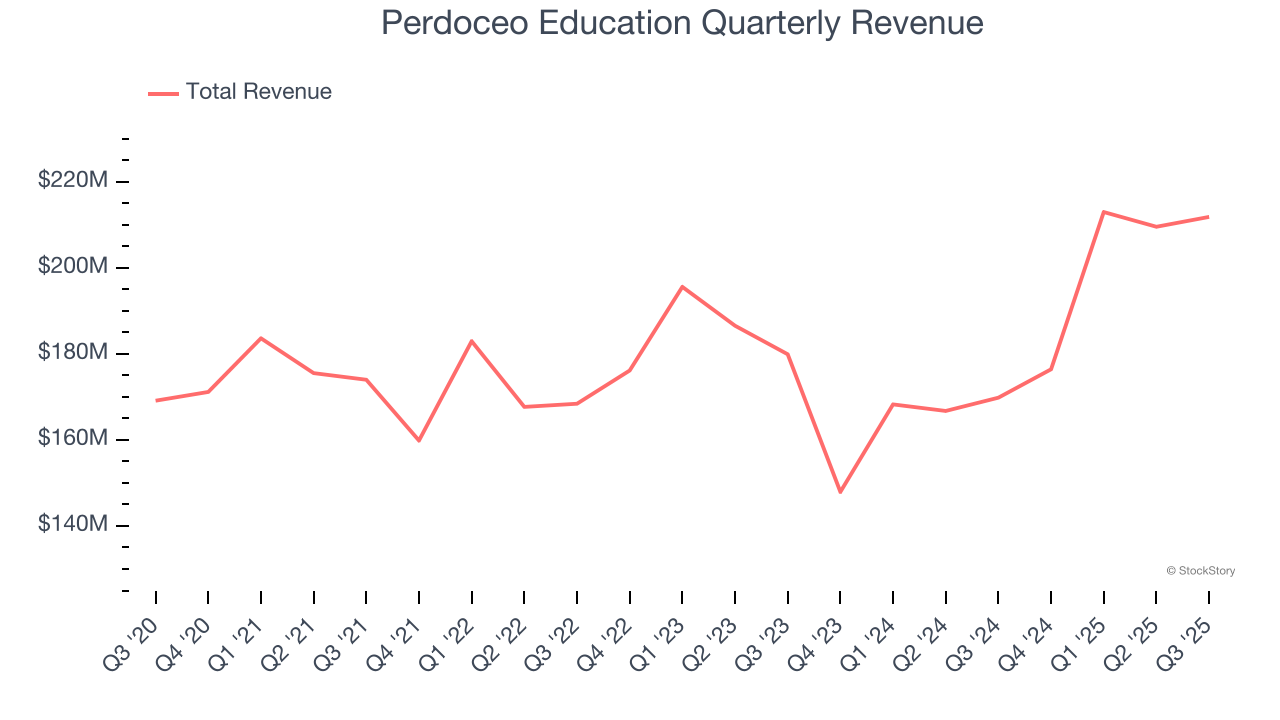

Higher education company Perdoceo Education (NASDAQ: PRDO) reported Q3 CY2025 results topping the market’s revenue expectations, with sales up 24.8% year on year to $211.9 million. Its non-GAAP profit of $0.65 per share was 6.6% above analysts’ consensus estimates.

Is now the time to buy Perdoceo Education? Find out by accessing our full research report, it’s free for active Edge members.

Perdoceo Education (PRDO) Q3 CY2025 Highlights:

- Revenue: $211.9 million vs analyst estimates of $207 million (24.8% year-on-year growth, 2.4% beat)

- Adjusted EPS: $0.65 vs analyst estimates of $0.61 (6.6% beat)

- Adjusted EBITDA: $152.7 million vs analyst estimates of $57.9 million (72.1% margin, significant beat)

- Management raised its full-year Adjusted EPS guidance to $2.55 at the midpoint, a 1.4% increase

