Over the past six months, Axon’s shares (currently trading at $516.63) have posted a disappointing 9.7% loss, well below the S&P 500’s 6.1% gain. This might have investors contemplating their next move.

Following the drawdown, is now an opportune time to buy AXON? Find out in our full research report, it’s free.

Why Is AXON a Good Business?

Providing body cameras and tasers for first responders, AXON (NASDAQ: AXON) develops technology solutions and weapons products for military, law enforcement, and civilians.

1. ARR Surges as Recurring Revenue Flows In

In addition to reported revenue, ARR (annual recurring revenue) is a useful data point for analyzing Law Enforcement Suppliers companies. This metric shows how much Axon expects to collect from its existing customer base in the next 12 months, giving visibility into its future revenue streams.

Axon’s ARR punched in at $1.49 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 37.6%. This performance was fantastic and shows that customers are willing to take multi-year bets on the company’s product offerings. Its growth also makes Axon a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

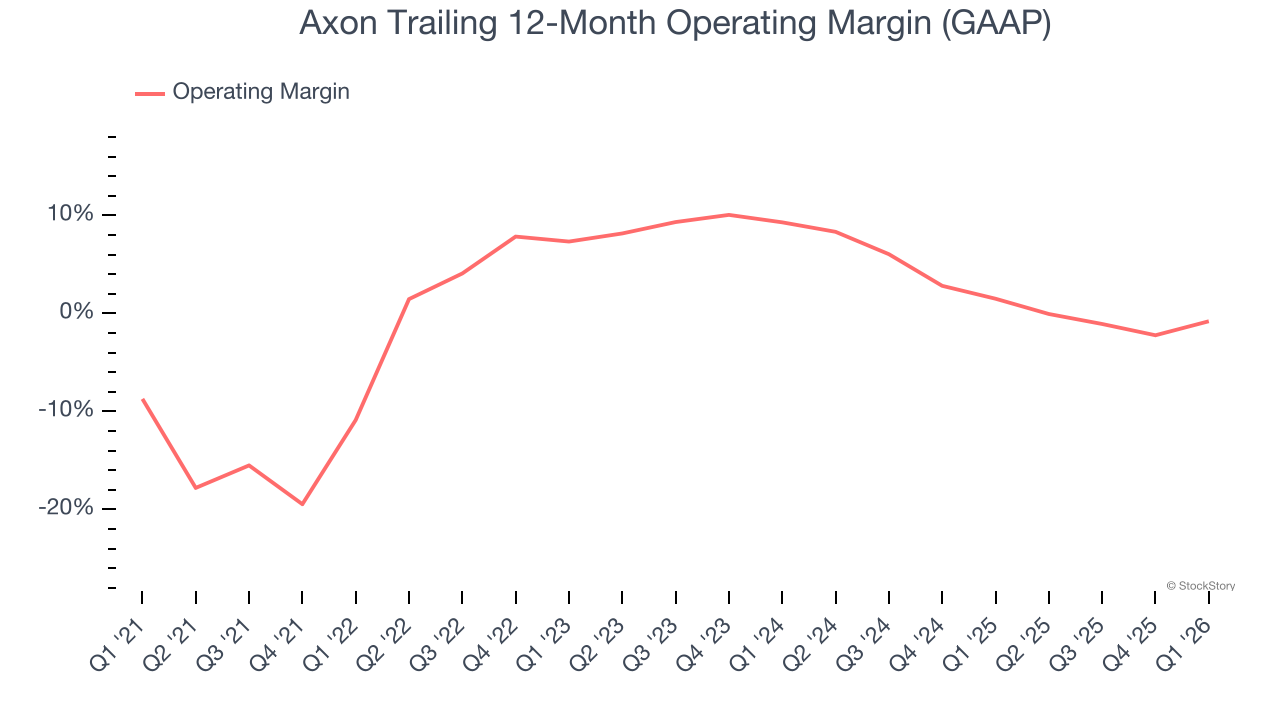

2. Operating Margin Rising, Profits Up

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Axon’s operating margin rose by 10.1 percentage points over the last five years, as its sales growth gave it immense operating leverage. Its operating margin for the trailing 12 months was breakeven.

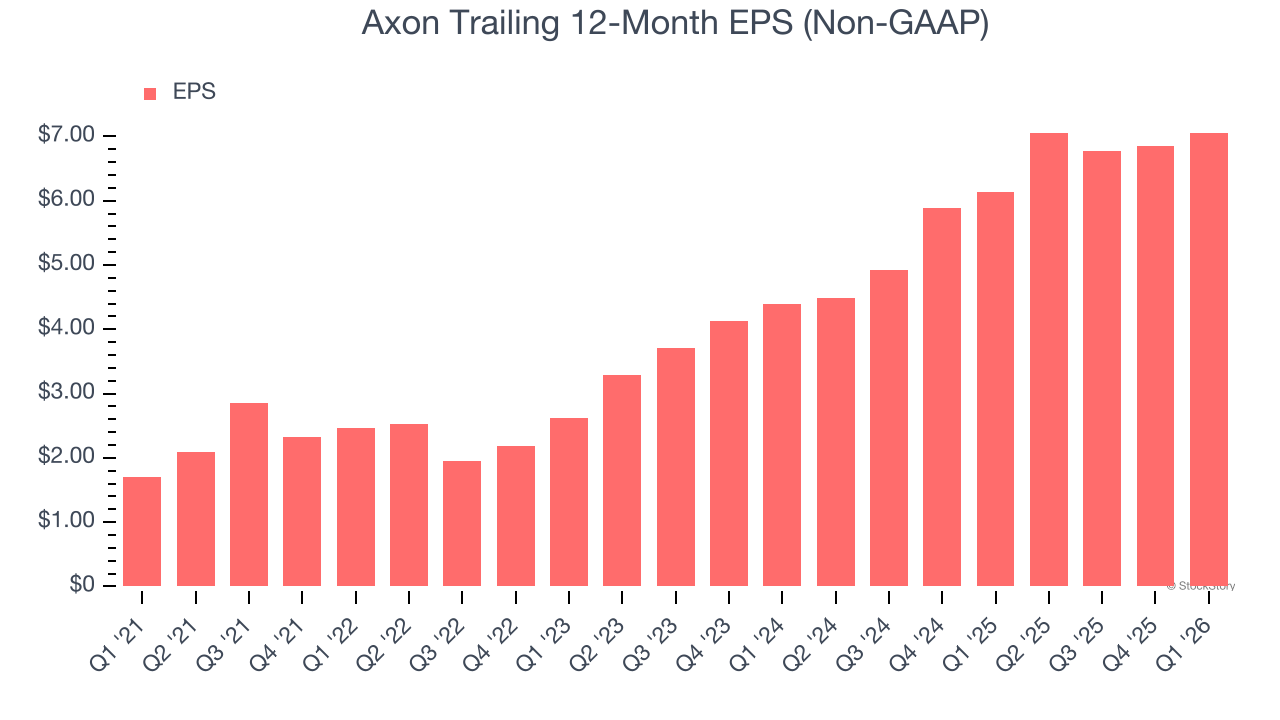

3. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Axon’s astounding 32.9% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Final Judgment

These are just a few reasons why we’re bullish on Axon. After the recent drawdown, the stock trades at 55.6× forward P/E (or $516.63 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Axon

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.