Anthropic, the company behind the Claude family of models, is stepping into a more critical role in the artificial intelligence (AI) race – one that goes beyond building intelligence to securing it. Its latest initiative, Project Glasswing, is a cybersecurity-focused effort powered by its most advanced model, Claude Mythos Preview, built to detect and even exploit software vulnerabilities at a level that rivals top human experts. The goal is to use AI offensively to strengthen defenses before bad actors can catch up.

Glasswing is not a solo play. It brings together a deep bench of partners, including Microsoft Corporation (MSFT), Broadcom (AVGO), and NVIDIA Corporation (NVDA), alongside other cybersecurity leaders and tech giants. The model has already uncovered thousands of high-severity flaws across major systems, highlighting both the risks and urgency behind this push. Anthropic is committing up to $100 million in credits, with access limited to select participants through platforms like cloud and API integrations.

Wedbush believes this signals a major shift. Cybersecurity, currently about 5% of IT budgets, could double as AI-driven threats rise, making it the enforcement layer of the AI era. That also means companies involved in Project Glasswing stand to benefit directly as demand for AI-driven security infrastructure scales up.

For investors looking to tap into Project Glasswing, MSFT, AVGO, and NVDA could be top-rated stocks to buy now.

Stock #1: Microsoft

A name almost everyone recognizes, Microsoft has become the backbone of modern digital life. What started as a software company has evolved into a tech giant, boasting a market capitalization of $2.75 trillion. Windows still powers much of the world’s PCs, but today Microsoft goes far beyond that – spanning Azure cloud, Microsoft 365, enterprise tools, and gaming. Over time, it has shifted from selling software to building subscription and AI-driven ecosystems.

Microsoft’s journey over the years has been built on steady growth. Over the years, its chart has moved in a fairly consistent upward direction, driven by its strong grip on cloud through Azure and its growing push into AI. That steady climb made it a core name in most tech portfolios.

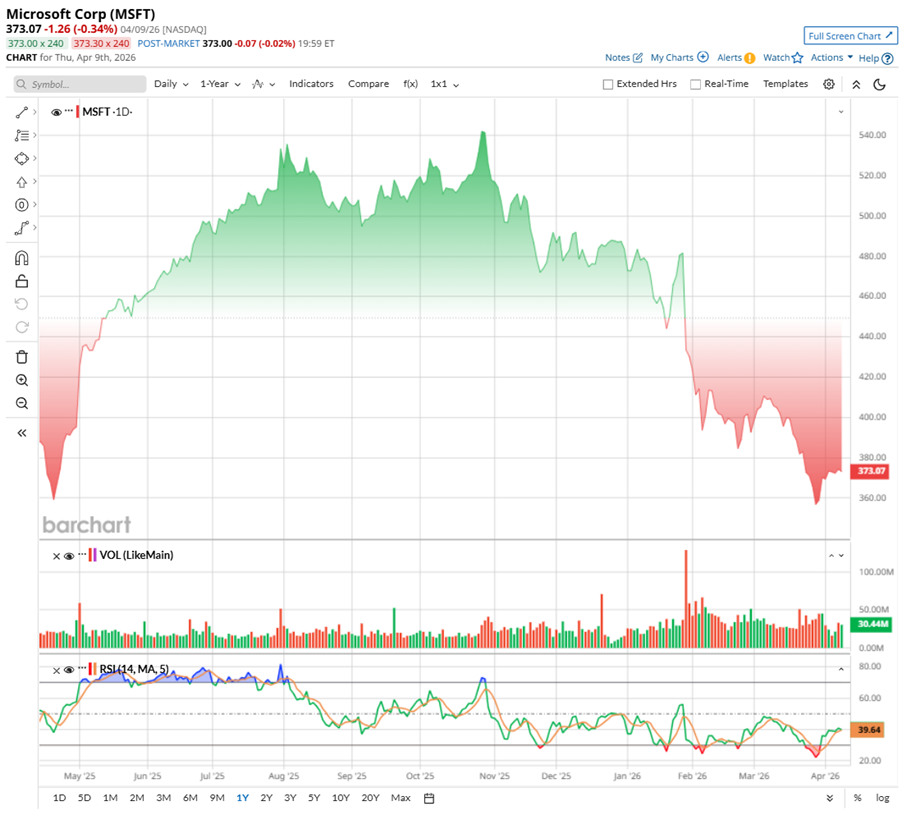

But the recent stretch tells a different story. The stock is down about 2.75% over the past 52 weeks, with a sharper drop of nearly 27.42% in the last six months. In 2026 alone, shares have fallen roughly 23.31% year-to-date (YTD. In fact, on March 30, MSFT was hovering near its 52-week low.

