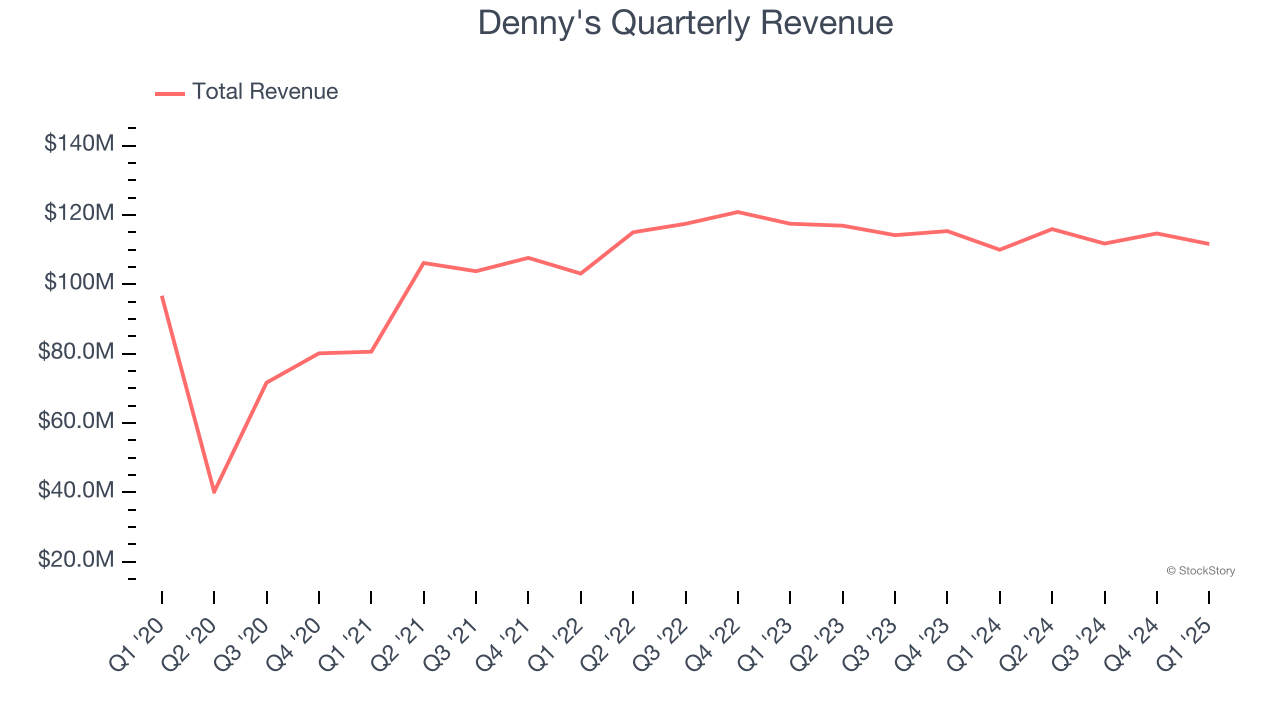

Diner restaurant chain Denny’s (NASDAQ: DENN) reported Q1 CY2025 results exceeding the market’s revenue expectations, with sales up 1.5% year on year to $111.6 million. Its non-GAAP profit of $0.08 per share was in line with analysts’ consensus estimates.

Is now the time to buy Denny's? Find out by accessing our full research report, it’s free.

Denny's (DENN) Q1 CY2025 Highlights:

- Revenue: $111.6 million vs analyst estimates of $110.1 million (1.5% year-on-year growth, 1.4% beat)

- Adjusted EPS: $0.08 vs analyst estimates of $0.08 (in line)

- Adjusted EBITDA: $16.82 million vs analyst estimates of $17.82 million (15.1% margin, 5.7% miss)

- EBITDA guidance for the full year is $82.5 million at the midpoint, in line with analyst expectations

