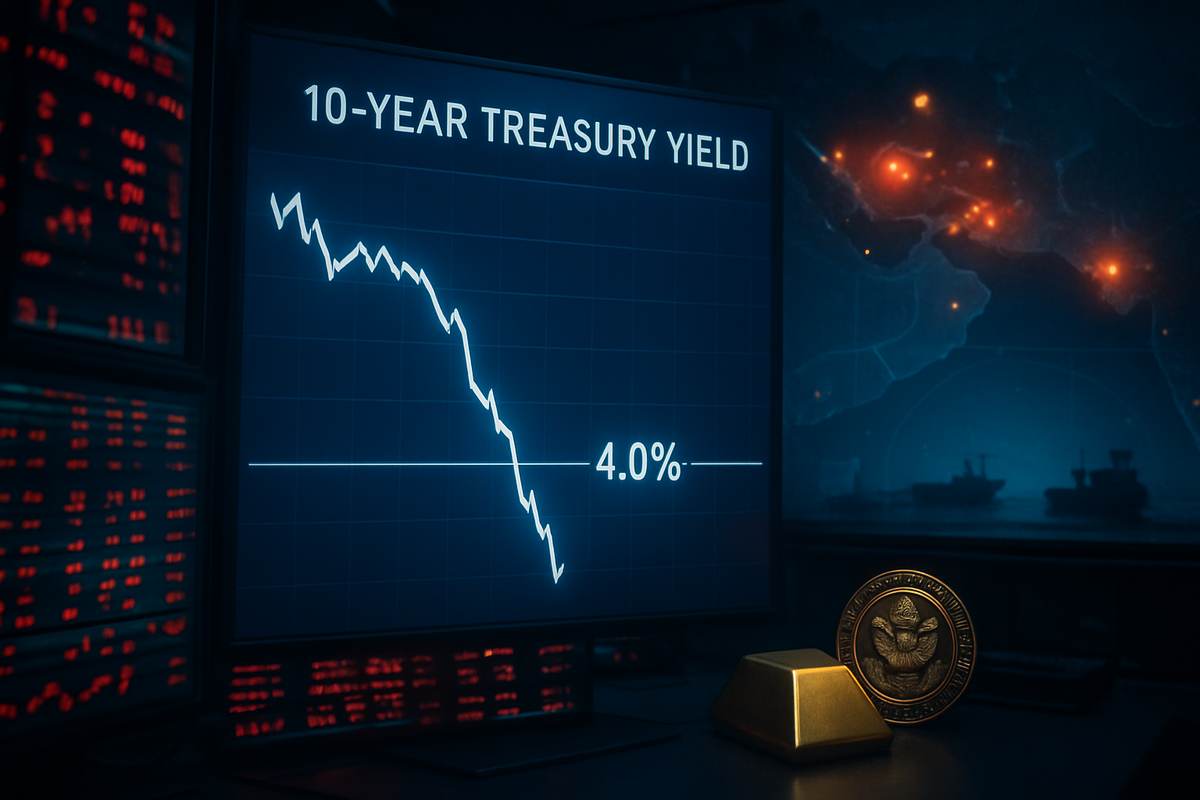

NEW YORK — In a dramatic reversal of the "higher-for-longer" narrative that has dominated the early months of 2026, the 10-year U.S. Treasury yield plummeted below the psychological 4.0% threshold today, March 20, 2026. This sudden surge in bond demand comes as a direct response to a rapidly deteriorating security situation in the Middle East and a simultaneous rout in global equity markets, which saw the S&P 500 post its worst single-session decline in nearly two years.

The flight to safety—a classic market maneuver during times of extreme geopolitical stress—is occurring despite "sticky" inflation data that just last week suggested the Federal Reserve might need to keep interest rates elevated. However, as news of the closure of the Strait of Hormuz and direct military engagements between major regional powers reached trading desks this morning, investors abandoned riskier assets, seeking the perceived sanctuary of U.S. government debt.

The catalysts for today’s market upheaval began in the early hours of the morning following reports that the Strait of Hormuz—a vital artery for 20% of the world’s oil supply—had been effectively shut down due to escalating hostilities between Israel and Iran. This follows a month of mounting tensions after the reported death of high-ranking Iranian officials, which has now transitioned from a localized shadow war into a full-scale regional confrontation involving direct state-on-state strikes.