Concerns around heavy AI spending, rising competition, and a more cautious near-term outlook have weighed on sentiment. After its January earnings, the stock even saw a sharp 10% one-day fall – its steepest since 2020 – and now sits near a 10-month low.

Technically, rising volumes suggest investors are actively repositioning, while the 14-day RSI has climbed from oversold levels to 38.82, hinting that selling pressure may be starting to ease.

Valuation-wise, Microsoft is not exactly cheap. MSFT is priced at around 22.67 times forward adjusted earnings and 8.4 times forward sales, a premium to the broader tech sector averages. But compared to its own history, it is actually a bit more reasonable, reflecting quality rather than overpricing.

On top of that, Microsoft has been steady with shareholder returns, growing its dividend since 2003. It now offers about $3.64 per-share dividend annually with a comfortable payout ratio that supports future increases.

Microsoft released its Q2 earnings report for fiscal 2026 in January, generating revenue growth of 17% year-over-year (YOY), with the top line coming in at $81.3 billion. Non-GAAP EPS climbed 24% annually to $4.14. Both exceeded Wall Street’s projections. Growth was driven by strength in Azure, productivity tools, and expanding AI services.

One standout was Microsoft’s investment in OpenAI, which delivered a $7.6 billion gain, flipping from a loss last year. Still, management kept the focus on core operations. Margins stayed solid, with the operating margin at 47%, even as the company continued heavy AI spending.

Cloud revenue crossed $50 billion in a quarter for the first time, up 26% YOY, while commercial bookings rose 23%. Remaining performance obligations surged to $625 billion, showing strong future demand. Yet, despite all this, the stock slipped as investors grew cautious about rising AI capex, which hit nearly $30 billion.

From a financial standpoint, Microsoft remains on a strong footing, with a hefty cash pile, manageable debt, robust cash flow generation, and billions returned to shareholders through dividends and buybacks.

Microsoft is all set to publish its fiscal 2026 Q3 financial results after market close on Wednesday, Apr. 29. The management estimates Q3 revenue between $80.65 billion and $81.75 billion, implying mid-teens growth. Azure is expected to remain a key driver, with growth projected to accelerate to around 37% to 38%, even as demand continues to run ahead of available capacity.

In the near term, margins may come under slight pressure as Microsoft continues investing heavily in AI infrastructure. However, management expects margins to improve over the full year as spending stabilizes and scale benefits kick in.

Meanwhile, Wall Street analysts are equally bullish on Microsoft. EPS is expected to be about $4.04 per-share profit, up 16.8% YOY in Q3, while revenue is projected to be around $81.4 billion, signaling that growth across cloud and AI remains steady.

Looking further ahead to fiscal 2026, confidence builds further. EPS is estimated at $16.46 for the year, marking roughly 20.7% annual growth, and another 13.9% jump annually to $18.74 in fiscal 2027. That kind of steady expansion keeps the long-term story intact.

