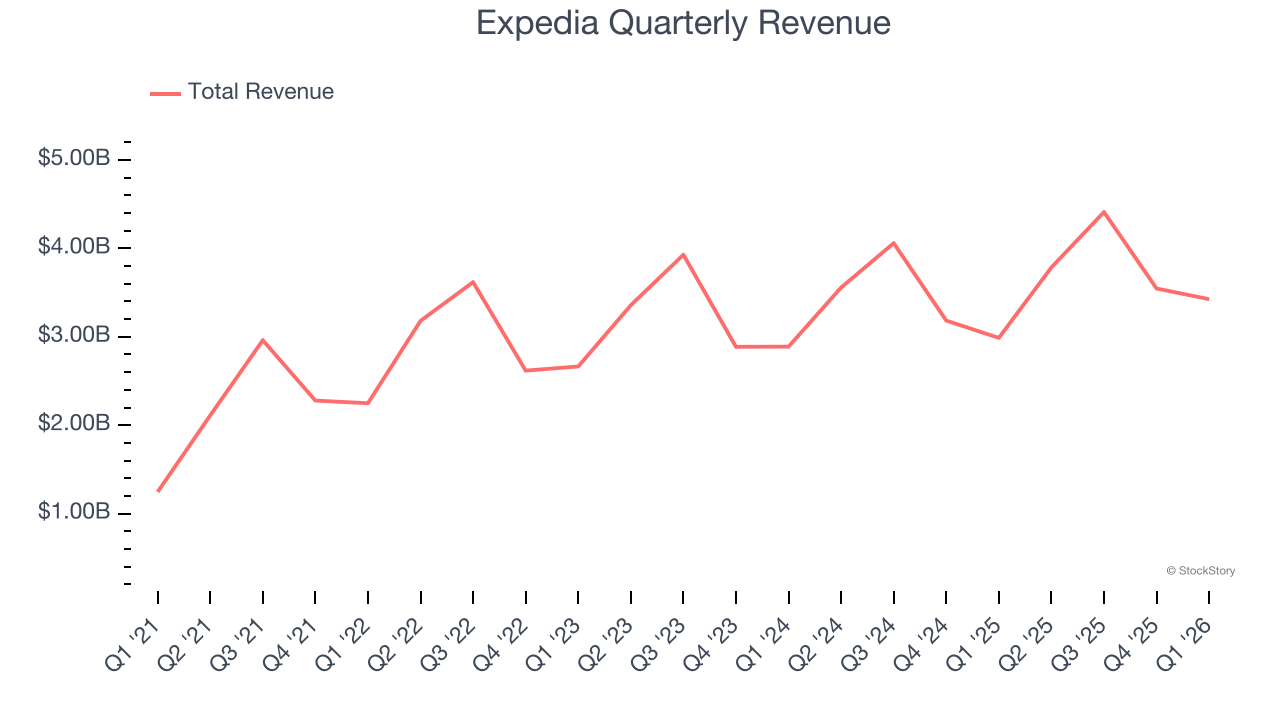

Online travel agency Expedia (NASDAQ: EXPE) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 14.7% year on year to $3.43 billion. Guidance for next quarter’s revenue was better than expected at $4.16 billion at the midpoint, 1% above analysts’ estimates. Its non-GAAP profit of $1.96 per share was 42.3% above analysts’ consensus estimates.

Is now the time to buy Expedia? Find out by accessing our full research report, it’s free.

Expedia (EXPE) Q1 CY2026 Highlights:

- Revenue: $3.43 billion vs analyst estimates of $3.35 billion (14.7% year-on-year growth, 2.2% beat)

- Adjusted EPS: $1.96 vs analyst estimates of $1.38 (42.3% beat)

- Adjusted EBITDA: $542 million vs analyst estimates of $451.7 million (15.8% margin, 20% beat)

- Revenue Guidance for Q2 CY2026 is $4.16 billion at the midpoint, above analyst estimates of $4.12 billion

- Operating Margin: 7.3%, up from -2.3% in the same quarter last year

- Free Cash Flow Margin: 109%, up from 3.4% in the previous quarter

- Room Nights Booked: 113.9 million, up 6.2 million year on year

- Market Capitalization: $29.6 billion

Company Overview

Originally founded as a part of Microsoft, Expedia (NASDAQ: EXPE) is one of the world’s leading online travel agencies.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Expedia’s 7.9% annualized revenue growth over the last three years was tepid. This wasn’t a great result compared to the rest of the consumer internet sector, but there are still things to like about Expedia.

