Digital advertising platform Magnite (NASDAQ: MGNI) fell short of the market’s revenue expectations in Q1 CY2025 as sales rose 4.3% year on year to $155.8 million. Its non-GAAP profit of $0.12 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Magnite? Find out by accessing our full research report, it’s free.

Magnite (MGNI) Q1 CY2025 Highlights:

- Revenue: $155.8 million vs analyst estimates of $159.9 million (4.3% year-on-year growth, 2.6% miss)

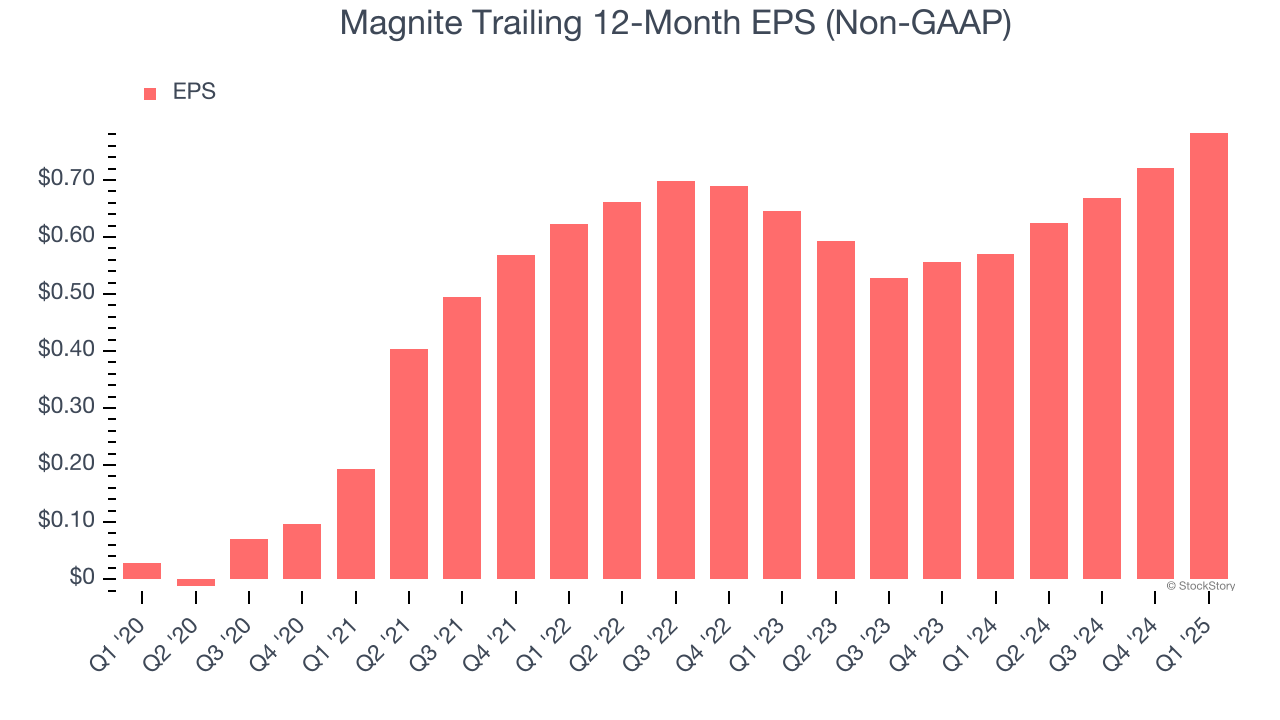

- Adjusted EPS: $0.12 vs analyst estimates of $0.06 (significant beat)

- Adjusted EBITDA: $36.8 million vs analyst estimates of $30.43 million (23.6% margin, 20.9% beat)