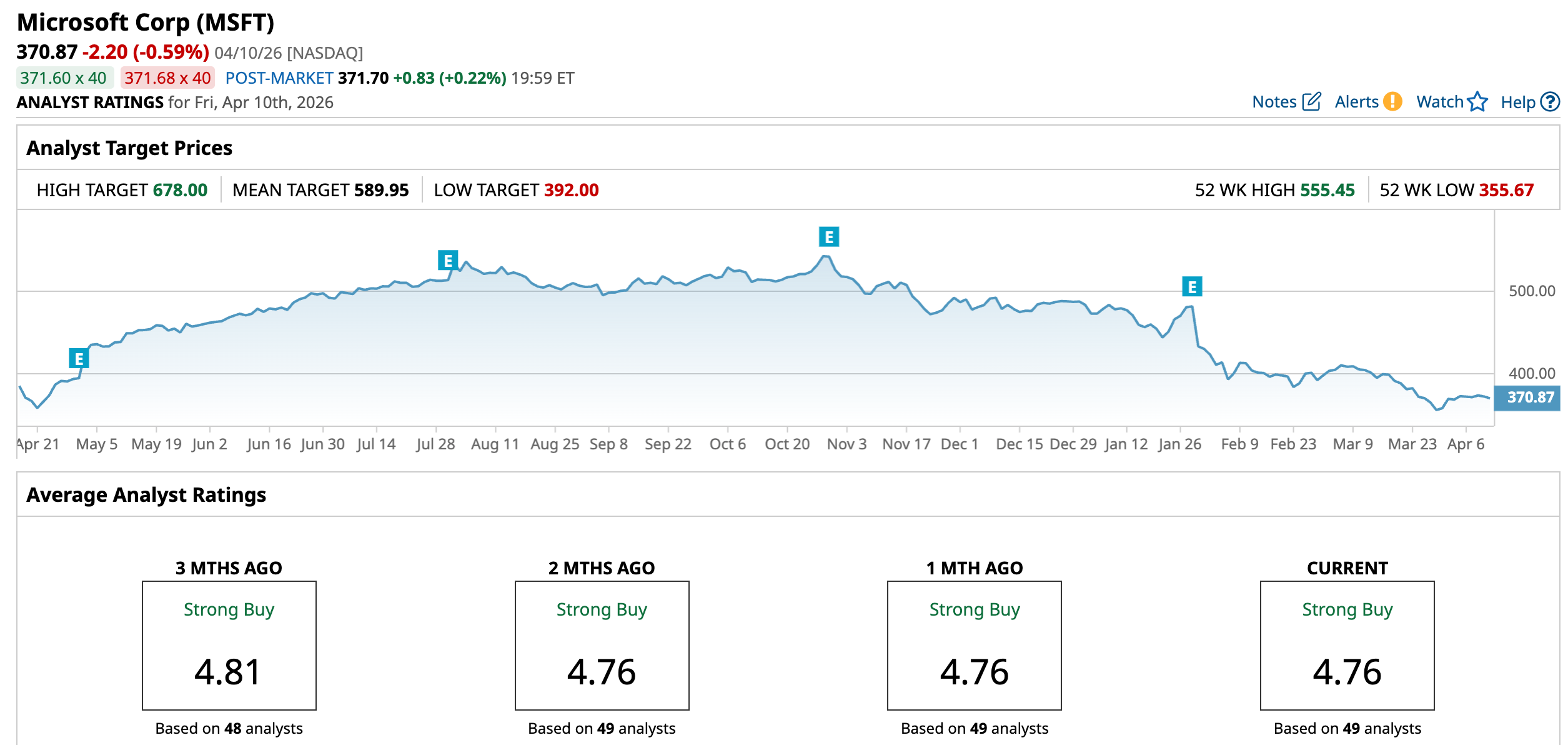

Overall, analysts are upbeat on MSFT, with a “Strong Buy” consensus. Of the 49 analysts tracking the tech stock, 41 have a “Strong Buy,” four advise a “Moderate Buy,” and the remaining four are on the sidelines with a “Hold” rating.

MSFT has an average price target of $589.95, implying roughly 59% upside potential from current levels, implying the momentum still has room to build. On the bullish end, the Street-high target of $678 points to even sharper gains of 82.8%, suggesting belief in Microsoft’s durable AI and cloud momentum.