This quarter, Expedia reported year-on-year revenue growth of 14.7%, and its $3.43 billion of revenue exceeded Wall Street’s estimates by 2.2%. Company management is currently guiding for a 10% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.5% over the next 12 months, similar to its three-year rate. This projection doesn't excite us and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Room Nights Booked

Booking Growth

As an online travel company, Expedia generates revenue growth by increasing both the number of stays (or experiences) booked and the commission charged on those bookings.

Over the last two years, Expedia’s room nights booked, a key performance metric for the company, increased by 8.7% annually to 113.9 million in the latest quarter. This growth rate is decent for a consumer internet business and indicates people enjoy using its offerings.

In Q1, Expedia added 6.2 million room nights booked, leading to 5.8% year-on-year growth. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t accelerating booking growth just yet.

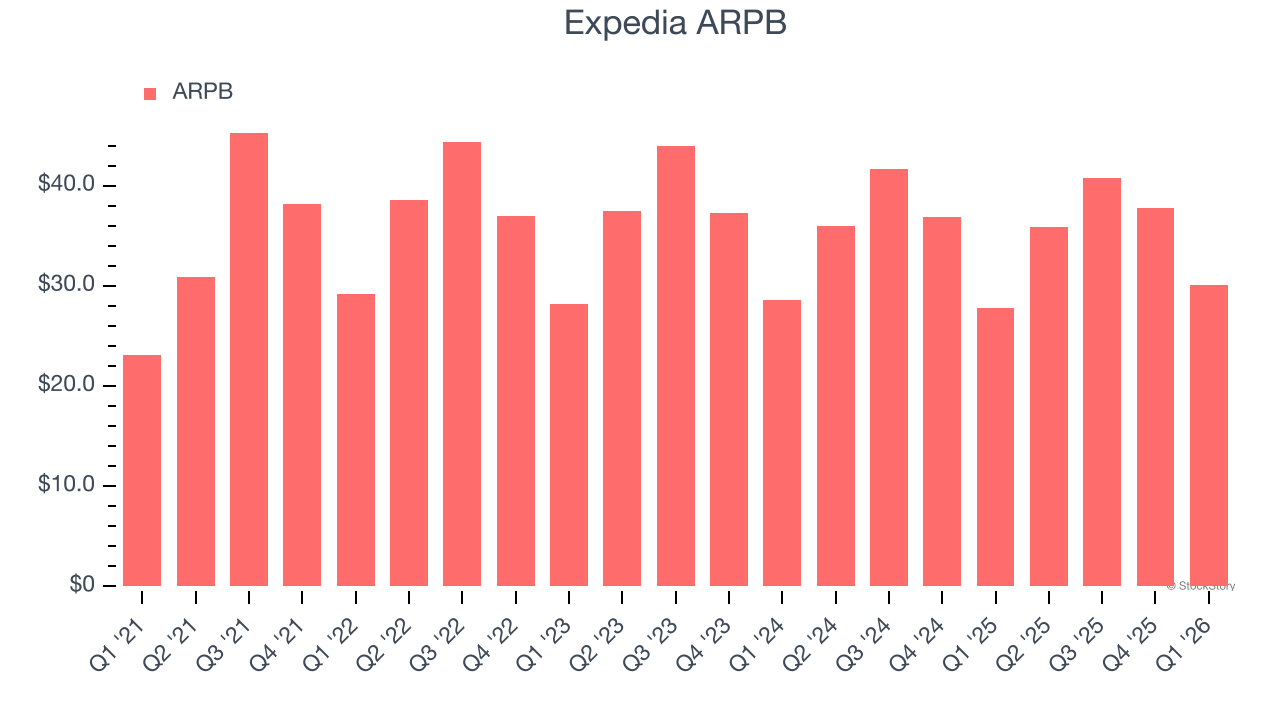

Revenue Per Booking

Average revenue per booking (ARPB) is a critical metric to track because it not only measures how much users book on its platform but also the commission that Expedia can charge.

Expedia’s ARPB has been roughly flat over the last two years. This isn’t great, but the increase in room nights booked is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Expedia tries boosting ARPB by taking a more aggressive approach to monetization, it’s unclear whether bookings can continue growing at the current pace.

This quarter, Expedia’s ARPB clocked in at $30.08. It grew by 8.4% year on year, faster than its room nights booked.

Key Takeaways from Expedia’s Q1 Results

We were impressed by how significantly Expedia blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. Investors were likely hoping for more, and shares traded down 9% to $229.93 immediately following the results.

So should you invest in Expedia right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).