Knight-Swift Transportation has had an impressive run over the past six months as its shares have beaten the S&P 500 by 29.7%. The stock now trades at $74.15, marking a 38.7% gain. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Knight-Swift Transportation, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Knight-Swift Transportation Will Underperform?

We’re happy investors have made money, but we don’t have much confidence in Knight-Swift Transportation. Here are three reasons you should be careful with KNX, plus one stock we’d rather own.

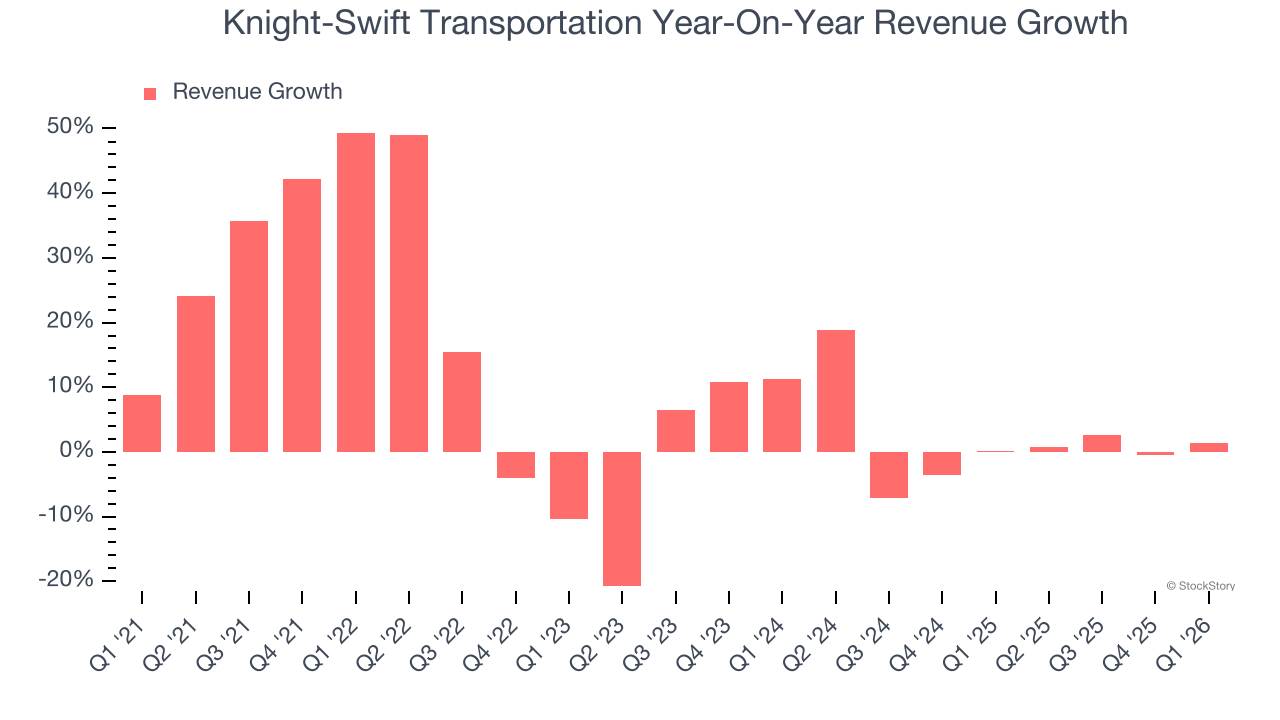

1. Lackluster Revenue Growth

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Knight-Swift Transportation’s recent performance shows its demand has slowed as its annualized revenue growth of 1.1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