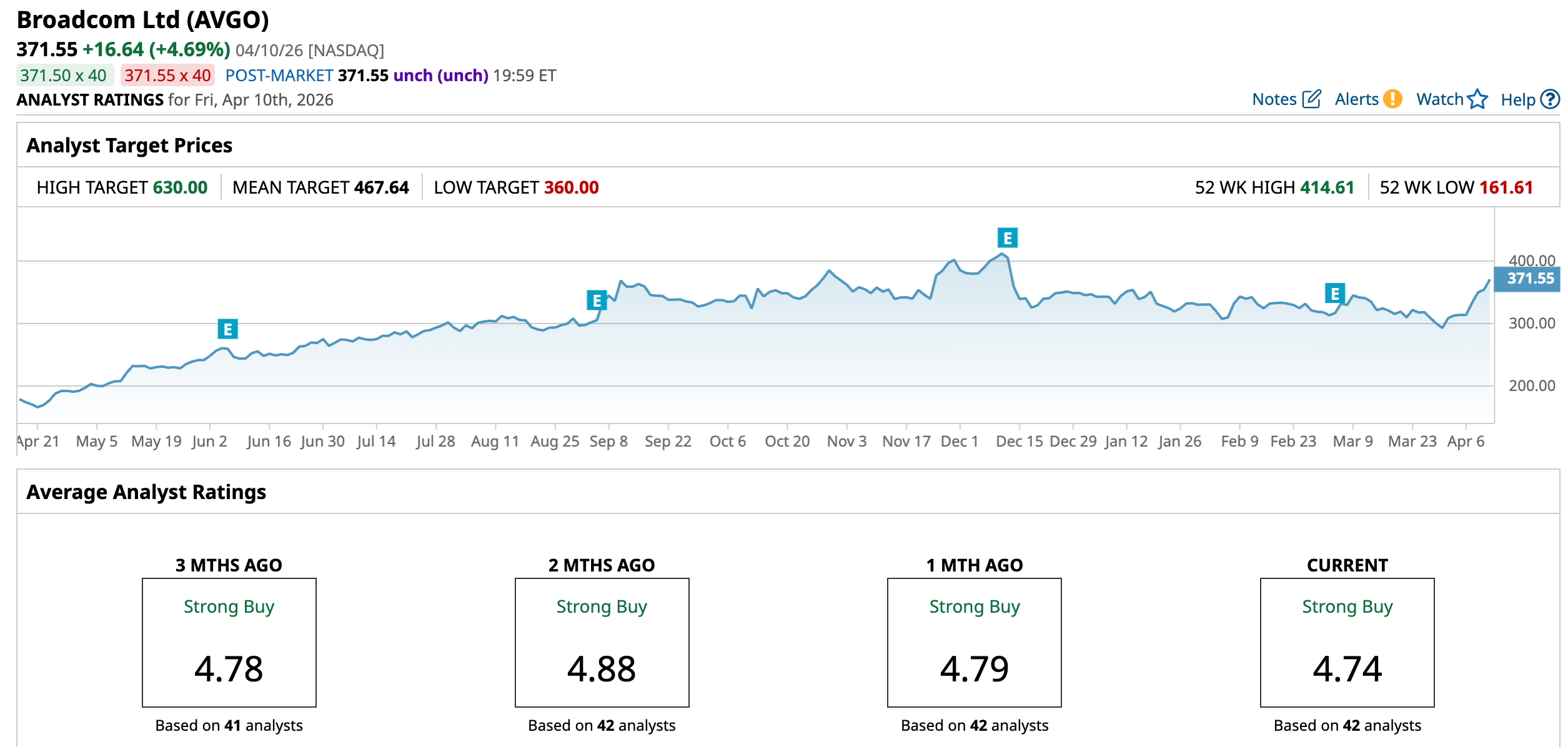

Stock #2: Broadcom

Broadcom, founded in 1961 and based in Palo Alto, has evolved into one of the most powerful names in global tech, with a market cap of $1.76 trillion. Its semiconductors may not be consumer-facing, but they quietly power cloud infrastructure, AI data centers, smartphones, broadband, and industrial systems. Alongside this, Broadcom has built a strong infrastructure software business rooted in long-term enterprise relationships, creating a durable edge through high-margin chips and sticky, mission-critical software.