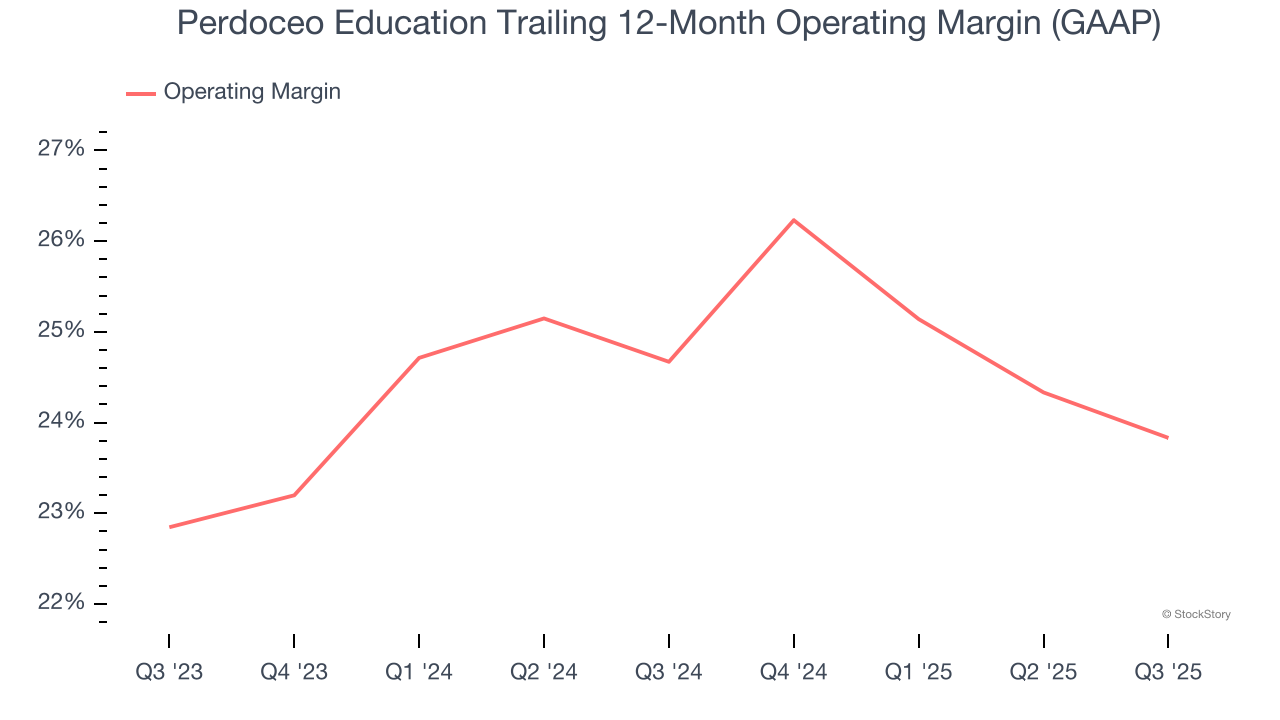

- Operating Margin: 24.1%, down from 26.4% in the same quarter last year

- Market Capitalization: $2.01 billion

Company Overview

Formerly known as Career Education Corporation, Perdoceo Education (NASDAQ: PRDO) is an educational services company that specializes in postsecondary education.

Revenue Growth

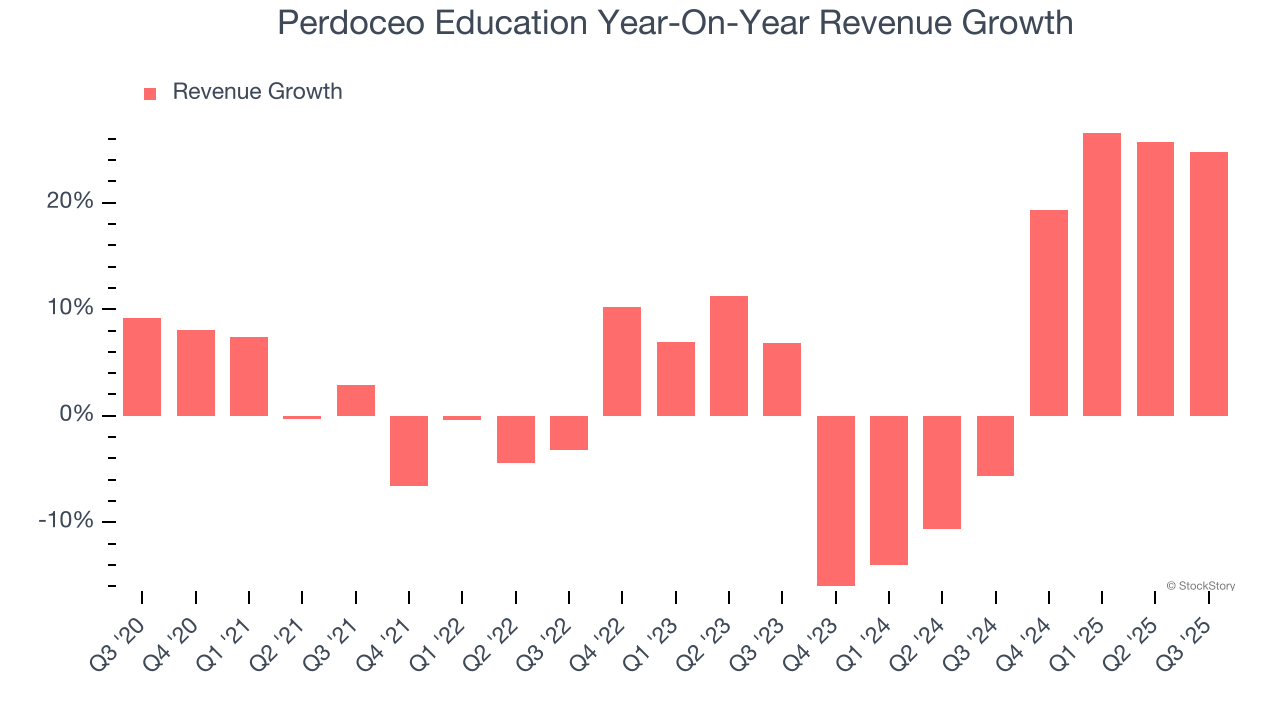

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Perdoceo Education’s 3.7% annualized revenue growth over the last five years was sluggish. This wasn’t a great result compared to the rest of the consumer discretionary sector, but there are still things to like about Perdoceo Education.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Perdoceo Education’s annualized revenue growth of 4.8% over the last two years is above its five-year trend, but we were still disappointed by the results.

