What a fantastic six months it’s been for Oceaneering. Shares of the company have skyrocketed 62.3%, hitting $36.69. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Oceaneering, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Oceaneering Not Exciting?

We’re happy investors have made money, but we don't have much confidence in Oceaneering. Here are three reasons why OII doesn't excite us and a stock we'd rather own.

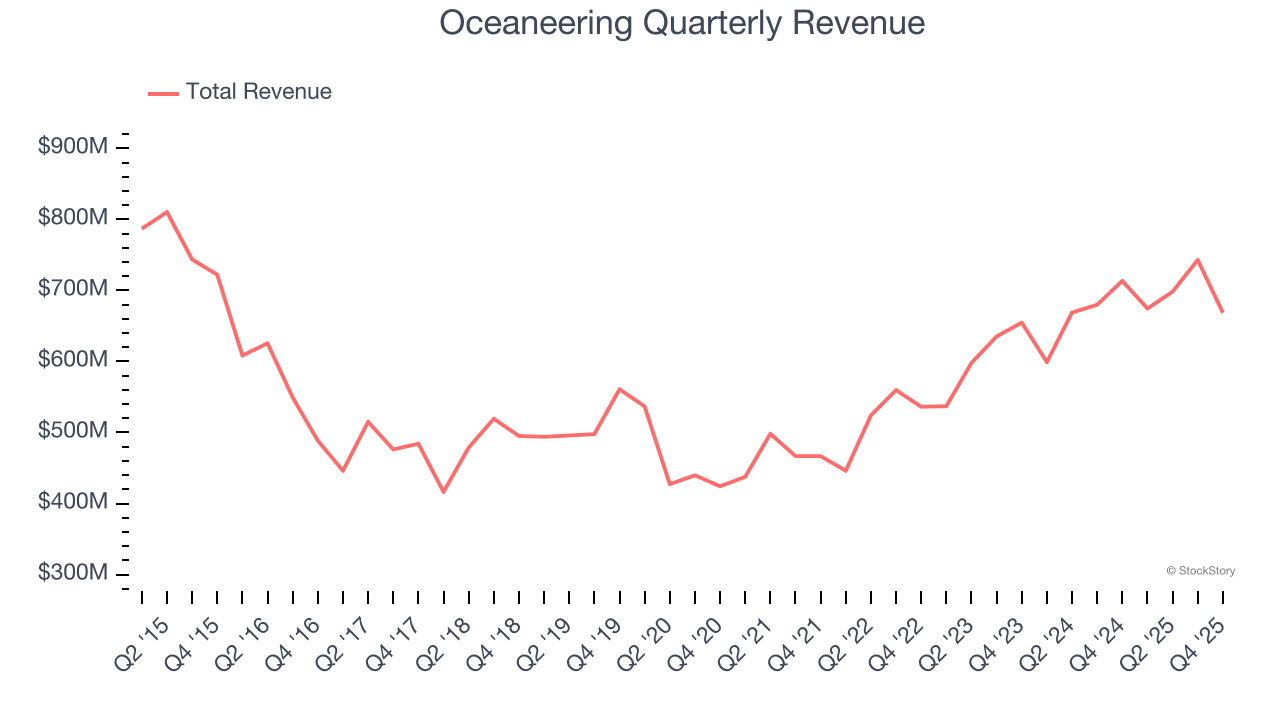

1. Long-Term Revenue Growth Disappoints

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Regrettably, Oceaneering’s sales grew at a mediocre 8.8% compounded annual growth rate over the last five years. This was below our standard for the energy upstream and integrated energy sector.

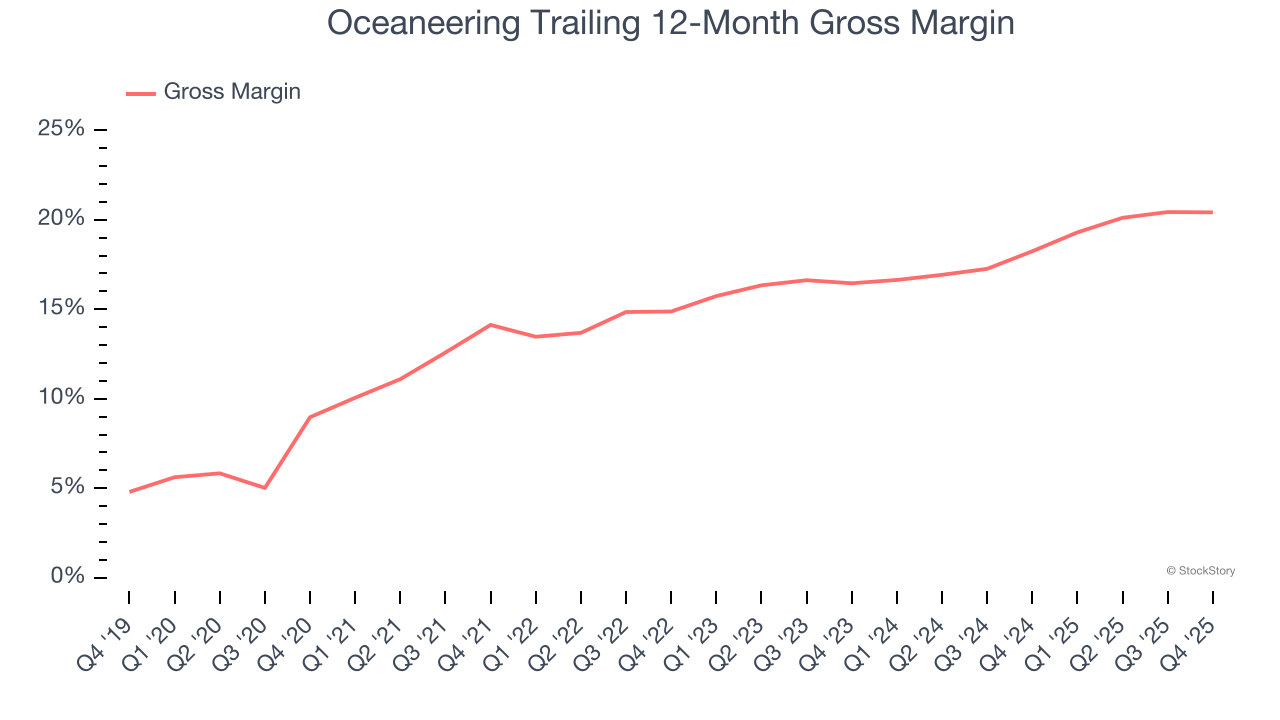

2. Low Gross Margin Reveals Weak Structural Profitability

While energy gross margins can be distorted by commodity prices, hedging, and short-term cost swings, sustained margins across a full cycle reflect a producer’s underlying asset quality, infrastructure position, and cost structure.

Oceaneering, which averaged 17.1% gross margin over the last five years, exhibiting bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

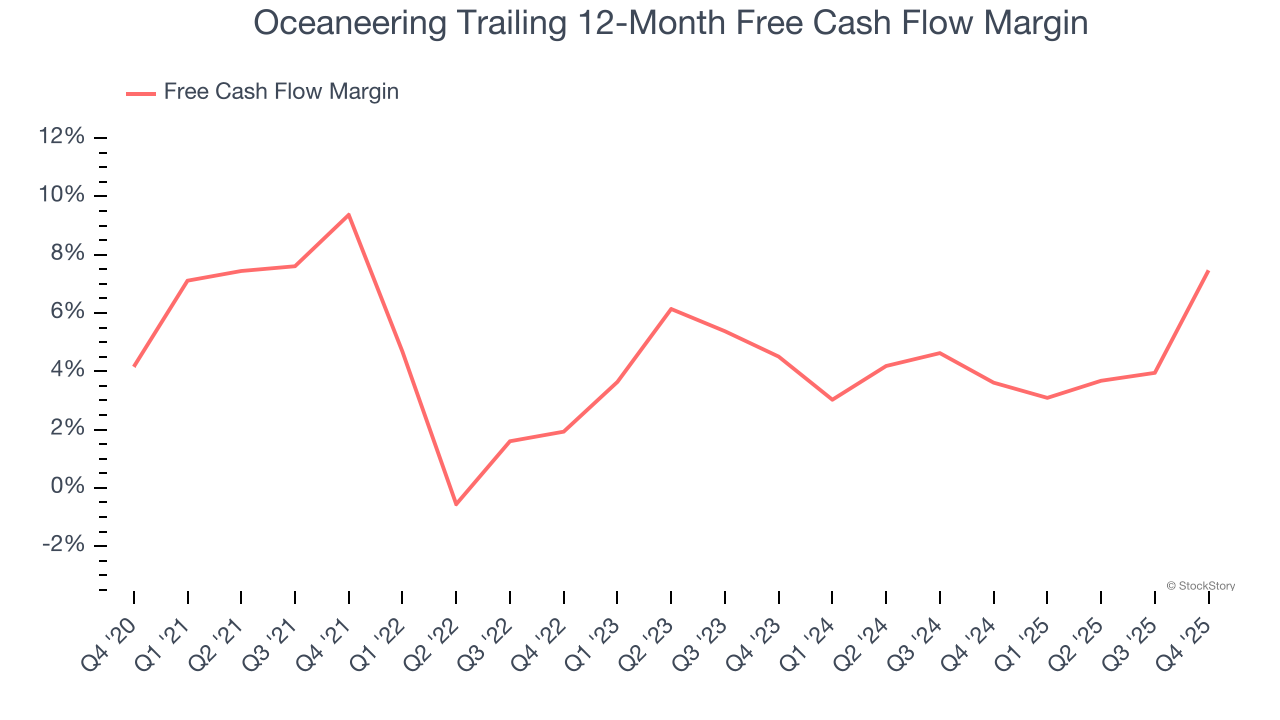

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Oceaneering has shown mediocre cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 5.3%, below what we’d expect for an upstream and integrated energy business.

Final Judgment

Oceaneering isn’t a terrible business, but it doesn’t pass our bar. Following the recent rally, the stock trades at 20× forward P/E (or $36.69 per share). This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere. We’d recommend looking at the most entrenched endpoint security platform on the market.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.