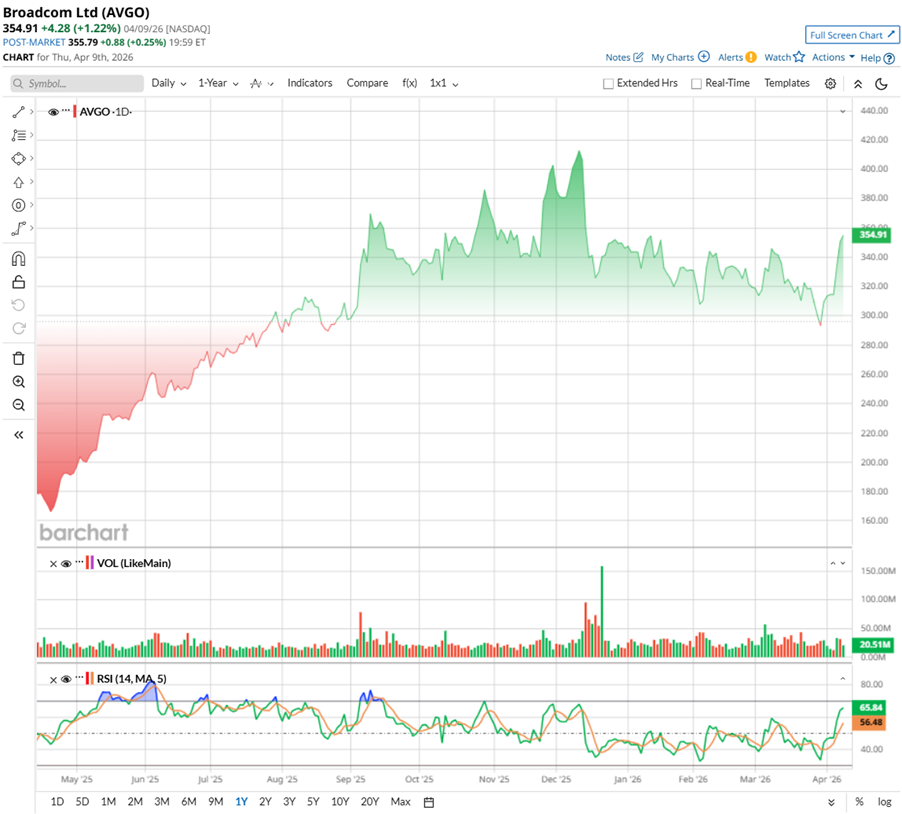

Broadcom stock has been on a powerful run, and investors have clearly rewarded its AI-led playbook. Over the past 52 weeks, AVGO has surged 115.64%, driven by strong AI networking demand, a successful VMware integration, and steady high-margin software earnings. Along the way, the stock notched 44 new highs, even touching a peak of $414.60 on Dec. 10, before cooling off and currently sitting about 10.38% below those levels.

Still, the recent pullback does not signal weakness, but looks more like a pause. Momentum is starting to pick up again, with shares up 7.35% so far in 2026 and jumping by a sharp 18.12% over the past five days. Technically, the 14-day RSI sits near 70.88, suggesting improving strength but now in overbought territory. At the same time, rising volume points to renewed buying interest.

Broadcom trades at a premium, with the stock currently priced around 35.83 times forward adjusted earnings and 16.81 times forward sales – both above the sector averages. That may seem expensive, but it also reflects confidence in its strong cash flow, scale, and steady earnings outlook.

Additionally, AVGO's strength shows up in shareholder returns. The company recently raised its quarterly dividend to $0.65 per share last year, bringing the annual payout to $2.60 per share and extending a 15-year streak of increases. With a payout ratio of about 34.1%, Broadcom still has room to reinvest while rewarding investors consistently.

Broadcom started fiscal 2026 on a strong note, keeping the momentum going from last year. In its Q1 report released on March 4, the company delivered revenue of $19.3 billion, up 29% YOY, surging past Street’s projections, while non-GAAP EPS rose 28% to $2.05, marking its ninth straight quarterly earnings beat.

Its Semiconductor Solutions segment revenue jumped 52% annually to $12.5 billion, driven largely by booming AI demand. Big partnerships with players like Alphabet (GOOG) (GOOGL) and Anthropic are fueling this growth. AI revenue alone came in at $8.4 billion, more than doubling annually and beating expectations, thanks to strong demand for custom AI chips and networking solutions. Meanwhile, its Infrastructure Software business added another $6.8 billion in revenue, providing steady support.

Financially, Broadcom looks solid. Cash flow from operations rose 35% to $8.3 billion, while free cash flow climbed 33% to $8 billion. The company also ended the quarter with $14.17 billion in cash and cash equivalents and approved a new $10 billion buyback program, easing concerns around funding needs.

Looking ahead, management guided for Q2 revenue of around $22 billion, implying 47% growth, with AI semiconductor revenue expected at $10.7 billion. With expanding AI deals with Anthropic and Google, Broadcom appears well-positioned to push past its long-term targets.

Wall Street sees Broadcom riding the AI wave in a big way, with revenue expected to reach about $104.6 billion in fiscal 2026. Earnings are projected to jump 76% YOY to $9.91 per share, with another strong 61.2% annual growth to $15.97 in 2027.

Analysts are confident, with AVGO stock having an overall “Strong Buy” rating. Of the 42 analysts tracking the stock, 35 back it with a “Strong Buy,” three have a “Moderate Buy,” while four sit on the sidelines with a “Hold" rating.

AVGO’s average target of $467.64 suggests an upside potential of 25.86% from the current price levels. The Street’s highest $630 price target hints the stock could rally as much as 69.56%.