This quarter, Perdoceo Education reported robust year-on-year revenue growth of 24.8%, and its $211.9 million of revenue topped Wall Street estimates by 2.4%.

We also like to judge companies based on their projected revenue growth, but not enough Wall Street analysts cover the company for it to have reliable consensus estimates. This signals Perdoceo Education could be a hidden gem because it doesn’t get attention from professional brokers.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Perdoceo Education’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 24.2% over the last two years. This profitability was elite for a consumer discretionary business thanks to its efficient cost structure and economies of scale.

In Q3, Perdoceo Education generated an operating margin profit margin of 24.1%, down 2.3 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

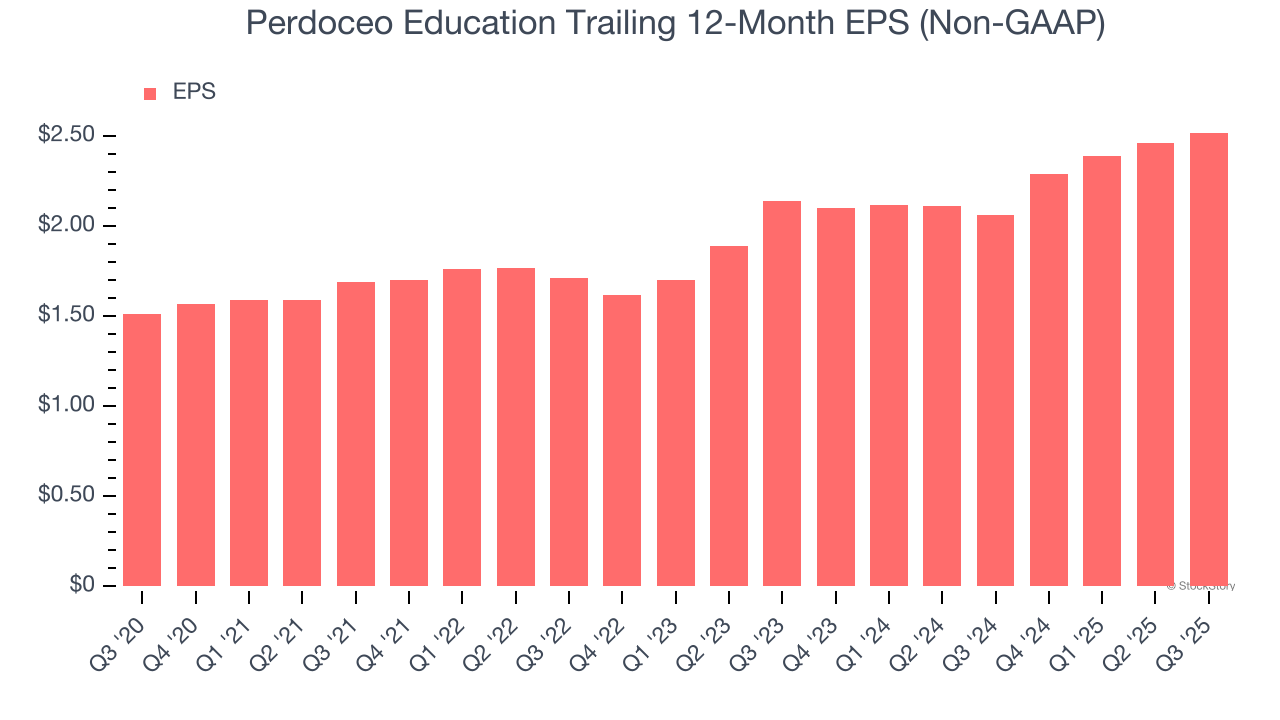

Perdoceo Education’s EPS grew at a decent 10.8% compounded annual growth rate over the last five years, higher than its 3.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q3, Perdoceo Education reported adjusted EPS of $0.65, up from $0.59 in the same quarter last year. This print beat analysts’ estimates by 6.6%. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data. This signals Perdoceo Education could be a hidden gem because it doesn’t have much coverage among professional brokers.

Key Takeaways from Perdoceo Education’s Q3 Results

We were impressed by how significantly Perdoceo Education blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $31.01 immediately following the results.

Perdoceo Education put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.