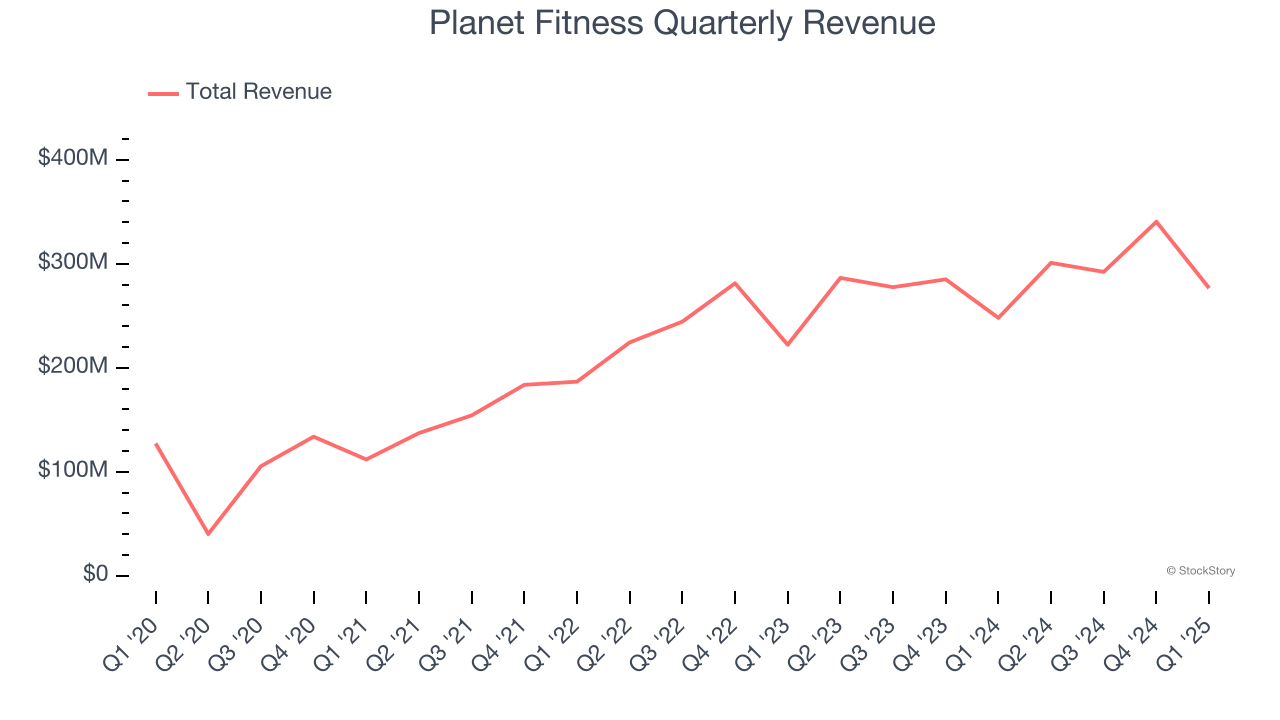

Inclusive gym franchise company (NYSE: PLNT) missed Wall Street’s revenue expectations in Q1 CY2025, but sales rose 11.5% year on year to $276.7 million. Its non-GAAP profit of $0.59 per share was 4.1% below analysts’ consensus estimates.

Is now the time to buy Planet Fitness? Find out by accessing our full research report, it’s free.

Planet Fitness (PLNT) Q1 CY2025 Highlights:

- Revenue: $276.7 million vs analyst estimates of $279.9 million (11.5% year-on-year growth, 1.2% miss)

- Adjusted EPS: $0.59 vs analyst expectations of $0.62 (4.1% miss)

- Adjusted EBITDA: $117 million vs analyst estimates of $120.3 million (42.3% margin, 2.7% miss)