As the news broke, the 10-year Treasury yield, which had been hovering near 4.25% earlier this week, cratered to 3.92% as the "buy-everything" panic hit the bond market. The timeline of this escalation has been swift; just forty-eight hours ago, analysts at JPMorgan Chase & Co. (NYSE: JPM) were projecting a stable yield environment based on strong domestic labor data. That outlook was discarded by noon today as major institutional funds pivoted to capital preservation. Key stakeholders, including global central banks and sovereign wealth funds, have reportedly increased their allocations to Treasuries and the iShares 20+ Year Treasury Bond ETF (NASDAQ: TLT), prioritizing liquidity over yield.

The initial reaction in the stock market was nothing short of a bloodbath. Technology giants that have led the 2025-2026 AI-driven bull market, such as Nvidia Corp (NASDAQ: NVDA) and Apple Inc. (NASDAQ: AAPL), saw their shares slide by 4.5% and 3.2% respectively, as the prospect of disrupted global trade and surging energy costs overshadowed recent earnings successes.

The primary "winners" in this volatile environment have been defense contractors and energy giants. Lockheed Martin (NYSE: LMT) and RTX Corporation (NYSE: RTX) both saw their stock prices surge by more than 6% in midday trading as investors anticipated a prolonged conflict and increased government procurement of missile defense systems. Similarly, Exxon Mobil Corp (NYSE: XOM) and Chevron Corp (NYSE: CVX) are benefiting from the supply-side shock, with Brent crude prices surging past $110 per barrel.

On the losing side, the financial sector is facing a dual threat. Banks like JPMorgan Chase & Co. (NYSE: JPM) and Bank of America Corp (NYSE: BAC) are seeing their net interest margins compressed by the sudden drop in long-term yields, even as the risk of credit defaults rises in a potential "war-recession" scenario. Consumer-facing companies, already struggling with the aforementioned "sticky" inflation, are now bracing for even higher input costs. Traditional retailers and logistics firms are expected to see their margins decimated by the spike in fuel prices and insurance premiums for cargo crossing the Indian Ocean.

Today’s flight to safety is particularly significant because it breaks the recent correlation between inflation and yields. Typically, sticky inflation (which currently sits at a resilient 3.2% headline CPI) would prevent yields from dropping significantly, as investors would demand a higher "inflation premium." However, the sheer magnitude of the Middle East crisis has temporarily rendered inflation a secondary concern to geopolitical survival. This event echoes the 1973 oil crisis and the early days of the 2020 pandemic, where "macro shocks" overrode standard economic indicators.

The ripple effects are already being felt across the globe. Competitors in the defense space from Europe and Asia are seeing similar spikes, while partners of the U.S. are being forced to choose between supporting the blockade-busting efforts or facing domestic political pressure over rising gas prices. From a policy perspective, this leaves the Federal Reserve in an impossible "Stagflationary Box": if they cut rates to support a sagging economy, they risk hyper-charging inflation; if they raise rates to combat $110 oil, they deepen the equity market's pain.

In the short term, markets will remain at the mercy of the headlines coming out of Tehran and Tel Aviv. If the closure of the Strait of Hormuz persists for more than a week, analysts expect the 10-year yield to drop even further, potentially testing the 3.5% level as a full-scale global recession becomes the base-case scenario. Strategically, multi-asset managers are already pivoting toward "defensive value," favoring companies with strong balance sheets and domestic supply chains that are insulated from the chaos in the Middle East.

Market opportunities may emerge for those positioned in alternative energy, as the sudden oil shock provides a renewed tailwind for the green transition—though this is a long-term play that offers little solace to investors watching their portfolios bleed today. A potential scenario where the U.S. and its allies successfully reopen shipping lanes could lead to a "relief rally," but the fundamental geopolitical landscape has likely been altered permanently, marking the end of the post-2024 period of relative market stability.

The events of March 20, 2026, represent a watershed moment for the global economy. The breach of the 4.0% yield level on the 10-year Treasury, despite persistent inflation, serves as a stark reminder that geopolitical risk remains the ultimate market mover. The "flight to safety" is currently shielding investors from total catastrophe, but it also signals a profound lack of confidence in the global status quo.

Moving forward, investors should watch for three critical indicators: the duration of the Strait of Hormuz closure, any shift in the Federal Reserve’s rhetoric regarding "emergency" rate cuts, and the resilience of the U.S. consumer in the face of triple-digit oil prices. While the bond market has provided a temporary haven today, the lasting impact of this conflict will likely be felt in every corner of the global financial system for months, if not years, to come.

This content is intended for informational purposes only and is not financial advice.