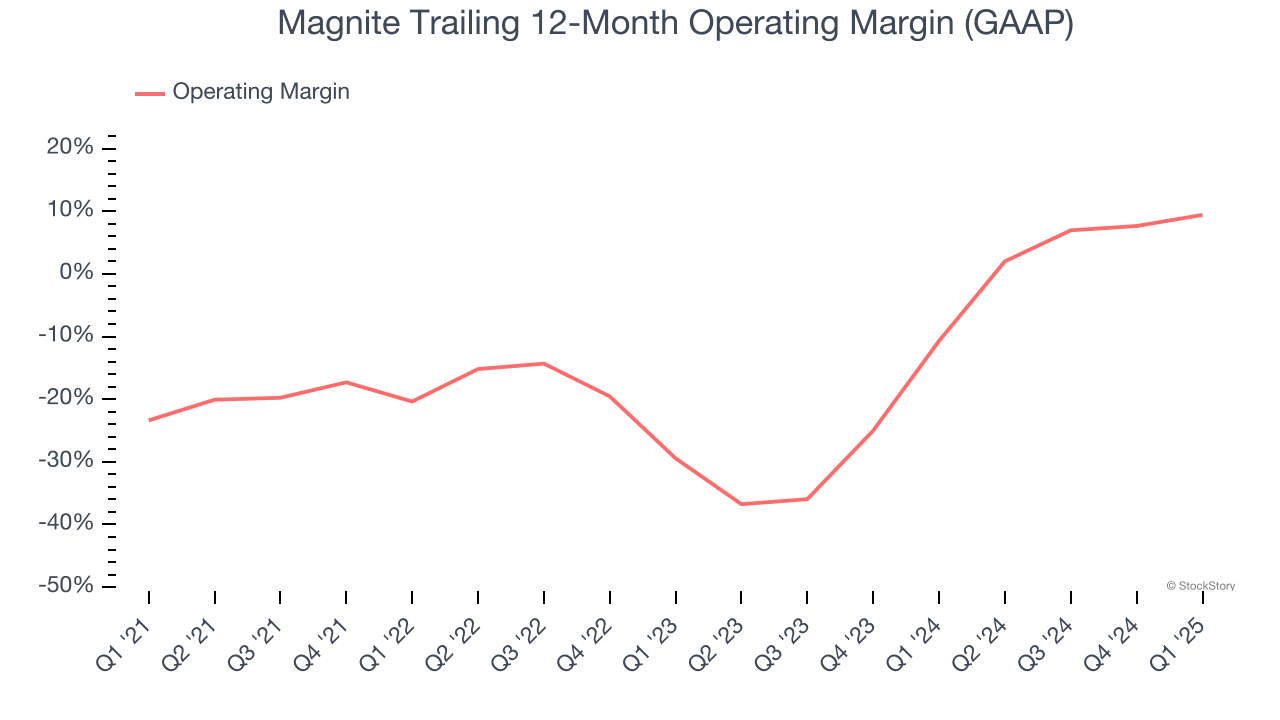

- Operating Margin: -0.9%, up from -9.3% in the same quarter last year

- Free Cash Flow was -$11.82 million compared to -$66.28 million in the same quarter last year

- Market Capitalization: $1.74 billion

“We beat the high end of our CTV and DV+ top line guidance in the first quarter, with significant outperformance in Adjusted EBITDA. Our performance has remained strong to start Q2. However, we have taken a more cautious approach to our outlook and guidance due to tariff-driven economic uncertainty. In CTV, we continue to see strong programmatic adoption and are very pleased with the growth of Netflix and their continued rollout of programmatic globally. On the DV+ side of the business, we applaud the monumental antitrust ruling against Google. This ruling and its ensuing remedies have the potential to radically transform the open internet and create a more level playing field, which could significantly increase our monetization opportunities and market share, possibly as soon as next year,” said Michael G. Barrett, CEO of Magnite.

Company Overview

Born from the 2020 merger of Rubicon Project and Telaria, Magnite (NASDAQ: MGNI) operates the world's largest independent sell-side advertising platform that automates the buying and selling of digital advertising inventory across all channels and formats.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