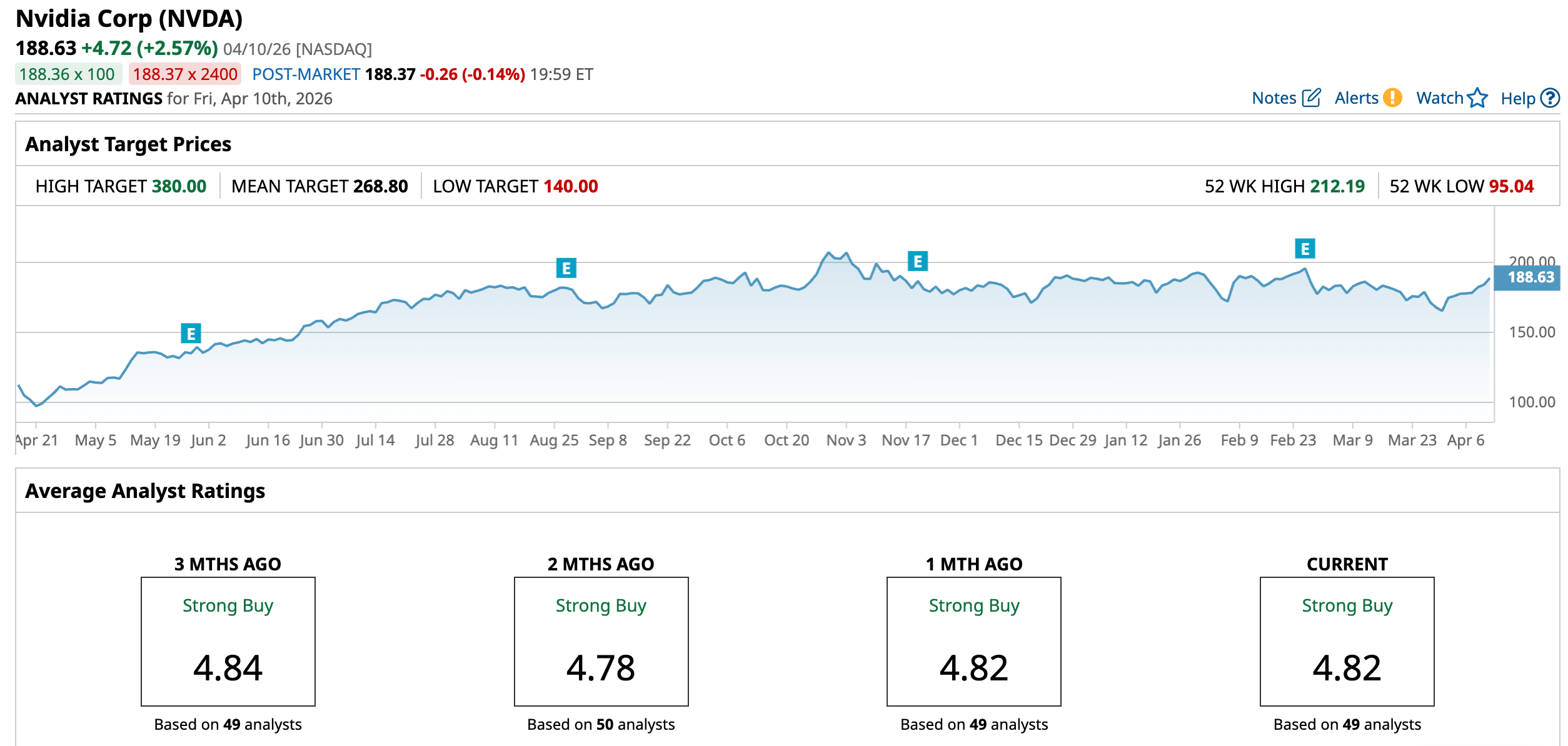

Stock #3: NVIDIA

Founded in 1993 and based in Santa Clara, California, NVIDIA has become a pioneer in GPUs and AI-driven computing. From gaming to data centers and automotive tech, its innovations have reshaped industries, powering the AI revolution. Beyond technology, Nvidia champions energy-efficient designs and diversity initiatives, combining cutting-edge innovation with responsibility, cementing its role as a cornerstone of modern high-performance computing. It currently boasts a market cap of about $4.6 trillion.