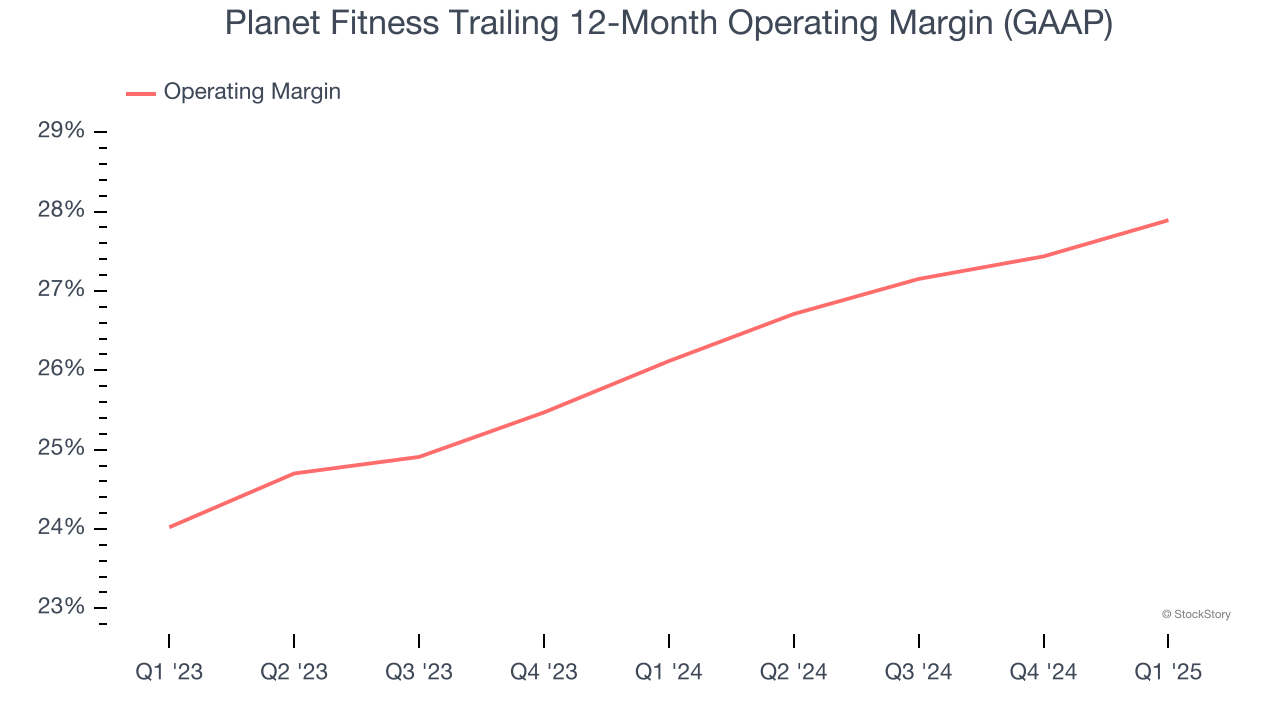

- Operating Margin: 28.6%, up from 26.5% in the same quarter last year

- Free Cash Flow Margin: 40.1%, up from 25.6% in the same quarter last year

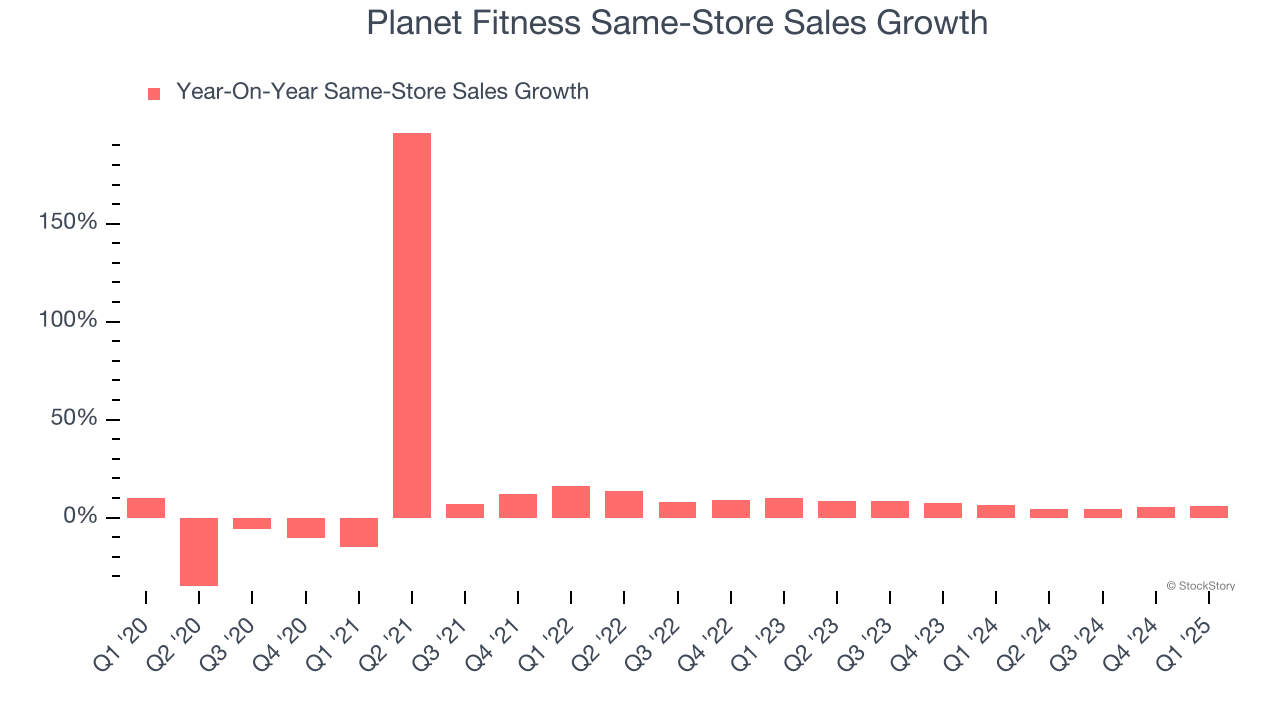

- Same-Store Sales rose 6.1% year on year, in line with the same quarter last year

- Market Capitalization: $8.53 billion

"We ended the first quarter with approximately 20.6 million members, an increase of approximately 900,000 from the end of 2024, and we grew system-wide same club sales by 6.1 percent," said Colleen Keating, Chief Executive Officer.

Company Overview

Founded by two brothers who purchased a struggling gym, Planet Fitness (NYSE: PLNT) is a gym franchise that caters to casual fitness users by providing a friendly and inclusive atmosphere.

Sales Growth