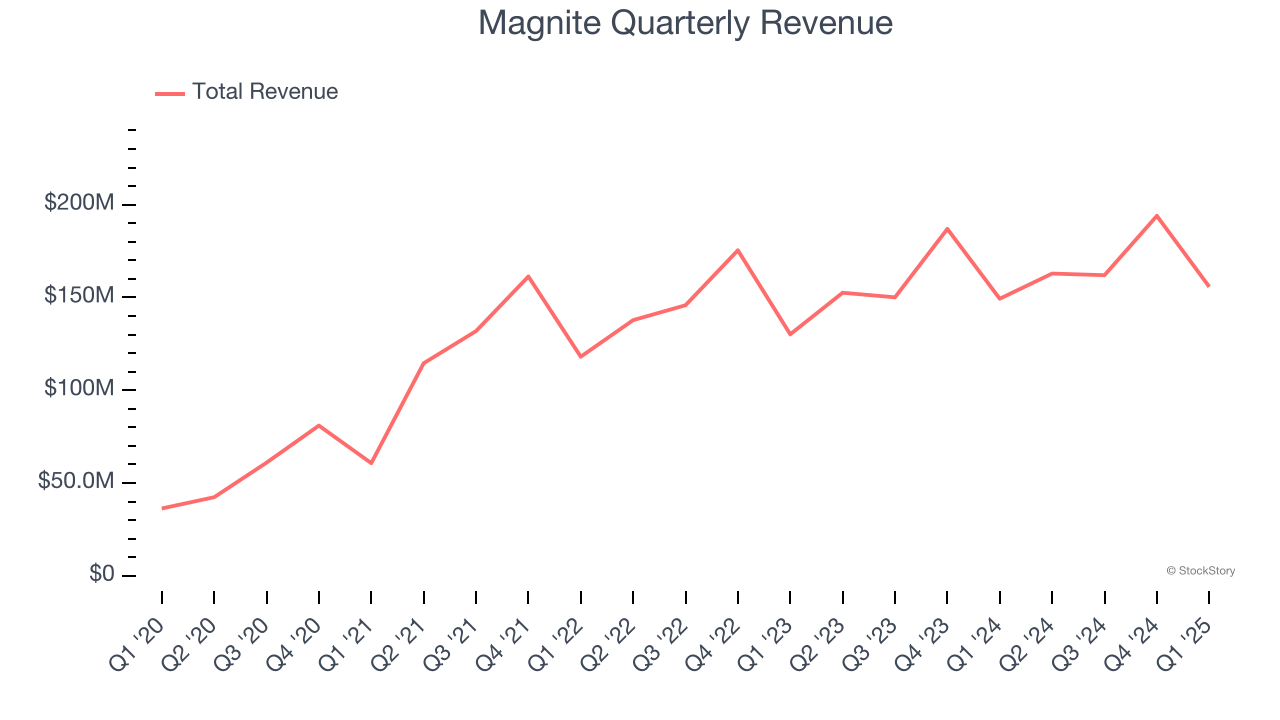

With $674.6 million in revenue over the past 12 months, Magnite is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

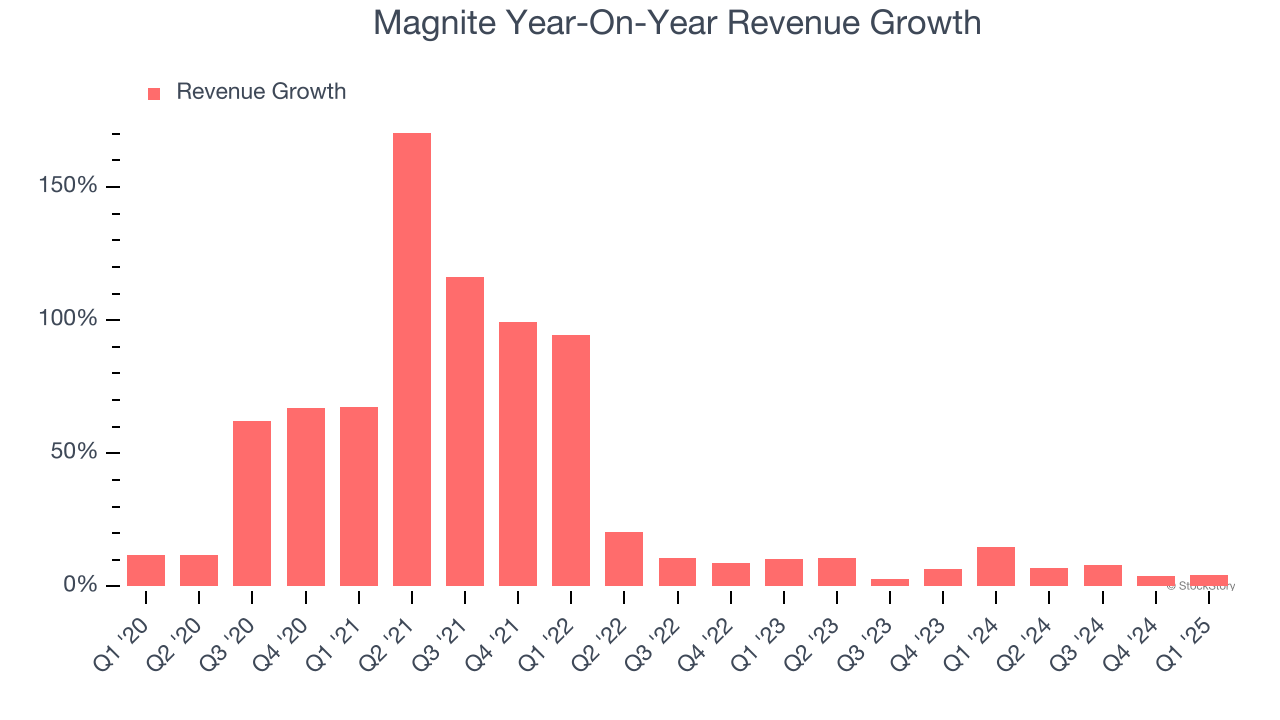

As you can see below, Magnite’s 33.3% annualized revenue growth over the last five years was incredible. This is a great starting point for our analysis because it shows Magnite’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Magnite’s annualized revenue growth of 7% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Magnite’s revenue grew by 4.3% year on year to $155.8 million, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 13.8% over the next 12 months, an improvement versus the last two years. This projection is admirable and suggests its newer products and services will spur better top-line performance.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Although Magnite broke even this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 12.8% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Magnite’s operating margin rose by 32.8 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q1, Magnite generated a negative 0.9% operating margin.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Magnite’s EPS grew at an astounding 94.7% compounded annual growth rate over the last five years, higher than its 33.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into Magnite’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Magnite’s operating margin expanded by 32.8 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Magnite reported EPS at $0.12, up from $0.06 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Magnite’s full-year EPS of $0.78 to grow 13.8%.

Key Takeaways from Magnite’s Q1 Results

We were impressed by how significantly Magnite blew past analysts’ EPS expectations this quarter. On the other hand, its revenue missed significantly. Overall, this print had some key positives. The stock traded up 8.3% to $13.50 immediately following the results.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.