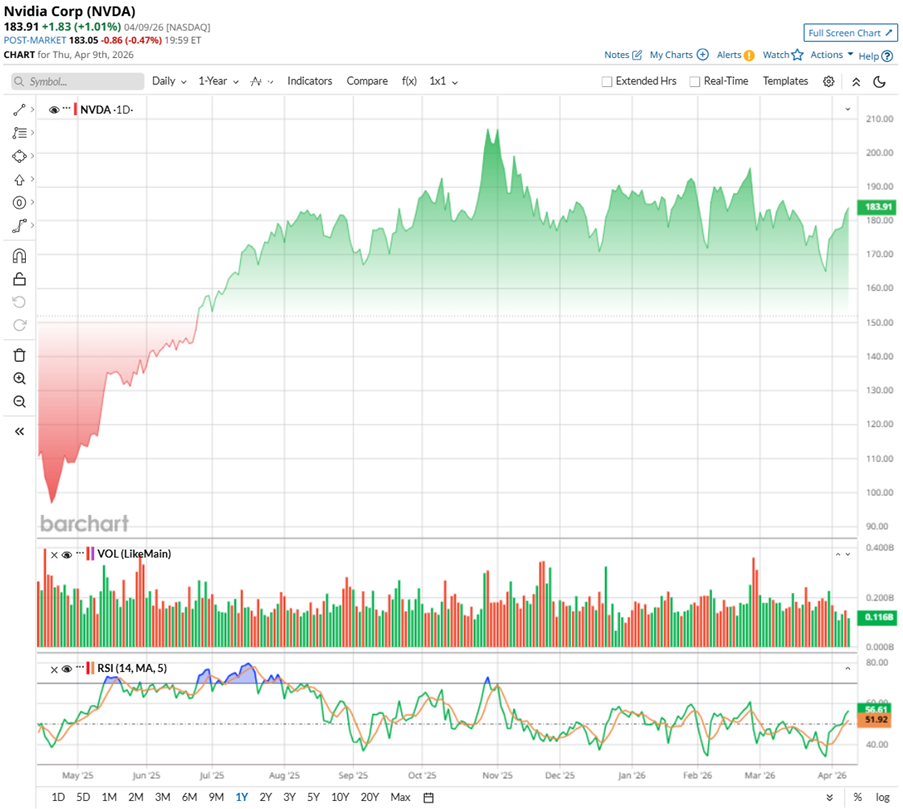

Shares of NVIDIA have moved in a start-stop pattern over the past year, rising sharply and then pausing before the next leg up. The stock hit new highs 44 times in 52 weeks, peaking at $212.19 in October before pulling back about 11%. Even with that dip, the stock is still up roughly 75.36% over the past 52 weeks.

In 2026, things have been less smooth, with slight declines as concerns around AI spending and rising competition weighed on sentiment. That said, sentiment has already shown signs of turning, with recent geopolitical easing helping the stock bounce back.

Technically, momentum is stabilizing again, with rising volumes and 14-day RSI improving – suggesting this may be a pause, not a trend break.

From a valuation standpoint, NVDA does not look as stretched now. It trades around 23.76 times forward adjusted earnings, below its historical levels and even the sector average, with room to ease further if AI growth holds strong. Its price-to-sales ratio has also cooled to 12.41 times. Plus, NVIDIA has steadily paid dividends for over a decade – small, but backed by strong cash flows.

When we look at NVIDIA's financials, it suggests just how strong the business is running. Its fiscal Q4 2026 numbers, released in February, made that clear. Revenue jumped 73.2% YOY to $68.1 billion, while adjusted earnings climbed 82% annually to $1.62 per share – both beating the Street’s estimates. The real engine remains its data center segment, where revenue soared roughly 75% YOY to $62.3 billion as companies continue pouring money into AI infrastructure. Even gaming held up well, growing 47% YOY.

All this strength shows up clearly in its financials. NVIDIA is sitting on over $62 billion in cash with relatively low debt, and it generated massive free cash flow of nearly $96.6 billion for the full year. That kind of cash gives it serious flexibility, whether it’s investing in future tech or rewarding shareholders. In fiscal 2026 alone, it returned $41.1 billion through buybacks and dividends, with another $58.5 billion still authorized.