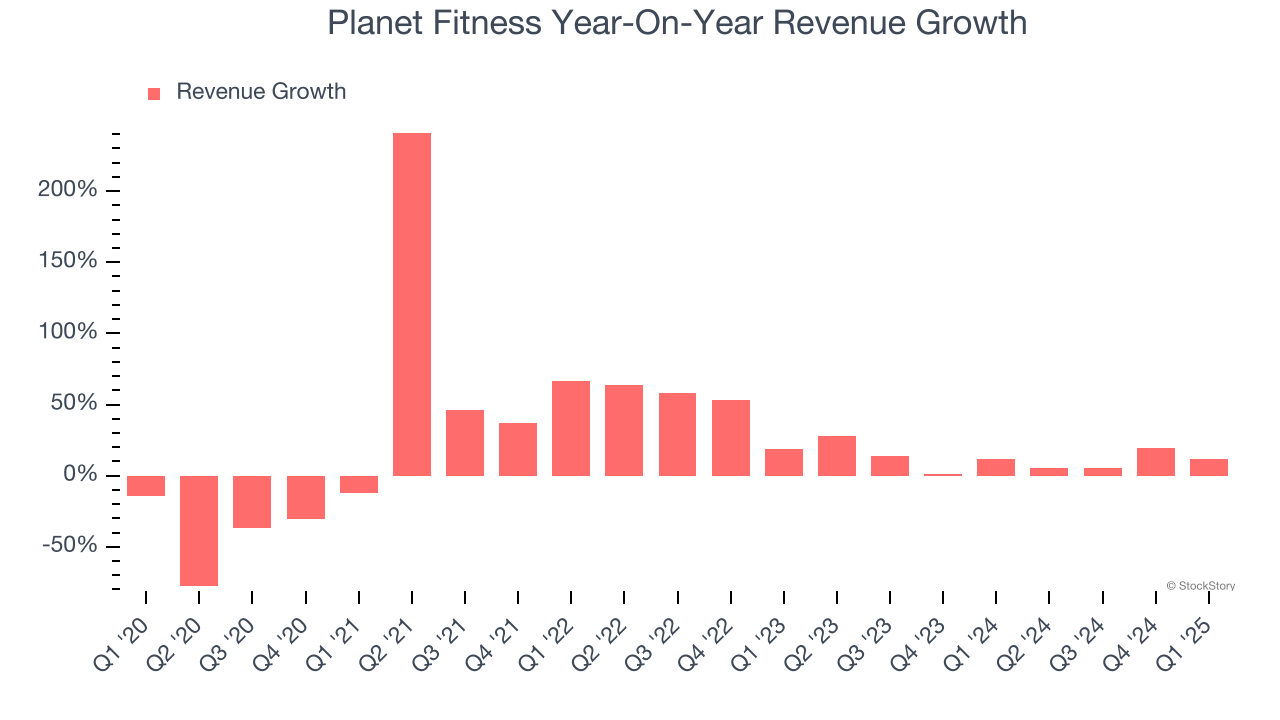

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Planet Fitness grew its sales at a 12.6% annual rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Planet Fitness’s recent performance shows its demand has slowed as its annualized revenue growth of 11.6% over the last two years was below its five-year trend. Note that COVID hurt Planet Fitness’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

We can better understand the company’s revenue dynamics by analyzing its same-store sales, which show how much revenue its established locations generate. Over the last two years, Planet Fitness’s same-store sales averaged 6.4% year-on-year growth. Because this number is lower than its revenue growth, we can see the opening of new locations is boosting the company’s top-line performance.

