Wall Street major Morgan Stanley's upgrade of the aluminum company Alcoa (AA) to “Overweight” resulted in its shares rising by more than 2%. The institution's bull case was primarily based on the disruptions brought about by the war in the Middle East, a region that accounts for 9% of the global aluminum supply. About 70% of which is exported.

Consequently, the firm has revised its pricing for Alcoa's aluminum segment higher by 13% in 2026, along with a 41% and 52% upward revision in EBITDA and EPS, respectively.

About Alcoa

Founded way back in 1888, Alcoa is a pure upstream aluminum company and operates across the entire aluminum value chain. It is involved in bauxite mining, alumina refining, and aluminum smelting, while also owning its own power assets. It has operations in about ten countries worldwide.

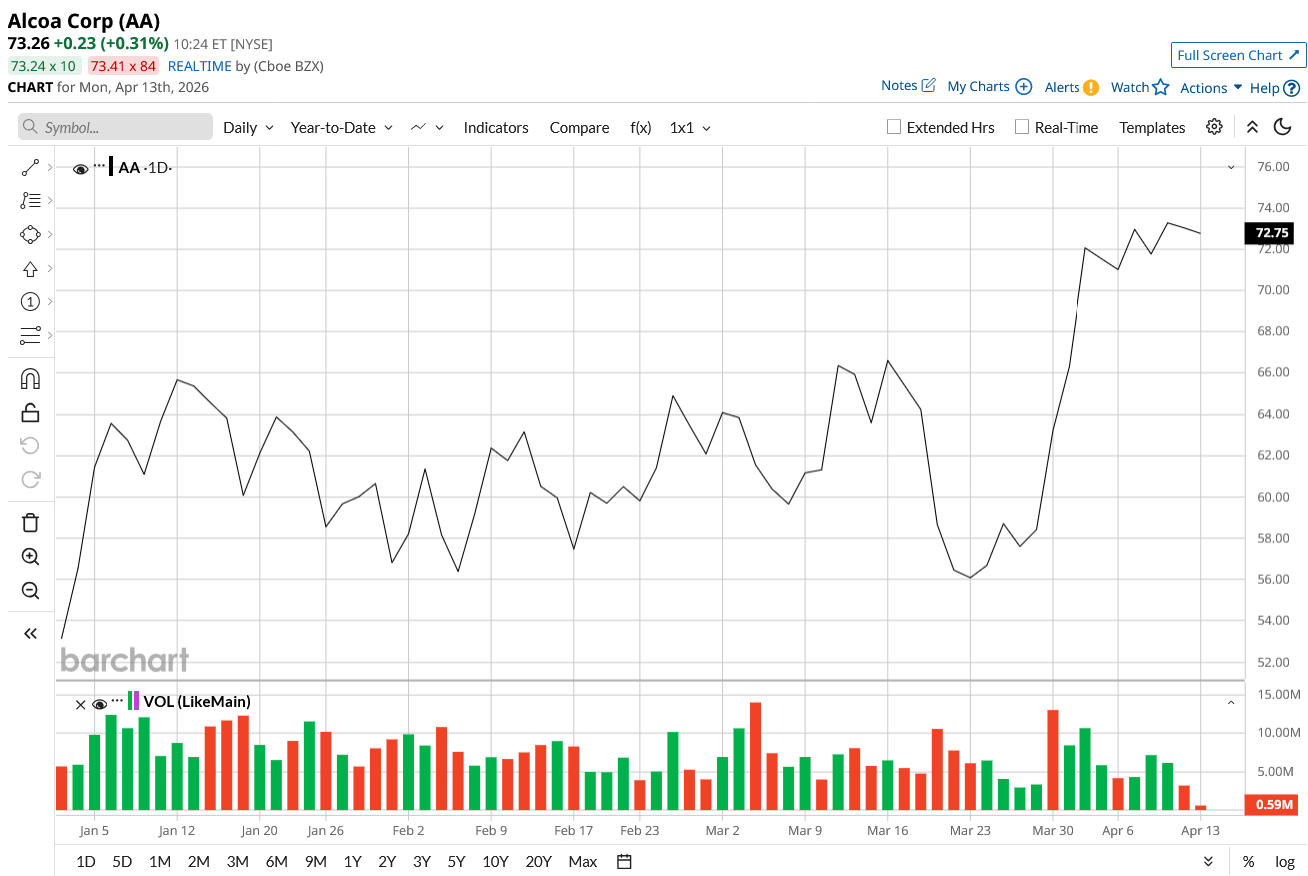

Valued at a market cap of about $19.3 billion, AA stock is up 39% on a year-to-date (YTD) basis.