Looking ahead, the runway still looks long. At its GTC event, management projected up to $1 trillion in revenue from its Blackwell and Vera Rubin AI platforms between 2025 and 2027. Management expects a strong start to fiscal 2027, guiding for first-quarter total revenue of around $78 billion, which is another sign that momentum remains firmly intact.

Analysts are even slightly more optimistic, forecasting about $78.8 billion in revenue, with earnings jumping 120.8% YOY to $1.70 per share. Looking further ahead, EPS is projected to climb 69.4% annually in fiscal 2027 to $7.74, followed by another 31.8% growth in fiscal 2028 to $10.20, pointing to sustained, high-growth ahead.

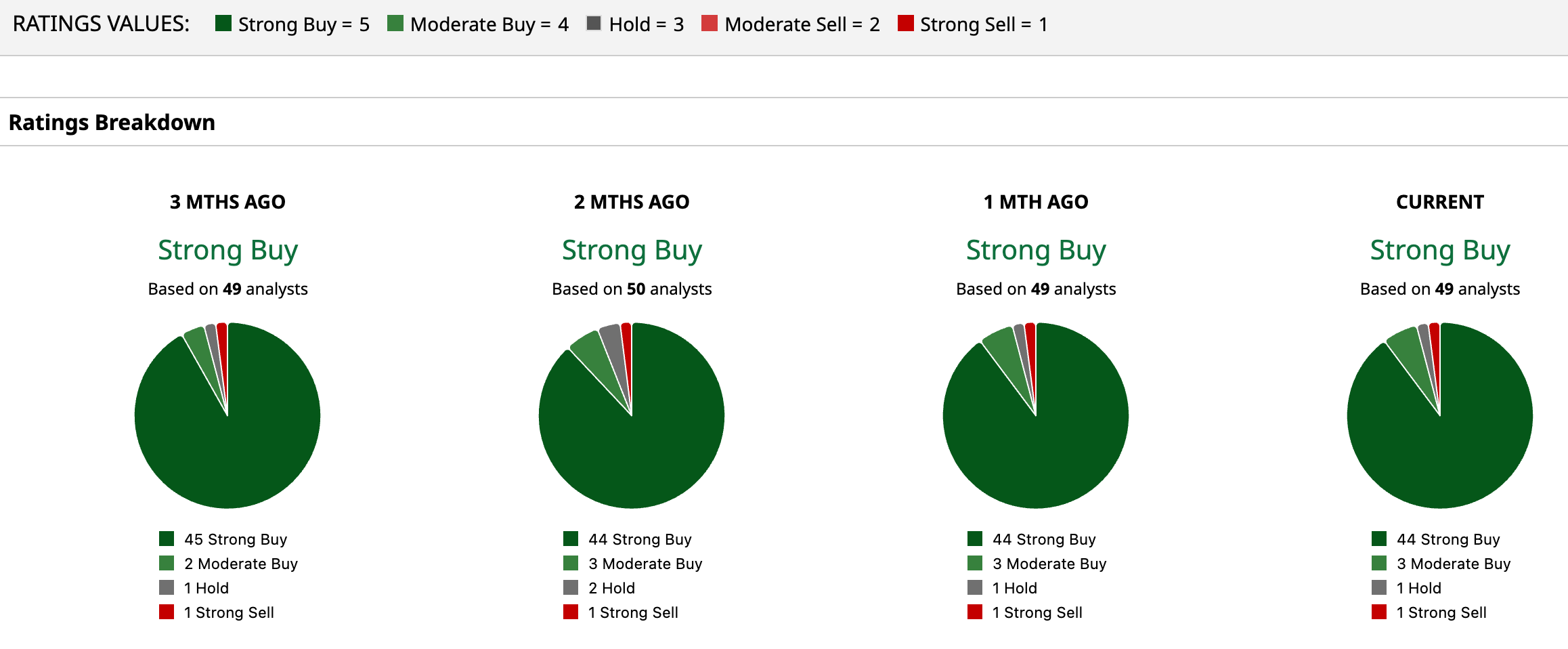

Overall, analysts are upbeat about the chip giant’s growth potential, giving the stock a consensus rating of “Strong Buy.” Of the 49 analysts covering the stock, 44 advise a “Strong Buy,” three suggest “Moderate Buy,” one recommends a “Hold,” and the remaining one has a “Strong Sell.”

The average analyst price target for NVDA is $268.80, indicating potential upside of 42.5%. The Street-high target price of $380 suggests that the stock could rally as much as 101.5% from here.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart