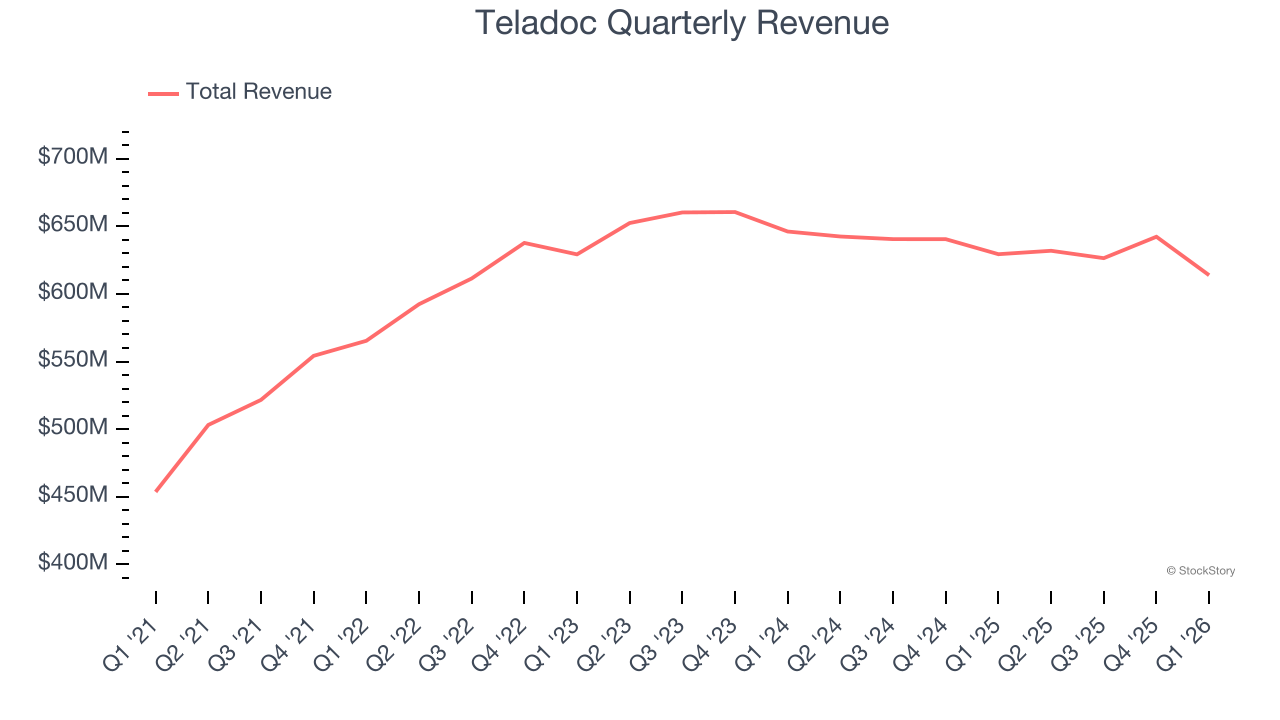

Digital medical services platform Teladoc Health (NYSE: TDOC) announced better-than-expected revenue in Q1 CY2026, but sales fell by 2.5% year on year to $613.8 million. Revenue guidance for the full year exceeded analysts’ estimates, but next quarter’s guidance of $611.5 million was less impressive, coming in 2% below expectations. Its GAAP loss of $0.36 per share was 4.7% below analysts’ consensus estimates.

Is now the time to buy Teladoc? Find out by accessing our full research report, it’s free.

Teladoc (TDOC) Q1 CY2026 Highlights:

- Revenue: $613.8 million vs analyst estimates of $610.8 million (2.5% year-on-year decline, 0.5% beat)

- EPS (GAAP): -$0.36 vs analyst expectations of -$0.34 (4.7% miss)

- Adjusted EBITDA: $58.17 million vs analyst estimates of $56.17 million (9.5% margin, 3.6% beat)

- The company reconfirmed its revenue guidance for the full year of $2.53 billion at the midpoint

- EPS (GAAP) guidance for the full year is -$0.90 at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for the full year is $286.5 million at the midpoint, above analyst estimates of $282.1 million