This quarter, Planet Fitness’s revenue grew by 11.5% year on year to $276.7 million but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 10.7% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not catalyze better top-line performance yet.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Planet Fitness’s operating margin has been trending up over the last 12 months and averaged 27% over the last two years. On top of that, its profitability was elite for a consumer discretionary business thanks to its efficient cost structure and economies of scale.

In Q1, Planet Fitness generated an operating profit margin of 28.6%, up 2.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

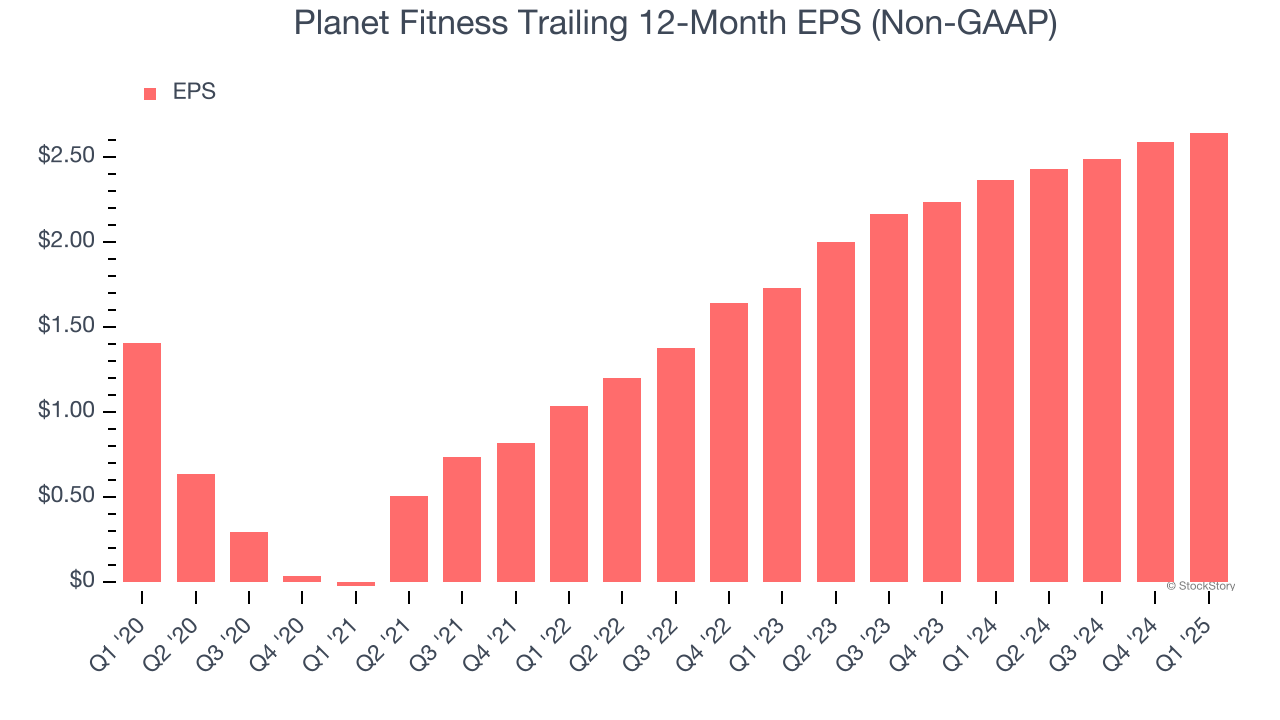

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Planet Fitness’s solid 13.4% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

In Q1, Planet Fitness reported EPS at $0.59, up from $0.53 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Planet Fitness’s full-year EPS of $2.64 to grow 14.3%.

Key Takeaways from Planet Fitness’s Q1 Results

It was good to see Planet Fitness narrowly top analysts’ same-store sales expectations this quarter. On the other hand, its revenue, EPS, and EBITDA missed. Overall, this quarter could have been better. The stock traded down 2.2% to $99.50 immediately after reporting.

Planet Fitness’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.