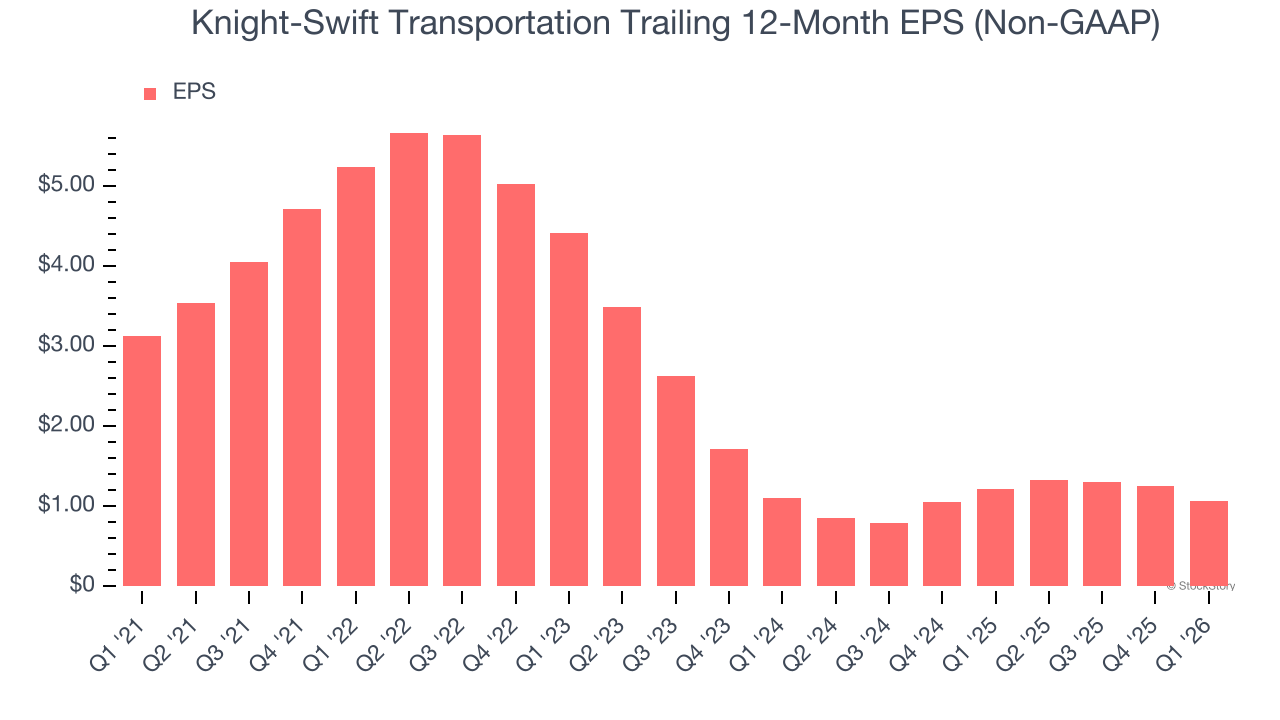

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Knight-Swift Transportation, its EPS declined by 19.3% annually over the last five years while its revenue grew by 9.5%. This tells us the company became less profitable on a per-share basis as it expanded.

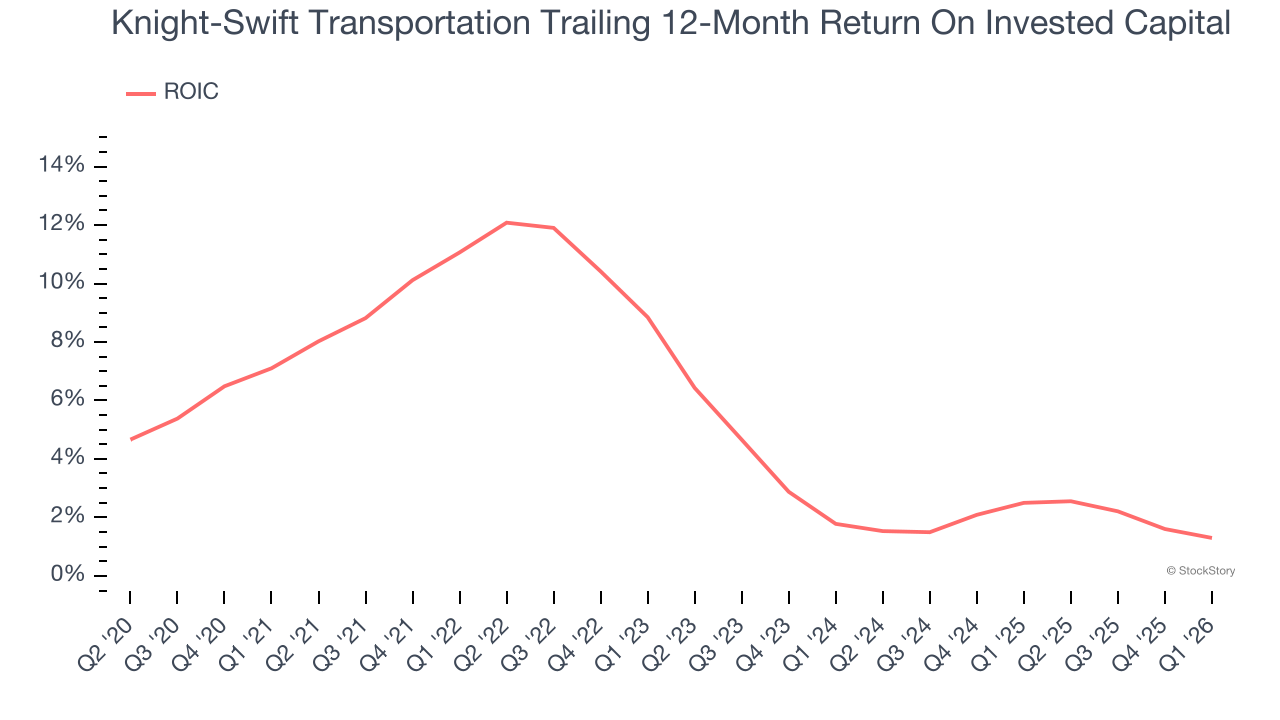

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

Unfortunately, Knight-Swift Transportation’s ROIC has decreased over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

Knight-Swift Transportation falls short of our quality standards. With its shares beating the market recently, the stock trades at 31.5× forward P/E (or $74.15 per share). This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.