- Operating Margin: -10.1%, up from -19.2% in the same quarter last year

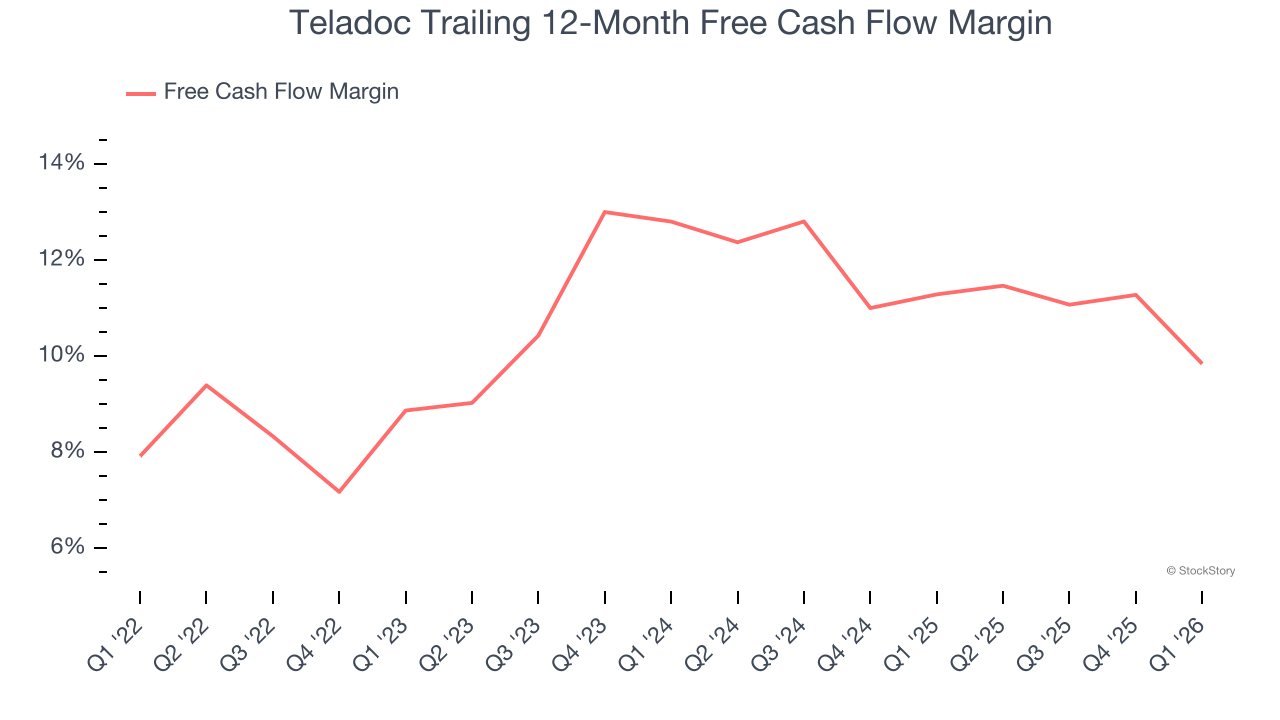

- Free Cash Flow was -$24.65 million, down from $85.12 million in the previous quarter

- Market Capitalization: $1.08 billion

Company Overview

Founded to help people in rural areas get online medical consultations, Teladoc Health (NYSE: TDOC) is a telemedicine platform that facilitates remote doctor’s visits.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Teladoc struggled to consistently increase demand as its $2.51 billion of sales for the trailing 12 months was close to its revenue three years ago. This was below our standards and is a tough starting point for our analysis.

This quarter, Teladoc’s revenue fell by 2.5% year on year to $613.8 million but beat Wall Street’s estimates by 0.5%. Company management is currently guiding for a 3.2% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection is underwhelming and implies its newer products and services will not catalyze better top-line performance yet.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Cash Is King

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Teladoc has shown impressive cash profitability, driven by its attractive business model that gives it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.6% over the last two years, better than the broader consumer internet sector.

Teladoc burned through $24.65 million of cash in Q1, equivalent to a negative 4% margin. The company’s cash flow turned negative after being positive in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Key Takeaways from Teladoc’s Q1 Results

It was great to see Teladoc’s full-year EBITDA guidance top analysts’ expectations. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 5.7% to $5.61 immediately following the results.

Teladoc’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).