Notably, Morgan Stanley's reasons for owning Alcoa's shares currently are solid. However, they are tactical. Short-term. The question is, can Alcoa be a “Buy” for the long term?

Solid Q4

Although earnings missed Wall Street's estimates, production and shipments increased when compared to the prior year. In fact, earnings also went up on a year-over-year (YoY) basis.

Revenues for the fourth quarter, which ended Dec. 31, 2025, were at $3.45 billion. This was a slight decrease from the previous year's $3.49 billion. In the same period, earnings went up by 11.8% to $0.85 per share, missing the consensus estimate of $0.93 per share.

Coming to production, both alumina and aluminum went up due to higher output in the company's Australian refineries and progress in its San Ciprián smelter. While alumina production increased by 3.8% on an annual basis to 2,481 thousand metric tons (kmt), aluminum production in the same period was up 5.8% to 604 kmt. Further, shipments for both also followed the same pattern. Alumina shipments rose to 2,324 kmt from 2,289 kmt in the year-ago period, and aluminum shipments increased as well, to 667 kmt from 641 kmt.

For 2026, Alcoa expects alumina production and shipments to be between 9.7 and 9.9 million metric tons and between 11.8 and 12 million metric tons, respectively. Similarly, for aluminum, production and shipments are expected to range between 2.4 and 2.6 million metric tons and 2.6 and 2.8 million metric tons, respectively.

2025 was also a positive year for the company in terms of its cash flow from operations. The metric witnessed a jump of over 90.5% in 2025 to $1.2 billion, as it closed the quarter with a cash balance of $1.6 billion and no short-term debt on its books.

Notably, even after a strong rally in 2026, the AA stock is trading at undervalued levels. While its forward P/E and P/S of 11.40 and 1.33 are below the sector medians, the EV/EBITDA metric is a more appropriate valuation metric for a company like Alcoa, which is involved in heavy capex. With a forward EV/EBITDA of 6.15, it is below the sector median of 8.44.

Allure of Alcoa

Aluminum has been in short supply over the past few years as production could not keep up with the high demand after the pandemic. Moreover, this scenario is set to continue, with Goldman Sachs raising its forecasts for aluminum prices in both 2026 and 2027.

That is good news for Alcoa, but amid many competitors, how can Alcoa be a prime beneficiary of this trend?

Well, Alcoa enjoys a crucial advantage over its peers. Unlike secondary producers reliant on purchasing raw materials at elevated spot prices, Alcoa mines its own bauxite and refines its own alumina. By acquiring its joint venture partner, Alumina Limited, in 2024, Alcoa consolidated complete control over one of the largest bauxite and alumina operations globally. This upstream leverage provides a massive structural advantage, allowing the company to translate the widening primary metal deficit directly into robust free cash flow generation.

Then there is ELYSIS, a green smelting technology developed with Rio Tinto (RIO). ELYSIS is uniquely designed to emit pure oxygen instead of greenhouse gases during smelting. While traditional facilities consume carbon anodes and release roughly two tons of carbon dioxide for just a ton of metal produced, ELYSIS replaces these with proprietary inert anodes that emit pure oxygen. Moving beyond laboratory phases in 2024, the joint venture successfully scaled its technology to industrial testing using massive 450-kiloampere cells at the Alma smelter in Quebec. It positions Alcoa to not only decarbonize its own output but also to potentially license this green technology package globally. Consequently, Alcoa could soon tap into high-margin licensing revenue streams as competitors rush to acquire the system to satisfy increasingly strict global environmental mandates.

When looking at scale, Alcoa holds up well. While looking at raw scale based on 2024 and 2025 metrics, Rio Tinto leads with approximately 3.2 million tons of primary aluminum production, whereas Alcoa produces roughly 2.1 million tons. Century (CENX) trails significantly at under 800,000 tons. However, Alcoa remains exceptionally competitive because its premier bauxite mining assets in Australia and Brazil ensure an uninterrupted, high-quality raw material pipeline that smaller peers simply cannot replicate.

Despite strong market tailwinds, Alcoa is battling severe, localized operational headwinds. A major ongoing headache involves its San Ciprian complex in Spain, where exorbitant energy costs and restrictive labor agreements have forced the company to endure massive cash burns just to keep idle facilities running throughout 2024 and 2025. Furthermore, Alcoa faced intense regulatory scrutiny regarding its bauxite mining approvals in Western Australia. These delayed environmental permits forced the company to mine lower-grade ore profiles to sustain production, which inherently reduced refinery yields and increased operating costs per ton. Resolving these regulatory bottlenecks and finalizing a permanent solution for the bleeding Spanish assets remain the most critical internal hurdles the company must clear to fully capitalize on rising metal prices.