- Operating Margin: 4.7%, down from 9.1% in the same quarter last year

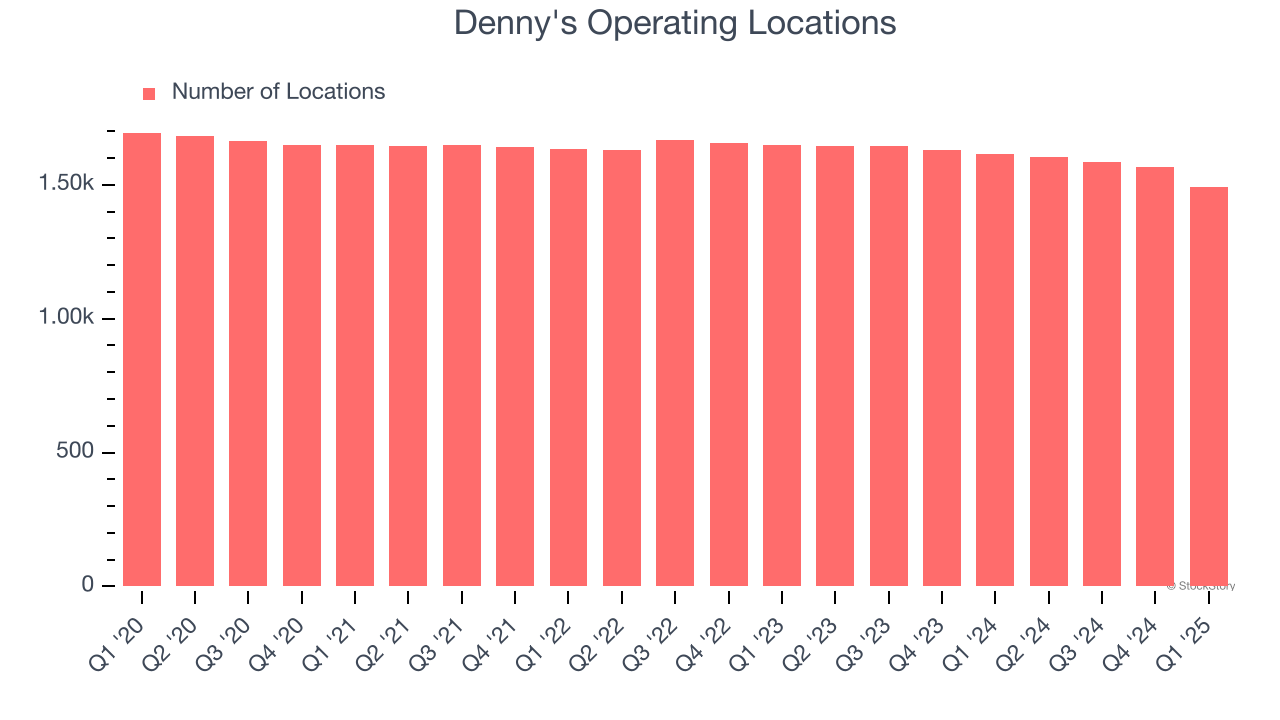

- Locations: 1,491 at quarter end, down from 1,614 in the same quarter last year

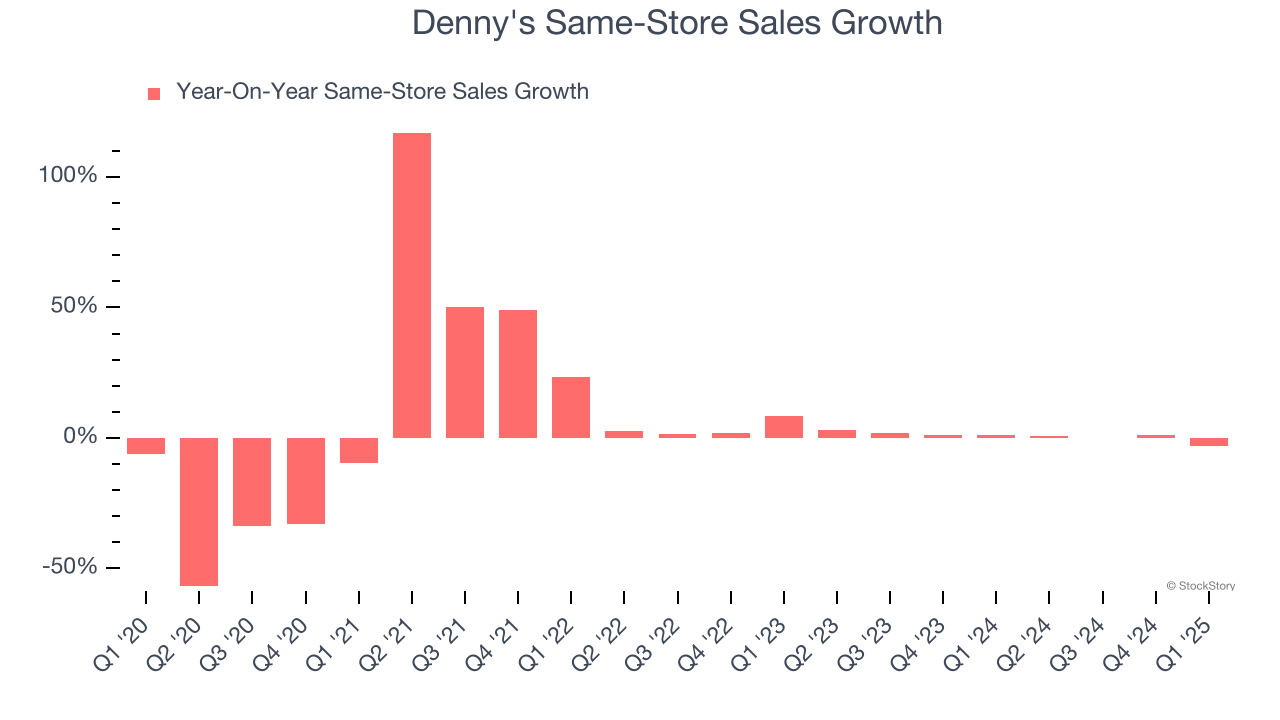

- Same-Store Sales fell 3% year on year (1.3% in the same quarter last year)

- Market Capitalization: $195.1 million

Kelli Valade, Chief Executive Officer, stated, "The beginning of the year has presented significant challenges for consumers, which is evident in our results. Our teams have remained focused on executing against our strategic initiatives and winning with our guests, despite these macro headwinds. This included staying true to our Denny's flagship, by focusing on compelling value, being strategic in reaching new younger demographics through innovative partnerships and new menu offerings. Keke's continued to steal share in its home state of Florida while also growing to its seventh state, Georgia. The dedication of our teams and franchisees continue to push our brands forward and we remain committed to navigating these headwinds together."

Company Overview

Open around the clock, Denny’s (NASDAQ: DENN) is a chain of diner restaurants serving breakfast and traditional American fare.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $454 million in revenue over the past 12 months, Denny's is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale.

As you can see below, Denny’s revenue declined by 5.2% per year over the last six years (we compare to 2019 to normalize for COVID-19 impacts) as it closed restaurants.

This quarter, Denny's reported modest year-on-year revenue growth of 1.5% but beat Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 5.2% over the next 12 months. Although this projection indicates its newer menu offerings will fuel better top-line performance, it is still below the sector average.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations often determines how much revenue it can generate.

Denny's operated 1,491 locations in the latest quarter. Over the last two years, the company has generally closed its restaurants, averaging 2.7% annual declines.

When a chain shutters restaurants, it usually means demand for its meals is waning, and it is responding by closing underperforming locations to improve profitability.

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at restaurants open for at least a year.

Denny’s demand within its existing dining locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and Denny's is attempting to boost same-store sales by closing restaurants (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Denny’s same-store sales fell by 3% year on year. This decline was a reversal from its historical levels.

Key Takeaways from Denny’s Q1 Results

It was good to see Denny's narrowly top analysts’ revenue expectations this quarter. On the other hand, its EBITDA missed significantly and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2.2% to $3.70 immediately after reporting.

The latest quarter from Denny’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.