Analyst Opinion on AA Stock

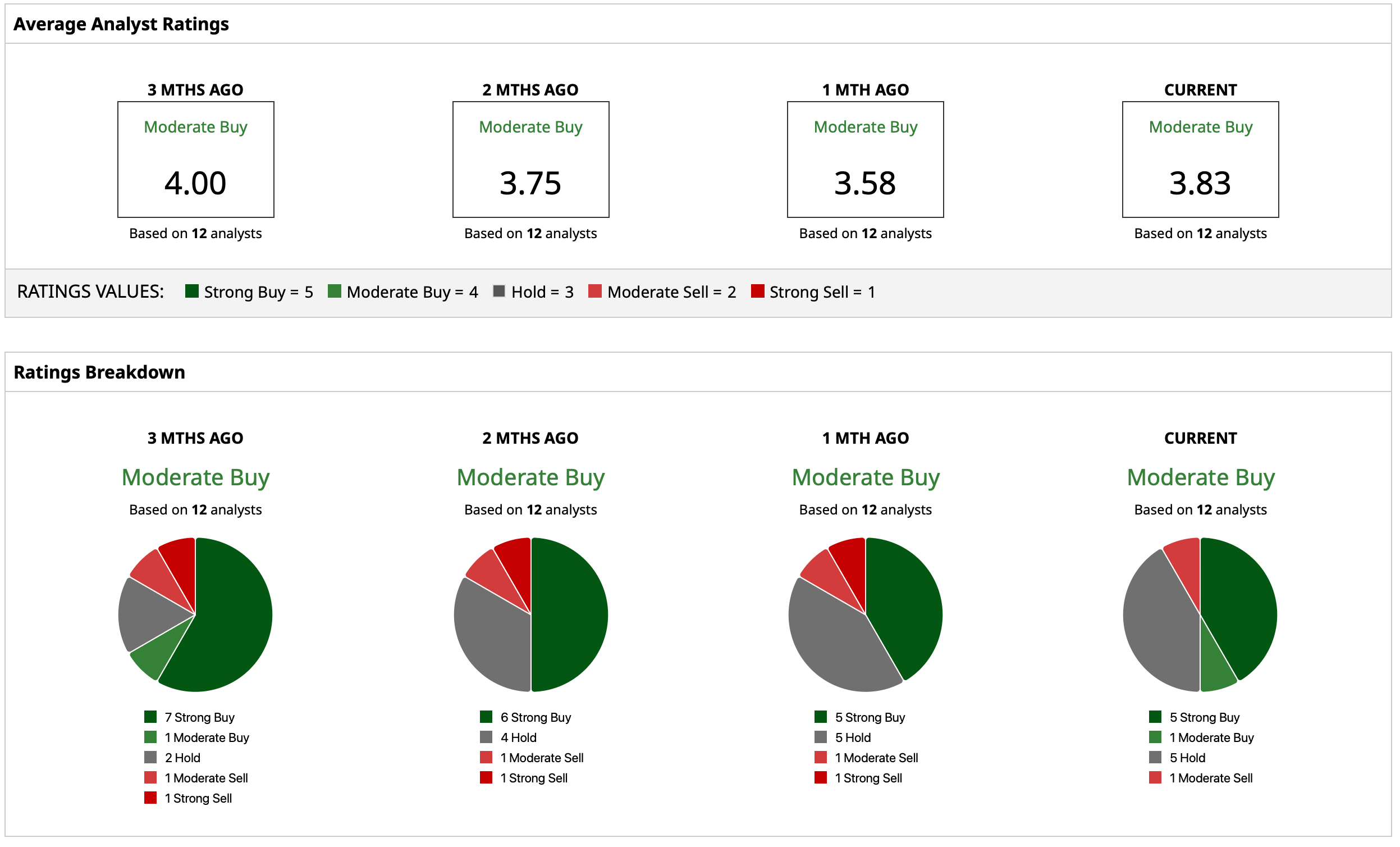

Considering all this, analysts remain cautiously optimistic about AA stock, with an overall rating of “Moderate Buy.” The mean target price has already been surpassed. The high target price of $96 indicates an upside potential of about 31% from current levels. Out of 12 analysts covering the stock, five have a “Strong Buy” rating, one has a “Moderate Buy” rating, five have a “Hold” rating, and one has a “Moderate Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart